- Best card for flights: The IDFC FIRST Wealth (lifetime-free, 10X RP on all travel from the first transaction, 1.5% forex) beats the Select for frequent travellers spending above ₹20,000/month — but both are significantly devalued in 2026.

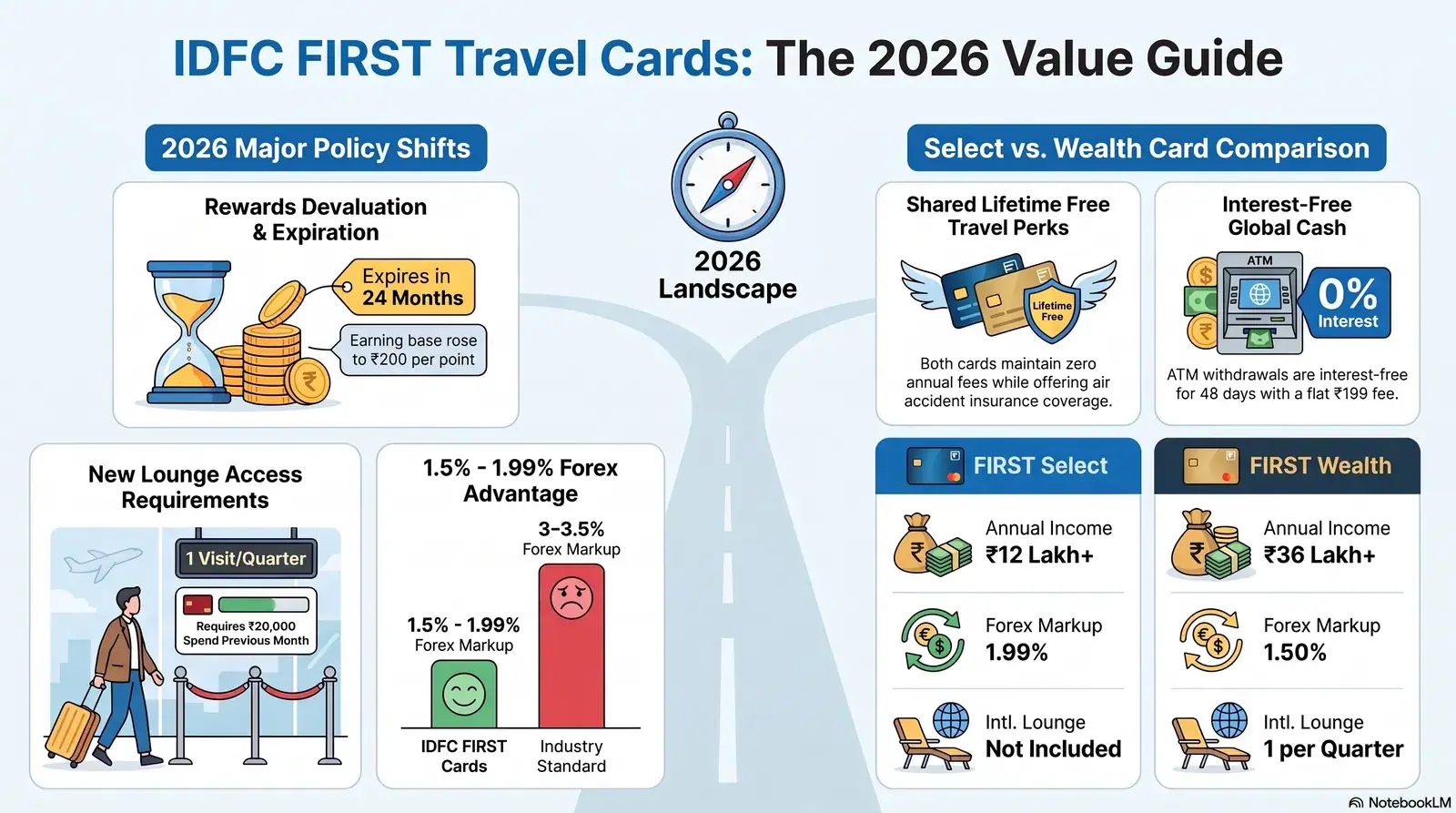

- 2026 devaluations: Reward base changed from ₹150 to ₹200 per point in January (25% cut), lounge access halved from April (now 1 per quarter vs 2), and RP now expire after 24 months from June 18. Factor these in before choosing.

- OTA discounts still work: Use coupon code EMTBIDFC on EaseMyTrip and IDFCEMI on Cleartrip for instant discounts; MakeMyTrip offers No Cost EMI on 3/6-month tenures with IDFC First cards.

1.99% — vs 3–3.5% industry standard

1.5% — one of the lowest on a lifetime-free card

₹0.25 per point (unchanged in 2026)

Interest-free up to 45–48 days; ₹199 + GST flat fee

In this guide

- IDFC First Bank Travel Card Lineup in 2026

- Reward Points on Flight Bookings: Exact Rates

- Lounge Access: What Changed in April 2026?

- Forex Markup and Zero-Interest Cash Withdrawal

- Flight Booking Discounts: OTA Codes and Offers

- DCC Trap and OTP Blocks on Foreign Airline Sites

- TCS Rules When Booking International Flights

- IDFC Rewards and Savings Calculator

- IDFC Wealth vs Select vs Axis Atlas: Head-to-Head

- Verdict: Which IDFC Card for Which Traveller?

IDFC First Bank Travel Card Lineup in 2026: What's Active?

IDFC FIRST Bank currently offers two active lifetime-free travel credit cards — the FIRST Select and FIRST Wealth — while the co-branded Club Vistara IDFC FIRST card was discontinued and is no longer available for renewal after March 2026. The Club Vistara card was axed following the Vistara–Air India merger in November 2024; all accumulated CV Points were converted to Maharaja Club (Air India) points at a 1:1 ratio and are now governed by Air India's Maharaja Club programme.

The two remaining cards target different income brackets. The IDFC FIRST Select requires a minimum annual income of ₹12 lakh and carries a 1.99% forex markup. The IDFC FIRST Wealth — a Visa Infinite product — requires a net monthly income of ₹3 lakh (annual income ₹36 lakh or equivalent ITR) and charges 1.5% forex markup. Both carry zero joining fee and zero annual fee for life. IDFC also offers the Diamond Reserve (zero forex markup, but paid card) and the Millennia (entry-level), which are outside this guide's travel focus.

If you held this card, renewal was stopped from March 31, 2026. Your accumulated CV Points (now Maharaja Points in Air India's loyalty programme at 1:1) can be redeemed against Air India flights. Contact IDFC FIRST Bank customer care to transition to the Wealth or Select card depending on income eligibility.

Reward Points on Flight Bookings: Exact Rates After 2026 Changes

The IDFC FIRST Wealth card earns 10 reward points per ₹200 on all travel, dining, and international spends from the very first eligible transaction in a billing cycle — a significant improvement over the earlier structure that required ₹20,000 monthly spend to unlock 10X. However, effective January 18, 2026, the earning base was revised from ₹150 to ₹200 per point, representing approximately a 25% devaluation in the programme's value.

The IDFC FIRST Select earns at a tiered rate: 3 reward points per ₹200 on spends up to ₹20,000 per month, and 10 reward points per ₹200 on spends exceeding ₹20,000 in the billing cycle. Each reward point is worth ₹0.25 at redemption, making the effective return rate 0.375% on standard Select spend (below ₹20k) and up to 1.25% on higher spends. The Wealth card effectively delivers 1.25% on travel from rupee one.

Bonus on OTA bookings via FIRST Rewards Gallery: Both cards earn an additional 10% bonus reward points on flight bookings and 20% bonus on hotel bookings made through the 'FIRST Rewards Gallery' section inside the IDFC FIRST Bank mobile app. This bonus is capped at 8,000 bonus reward points per billing cycle. Note that the app's OTA prices may not always match direct airline sites — compare fares before booking.

Effective June 18, 2026, reward points on the FIRST Wealth and FIRST Millennia cards expire after 24 months from the date of credit. Previously, IDFC reward points were lifetime-valid — a major differentiator. If you have a large accumulated balance, redeem before the oldest batch reaches 24 months. The FIRST Select card's expiry policy was also aligned to 24 months in this update.

Reward points are not earned on fuel transactions, EMI conversions, or cash withdrawals. If the minimum amount due is not paid on time in any billing cycle, no reward points are credited for that month's spends — a penalty clause introduced as part of the January 2026 revision.

Lounge Access in 2026: What Was Cut in April?

Both the IDFC FIRST Select and FIRST Wealth cards reduced their complimentary airport lounge access from April 1, 2026 — from 2 visits per quarter to 1 visit per quarter — and introduced a mandatory ₹20,000 monthly spend condition to unlock lounge access for the following month. This means you must spend ₹20,000 on the card in any calendar month to activate 1 lounge visit in the next calendar month for both cards.

Railway lounge access was not cut and remains a strength of both cards. The Select card offers 4 complimentary railway lounge visits per quarter; the Wealth card offers 4 railway lounge visits per year. Railway lounges are accessible at major Indian stations including New Delhi, Mumbai Central, Chennai Central, and Howrah, and access is verified via the credit card at the lounge counter without a separate membership.

| Benefit | IDFC FIRST Select | IDFC FIRST Wealth |

|---|---|---|

| Annual Fee | ₹0 (lifetime free) | ₹0 (lifetime free) |

| Income Eligibility | ₹12L+ annual income | ₹36L+ annual income / ₹3L+ monthly net |

| Forex Markup | 1.99% | 1.5% |

| Reward on Travel Spend | 10 RP/₹200 (above ₹20k/month); 3 RP/₹200 below | 10 RP/₹200 from 1st transaction (no threshold) |

| Reward Point Value | ₹0.25 per point | ₹0.25 per point |

| Domestic Lounge (post Apr 2026) | 1 per quarter (spend ₹20k prev month) | 1 per quarter (spend ₹20k prev month) |

| International Lounge (post Apr 2026) | Not included | 1 per quarter (spend ₹20k prev month) |

| Railway Lounge | 4 visits per quarter | 4 visits per year |

| Cash Withdrawal (interest) | 0% interest, ₹199 + GST per withdrawal | 0% interest, ₹199 + GST per withdrawal |

| Air Accident Cover | ₹1 crore | ₹1 crore |

| Personal Accident Cover | ₹5 lakh | ₹5 lakh |

| Card Network | Visa | Visa Infinite |

Sources: IDFC FIRST Select official PDF, IDFC FIRST Wealth official PDF, July 2026.

On-the-Ground Insight: "I've held the IDFC Wealth card for two years and the April 2026 lounge change stung — I used to get 2 domestic visits a quarter but now it's just 1, and I have to remember to hit ₹20k in the previous month. Last month I forgot and was turned away at the Bengaluru lounge. The card still saves me real money on forex when booking Emirates directly, but I now keep a secondary lounge card for the days I miss the spend threshold." — Rohit M., IIIT Hyderabad alumni, frequent Dublin–Hyderabad traveller

Forex Markup and Zero-Interest Cash Withdrawal: The Real Numbers

The IDFC FIRST Wealth card's 1.5% forex markup is one of the lowest available on a lifetime-free card in India in 2026 — saving you ₹1,500–₹2,000 compared to standard cards on every ₹1 lakh of international spend. The Select card's 1.99% forex is similarly competitive against the 3–3.5% charged by most Indian bank credit cards. Both are billed on your statement as a separate line item alongside the INR transaction amount, making it easy to track.

The zero-interest cash withdrawal feature is genuinely unusual in India's credit card market. Both the Select and Wealth cards allow ATM cash withdrawals with zero interest for up to 45–48 days — matching the standard billing cycle interest-free period — and charge only a flat ₹199 + GST per withdrawal (source: IDFC FIRST Bank official forex benefit page). This is valuable for travellers who land internationally and need emergency cash before exchanging currency.

True Cost = Base Fare (in foreign currency) × (1 + Forex Markup %) + Reward Points Offset

Example: A ₹80,000 Dublin–Delhi flight booked on a foreign-currency site with the Wealth card costs ₹80,000 × 1.015 = ₹81,200. You earn 10 RP/₹200 = 4,000 points = ₹1,000 cashback. Net true cost: ₹80,200 vs ₹82,800 on a 3.5% forex card with no rewards.

For international airline website bookings, the forex markup applies to the base fare only. Taxes and fees quoted in INR are not subject to forex markup. If a booking portal offers Dynamic Currency Conversion (DCC) — charging your card in Indian rupees instead of the local currency — always decline (see the DCC section below), as DCC rates are typically 4–8% above the mid-market rate, wiping out the IDFC card's forex advantage entirely.

Flight Booking Discounts on EaseMyTrip, MakeMyTrip, and Cleartrip (July 2026)

IDFC FIRST Bank credit cards qualify for instant discounts and No Cost EMI options on India's major Online Travel Agencies (OTAs) — including EaseMyTrip, Cleartrip, and MakeMyTrip — with dedicated coupon codes verified as active in July 2026.

EaseMyTrip: Apply coupon code EMTBIDFC at checkout for an instant discount on confirmed domestic and international flight bookings. The No Cost EMI offer uses code IDFC6EMI for 6-month zero-interest instalment plans on IDFC FIRST Bank credit cards. EaseMyTrip's July 2026 monsoon promotion also runs broader IDFC discounts — check the bank's EaseMyTrip offers page for the current active deal before booking.

Cleartrip: Enter coupon code IDFCEMI at payment to receive an instant discount on IDFC FIRST Bank credit card transactions. Cleartrip also runs No Cost EMI campaigns with IDFC cards periodically — the current offer page confirms availability through mid-2026.

MakeMyTrip: IDFC FIRST Bank credit cards qualify for No Cost EMI on 3-month and 6-month tenures plus instant discounts during active campaign periods. MakeMyTrip runs promotional windows (typically 2-week periods each month) — the bank's offer page lists currently valid windows. Bookmark the offer page and check before purchase rather than assuming the deal is live.

Additionally, the IDFC FIRST Bank mobile app's FIRST Rewards Gallery allows booking flights and hotels while earning 10% bonus RP on flights and 20% bonus RP on hotels, capped at 8,000 bonus points per cycle. Compare the Rewards Gallery price against direct airline booking and OTA prices before confirming — the bonus points add value only if the underlying fare is competitive.

OTA promotions with IDFC FIRST Bank are time-limited and typically renewed monthly or quarterly. Codes listed in this article were verified in July 2026. Always confirm current validity on the bank's official offers page before checking out — using an expired code results in no discount without error notice on some platforms.

Avoiding the DCC Trap and OTP Blocks on Foreign Airline Websites

Dynamic Currency Conversion (DCC) is the single biggest hidden cost trap for Indian cardholders booking on foreign airline websites — always choose to pay in the airline's local currency, never in INR, to preserve your IDFC card's 1.5% forex advantage.

When you book on Emirates.com, British Airways, Etihad, or other foreign airline sites using an Indian credit card, the payment page typically presents a DCC offer: "Would you like to pay ₹86,500 in Indian Rupees instead of USD 1,040?" The INR rate in this offer is set by the DCC provider — not Visa or IDFC — at a markup of 4–8% above the mid-market rate. Accepting DCC converts what should have been a 1.5% IDFC markup into a 5.5–9.5% effective cost. Always select "Pay in local currency" (USD / EUR / GBP / AED) and let IDFC's competitive forex rate do its job.

Point of Sale (PoS) Arbitrage: The same flight on a foreign airline's site can cost differently depending on which regional version of the website you access. A Dublin-to-Delhi flight on Air India's UK site priced in GBP may be 6–10% cheaper than the same fare on the India site in INR after accounting for PoS pricing differences and fare class availability. Use Incognito mode, clear cookies, and compare the INR equivalent across 2–3 regional site versions before booking.

OTP and e-mandate blocks: Before booking an international flight on a foreign website using your IDFC FIRST card, ensure international transactions are enabled. In the IDFC FIRST Bank mobile app, navigate to Cards → your card → Card Controls → International Usage → Enable. For high-value transactions (typically above ₹2 lakh), IDFC sends an OTP to your registered mobile number as part of 3D Secure authentication. If your number lacks international roaming when you're abroad, enable SMS alerts via the app before you travel. For repeated transaction failures on Lufthansa.com or similar European sites, contact IDFC customer care to confirm no daily international limit is set below the transaction value.

TCS Rules for International Flight Bookings with IDFC Cards in 2026

No TCS (Tax Collected at Source) applies to standalone international airline ticket purchases made with an Indian credit card — this has been the consistent position under LRS rules and was not altered by Budget 2026. TCS under the Liberalised Remittance Scheme (LRS) applies to remittances, not to domestic card-based payments for foreign travel services.

The TCS framework for 2026 is as follows, per the Reserve Bank of India (RBI) and Finance Act 2025 / Budget 2026 updates:

| Transaction Type | TCS Rate (2026) | Threshold | Notes |

|---|---|---|---|

| Standalone air tickets (credit card) | Nil | No threshold — not applicable | Never subject to TCS; credit card purchase is not LRS remittance |

| Overseas tour packages | 2% flat (from Apr 1, 2026) | No minimum threshold | Budget 2026 removed the earlier 5%/20% bracket structure |

| LRS remittances — general | 20% above ₹10 lakh/FY | ₹10 lakh per FY (Finance Act 2025) | Threshold raised from ₹7L to ₹10L from Apr 1, 2025 |

| Education via specified loan | Nil | No threshold | Finance Act 2025: removed TCS on education loans from recognised lenders |

| Loading a multi-currency forex card | 20% above ₹10 lakh/FY | Cumulative annual LRS limit | Forex card loading is treated as LRS remittance; tracked cumulatively across FY |

Sources: Finance Act 2025 (April 1, 2025), Union Budget 2026 (April 1, 2026), RBI LRS guidelines.

In practice, the TCS you pay on LRS remittances above ₹10 lakh is fully reclaimable as a credit in your annual Income Tax Return (ITR) — it is advance tax collection, not an additional levy. If you are an Indian resident NRI purchasing a ₹1.5 lakh international ticket using your IDFC FIRST Wealth card on an airline's website, zero TCS applies.

IDFC First Bank Rewards and Forex Savings Calculator

Use this calculator to compare the Select and Wealth card reward earnings and forex savings on your flight spend — all constants below are sourced from the card benefit tables in this article.

🧮 IDFC First Bank Flight Booking Rewards Calculator

Compare reward points earned and forex savings between Select and Wealth cards on your international flight spend.

IDFC FIRST Wealth vs IDFC FIRST Select vs Axis Bank Atlas: Head-to-Head

The IDFC FIRST Wealth is the strongest lifetime-free travel card in its income bracket for Indian travellers primarily spending on international flights — but for frequent flyers doing 3 or more international trips per month, Axis Bank Atlas's EDGE miles programme offers higher effective returns despite its ₹10,000 annual fee.

| Feature | IDFC FIRST Wealth | IDFC FIRST Select | Axis Bank Atlas | HDFC Regalia Gold |

|---|---|---|---|---|

| Annual Fee | ₹0 | ₹0 | ₹10,000 | ₹2,500 (waived at ₹2–3L spend) |

| Forex Markup | 1.5% | 1.99% | 2% | 2% |

| Travel Reward Rate | 10 RP/₹200 (1.25% return) | 10 RP/₹200 above ₹20k (1.25%), else 0.375% | 5 EDGE miles/₹200 on travel (converts to airline miles) | 10X RP via SmartBuy portal (~2% effective) |

| Lounge (Domestic) | 1/quarter (₹20k spend req.) | 1/quarter (₹20k spend req.) | Unlimited (no spend req.) | 8/year (no spend req.) |

| Lounge (International) | 1/quarter (₹20k spend req.) | None | 8/year via Priority Pass | 6/year via Priority Pass |

| Best for | Monthly spenders ₹20k+, international travel | Moderate spenders wanting lifetime-free card | Frequent flyers (3+ trips/month) wanting air miles | Mid-tier spenders wanting SmartBuy portal rewards |

Sources: Official card benefit pages, PaisaBazaar comparison, TradeBrains 2026 comparison, July 2026.

The key distinguishing factor for IDFC Wealth is the combination of zero annual fee and 1.5% forex markup. Against the Axis Atlas, a traveller spending ₹5 lakh/year on international flights saves ₹10,000 in annual fees on the IDFC Wealth, while Atlas's EDGE miles programme can deliver free domestic flights (approximately 1 IndiGo ticket = 6,500 EDGE miles) for heavy spenders. If you're spending above ₹8–10 lakh/year on flights, Axis Atlas's superior miles return overtakes IDFC's fee-free advantage.

A note on IDFC card cons: The 2026 devaluations are real and material. The reward base change (₹150 → ₹200 per point) reduced the per-rupee return by ~25%. The lounge access halving removes a key differentiator vs competitors. And the 24-month RP expiry means the programme no longer rewards long-term accumulation for redemptions. These are legitimate downsides that must be weighed against the zero-fee, low-forex advantages.

Verdict: Which IDFC Card Is Best for Which Traveller?

The IDFC FIRST Wealth is the correct choice for any eligible Indian traveller who books international flights regularly and wants a lifetime-free card with low forex exposure — provided you can maintain ₹20,000 monthly spend to keep the lounge benefit alive. For budget travellers or students who may not consistently hit ₹20,000 monthly spend, the IDFC FIRST Select offers the same zero-fee foundation with a slightly higher forex rate, and the reward structure on Select becomes competitive above ₹20,000 monthly spend.

Neither card is suitable as your sole card for maximising airline miles or accessing unlimited lounges — pair either IDFC card with a dedicated miles card (Axis Atlas or Air India SBI Signature) if frequent flying is your primary use case. The IDFC Wealth card earns best as a daily-spend card that also handles international travel without the fee burden of premium cards.

- International student / NRI traveller: IDFC FIRST Wealth if income-eligible — best zero-fee + low forex combo. Select as fallback.

- Occasional traveller (1–2 trips/year): IDFC FIRST Select — simpler to qualify, same zero-fee benefit, OTA codes work on both.

- Frequent business traveller (3+ trips/month): Axis Bank Atlas or HDFC Infinia for superior miles and unrestricted lounge access; keep IDFC Wealth as secondary for non-travel spends.

- Cash-heavy traveller: Either IDFC card — zero-interest cash withdrawal is a rare and genuine benefit for ATM withdrawals abroad.

Frequently Asked Questions

Which IDFC First Bank credit card is best for flight bookings?

The IDFC FIRST Wealth card is best for flight bookings in 2026 — it earns 10X reward points from the first transaction on travel and international spends, charges a lower 1.5% forex markup vs 1.99% on the Select, and is lifetime-free. For lower-income cardholders who don't qualify for the Wealth (which requires ₹36L+ annual income), the IDFC FIRST Select offers the same zero-fee structure with competitive rewards above ₹20,000 monthly spend.

Does IDFC First Bank charge forex markup on international flight bookings?

Yes — the IDFC FIRST Wealth charges 1.5% and the IDFC FIRST Select charges 1.99% forex markup on international transactions. Both are significantly below the industry standard of 3–3.5%. For zero forex markup, IDFC's WOW! Black and Diamond Reserve cards are options, though those carry joining fees.

How do I earn reward points on flights with IDFC First Bank cards?

With the IDFC FIRST Wealth card, you earn 10 reward points per ₹200 on all travel and international spends from your very first transaction in a billing cycle. Additionally, booking flights via the 'FIRST Rewards Gallery' in the IDFC FIRST Bank mobile app earns 10% bonus reward points on flights and 20% on hotels (capped at 8,000 bonus points). Each reward point is worth ₹0.25. Note: reward points now expire after 24 months from June 18, 2026.

Does IDFC First Bank credit card offer lounge access?

Yes, but with reduced benefits since April 2026 — both the Select and Wealth cards now offer 1 complimentary domestic airport lounge visit per quarter, down from 2 before April 2026. The Wealth additionally provides 1 international lounge visit per quarter. Both require a minimum spend of ₹20,000 in the previous calendar month to unlock lounge access. Railway lounges are unaffected: Select offers 4 per quarter and Wealth offers 4 per year.

Is there TCS on flight tickets booked with IDFC First Bank credit cards?

No TCS applies on standalone international airline tickets purchased with an Indian credit card — this has never applied and remains unchanged under Budget 2026. TCS at 20% applies only on LRS remittances above ₹10 lakh per financial year (threshold raised by Finance Act 2025). Overseas tour packages attract a flat 2% TCS with no minimum threshold under Budget 2026 rules.

Ready to Book? Find the Cheapest Fares for Your IDFC Card

Compare live Dublin-to-India and London-to-India fare calendars across Emirates, Etihad, Qatar Airways, and Air India — and pair your IDFC FIRST card discount codes with the lowest base fare available.

- HDFC Bank Credit Card Flight Offers 2026 — Regalia, Infinia, and Millennia card deals on EaseMyTrip, MakeMyTrip, and airline direct bookings.

- Axis Bank Atlas and Other Travel Cards for Flight Bookings 2026 — EDGE miles, lounge access, and how Atlas compares to IDFC Wealth for frequent flyers.

- Airport Lounge Access with Indian Credit Cards 2026 — Comprehensive guide to which cards offer Priority Pass, DreamFolks, and domestic lounge access in 2026.

- Transfer Credit Card Points to Airline Miles in India 2026 — How to convert IDFC, HDFC, and Axis reward points into Air India, IndiGo, and Vistara (now Maharaja) miles.

All card benefit figures, forex rates, reward point values, lounge entitlements, OTA codes, and TCS rules cited in this article are based on official IDFC FIRST Bank benefit documents, RBI guidelines, Finance Act 2025, and Budget 2026 as publicly available in July 2026. Card benefits and OTA promotions change regularly — always verify current terms directly with IDFC FIRST Bank, the respective OTA, and the Reserve Bank of India before applying for a card or booking a flight. MyFlightOffers is not affiliated with IDFC FIRST Bank or any organisation mentioned. This article does not constitute financial or tax advice.