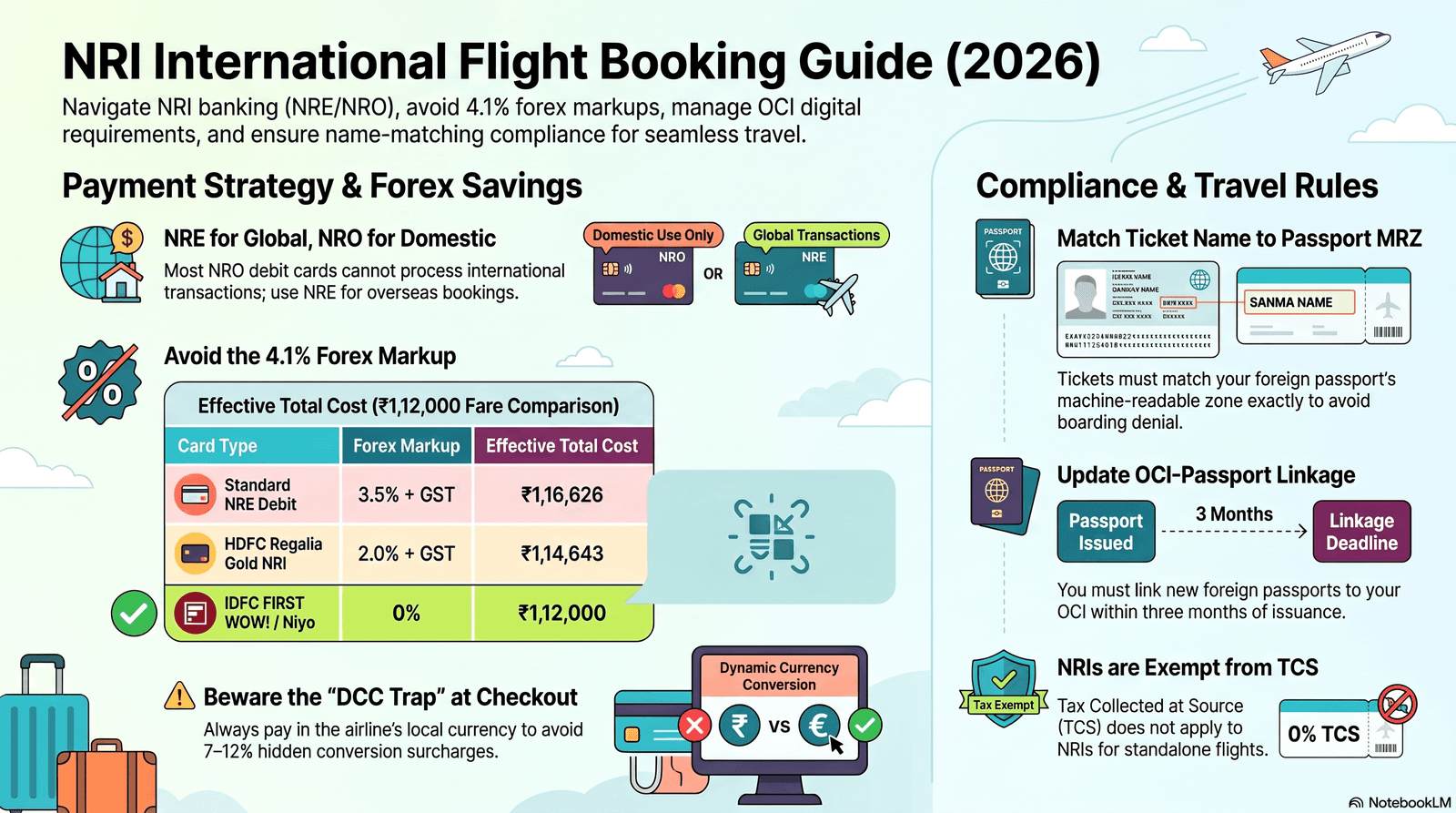

- NRE card = global, NRO card = India-only: Most NRO debit cards (ICICI, HDFC) cannot process international transactions. Use your NRE debit card or an NRI credit card for overseas bookings.

- 3.5% + GST is the default markup — but zero-forex options exist: Standard NRE debit cards levy a cross-currency surcharge of 3.5% plus GST (~4.1% effective). IDFC FIRST WOW! NRI Credit Card and Niyo Global card charge zero markup.

- TCS does not apply to NRIs under LRS — but OCI name must match your foreign passport exactly: The Liberalised Remittance Scheme applies only to resident Indians. Always book your ticket in the name printed on the foreign passport you will travel with.

NRE card — international use?

✅ Yes — Visa/Mastercard, 3.5% + GST forex markup

NRO card — international use?

❌ No — domestic India use only (most banks)

TCS on standalone flight tickets?

❌ No TCS — neither for NRIs nor resident Indians

Best zero-forex option?

IDFC FIRST WOW! NRI Card or Niyo Global (₹0 markup)

In this guide

- NRE vs NRO: what each account covers for flight payments

- Can you book flights with an NRE or NRO debit/credit card internationally?

- Enabling international transactions: step-by-step for HDFC, ICICI, SBI

- Name matching on tickets: why your passport name matters for NRI bookings

- OCI card travel rules 2026: what immigration expects at Indian airports

- TCS and LRS 2026: does it apply to NRIs booking flights?

- Best payment strategy: NRE card vs Indian credit card vs Wise vs Niyo

1. NRE vs NRO: What Each Account Covers for Flight Payments

An NRE (Non-Resident External) account holds foreign earnings converted to INR and is freely repatriable with no upper limit, while an NRO (Non-Resident Ordinary) account holds India-sourced income (rent, dividends, pensions) and has a repatriation cap of USD 1 million per financial year under the Reserve Bank of India's FEMA master circular. This structural difference directly affects how each account's linked card behaves at international checkout.

For flight booking purposes, the practical distinction is simple: NRE accounts are designed for global spending, NRO accounts are designed for domestic Indian spending. Interest on NRE balances is tax-free in India as long as the account holder maintains non-resident status under the Income Tax Act, 2025 (formerly the Income Tax Act, 1961). NRO interest is taxable at 30% plus surcharge, though NRIs from countries with a Double Taxation Avoidance Agreement (DTAA) — including Ireland, the UK, UAE, USA, Canada, and Australia — can apply for a lower withholding rate by filing Form 15G/15H or Form 10-F with their bank.

NRE funds: freely repatriable, no cap, no RBI permission needed. NRO funds: up to USD 1 million per financial year, requires Form 145 (new format, effective 1 April 2026 — replaces old Form 15CA) and chartered accountant certificate Form 146 (replaces Form 15CB) per the Income Tax Rules, 2026.

2. Can You Book International Flights with an NRE or NRO Debit/Credit Card?

NRE debit cards linked to Visa or Mastercard networks can be used on any international airline website or OTA that accepts cards, provided international usage is enabled. NRO debit cards are restricted to domestic Indian transactions by default at most banks — they cannot process international payments online or overseas.

Here is the full picture by account and card type:

| Card Type | International Online Booking? | Forex Markup | Key Restriction |

|---|---|---|---|

| NRE Debit Card (HDFC / ICICI / SBI / Axis) | ✅ Yes — after enabling | 3.5% + GST (~4.1% effective) | Must enable internationally before travel; daily limit applies |

| NRO Debit Card (HDFC / ICICI) | ❌ No | N/A | Domestic India use only per bank policy |

| NRI Credit Card (ICICI NRI / HDFC Regalia Gold) | ✅ Yes | 2.0%–3.5% varies by card | Requires NRE/NRO account; approval subject to overseas income proof |

| IDFC FIRST WOW! NRI Credit Card | ✅ Yes | 0% (zero forex markup) | Requires IDFC FIRST NRE savings account; no NRO-only applicants |

| Niyo Global Zero Forex Card | ✅ Yes — Visa network | 0% (zero markup) | Must load INR balance; conversion at Visa network rate at point of sale |

| Wise Multi-Currency Card | ✅ Yes — 40+ currencies | 0% (mid-market rate) | Must hold foreign currency balance or convert before spending; small conversion fee applies above monthly free limit |

The ICICI Bank NRI World Debit Card (linked to NRE) is issued on the Visa network and works globally. The HDFC Bank EasyShop NRO Debit Card, by contrast, is explicitly marketed for India-only use. ICICI Bank confirms on its NRI Debit Card page that debit cards linked to NRO accounts can only be used in India. The takeaway for flight booking: if you have both NRE and NRO accounts at the same bank, always link your international booking to the NRE-linked card.

When you pay on a non-Indian airline website (Emirates.com, Lufthansa.com, British Airways) using your NRE or NRO card, the payment gateway may offer to charge you in Indian Rupees rather than the site's local currency. This is Dynamic Currency Conversion (DCC). Accepting DCC adds a 4–8% surcharge on top of your bank's existing 3.5% + GST forex markup — you could lose 7–12% of the transaction value in hidden conversion charges. Always select the airline's local currency (USD, EUR, GBP) at checkout, even if INR is offered. Your bank will do the conversion at the card network rate, which is always better.

3. Enabling International Transactions: Step-by-Step for HDFC, ICICI, and SBI

All major Indian banks disable international online transactions on NRE debit cards by default as a fraud prevention measure. You must explicitly enable them via net banking or the mobile app — a process that takes 5–10 minutes but must be done before your transaction, ideally before you leave India or before the fare expires.

How to enable international use on an HDFC NRE debit card

Log in to HDFC NetBanking, navigate to Cards → Debit Card → Manage Card, and toggle "International Usage" to ON. The change is effective immediately. You can also call the 24-hour NRI helpline at +91-22-61606161 to request activation. HDFC's Card Control feature (in the MobileBanking app) lets you set per-transaction spending limits — raise the international limit to match or exceed your expected fare before booking. HDFC's OTP Checkout sends one-time passwords via the mobile app push notification if you are abroad and do not have an Indian SIM — you must enable push alerts for the HDFC mobile app before departing.

How to enable international use on an ICICI NRE debit card

Log in to ICICI iMobile Pay or iNetBanking, go to My Accounts → Cards → Debit Card Services → Enable International Transactions. Activation can take up to 24–48 hours. Alternatively, call the ICICI NRI helpline at +91-22-33667777. For OTP delivery while abroad, ICICI supports OTP via the iMobile Pay app push notification — ensure the app is installed and logged in with your registered mobile number before you are overseas.

How to enable international use on an SBI NRE debit card

Log in to SBI YONO, go to Services → Card Services → ATM Card Services → Enable International Use. The change is applied immediately. SBI's international transaction limits default to ₹75,000 per day — significantly lower than HDFC (₹3 lakh) or ICICI (₹2.5 lakh). If your flight fare exceeds this, call the SBI NRI helpline at 1800-1234 (toll-free from India) or +91-80-26599990 from overseas to request a temporary limit increase.

On-the-Ground Insight: "I was trying to book my return flight Dublin to Delhi on the Air India website from my laptop in Ireland. My HDFC NRE debit card kept failing at checkout. Turned out international transactions were disabled — I hadn't touched the settings since I opened the account in India. I opened the HDFC app, toggled international usage on, and the next attempt went through in 30 seconds. But the fare had jumped ₹4,200 while I was troubleshooting. Always enable international use before you even start shopping for tickets." — Priya M., Dublin, MSc Graduate, Autumn 2025 Intake

4. Name Matching on Tickets: Why Your Passport Name Matters for NRI Bookings

Always book your international flight ticket in the exact name printed on the Machine Readable Zone (MRZ) of the foreign passport you will use to travel — not the name on your Indian passport, not the name on your NRE/NRO account, and not the name on your OCI booklet. Airlines and border control check passport MRZ data electronically; any discrepancy between the ticket and the MRZ triggers boarding denial or secondary immigration screening.

This is particularly critical for NRIs who have changed their surname (e.g., after marriage), acquired citizenship in a new country, or updated their foreign passport since their OCI was issued. The most common name-mismatch scenarios that cause NRI flight booking problems include surname changes not yet reflected on the OCI, expanded middle names that appear in the MRZ but were shortened on the airline booking form, and hyphenated surnames entered inconsistently.

The Directorate General of Civil Aviation issued updated passenger protection rules on 24 February 2026. If you notice a name error within 48 hours of booking and the departure is at least 15 days away (international routes), most airlines must correct the error at no charge. After 48 hours, name changes are treated as rebooking and attract cancellation/rebooking fees that can exceed ₹8,000–₹15,000 on international fares. Fix errors immediately — do not wait until check-in.

When filling in your name on any airline booking form, always copy character-for-character from your foreign passport's MRZ (the two lines of text at the bottom of the bio-data page). For example, if your foreign passport MRZ reads "SHARMA<<RAHUL<KUMAR", book as "RAHUL KUMAR SHARMA" — not "R. K. Sharma" or "Rahul Sharma". Some OTA booking forms auto-separate first and last name, which can create inconsistencies: always double-check the confirmation email to ensure your full name appears as on the MRZ before payment is processed.

5. OCI Card Travel Rules 2026: What Immigration Expects at Indian Airports

OCI (Overseas Citizen of India) cardholders travel to India visa-free for life, presenting their current foreign passport together with the OCI card (physical or digital) at Indian immigration. As of 1 May 2026, the Indian government launched a fully digital OCI system under the Citizenship (Amendment) Rules 2026, allowing the OCI credential to be stored in a mobile wallet — physical booklets are optional for travel but must still be registered against the current foreign passport.

The critical immigration requirement NRIs frequently overlook is the OCI-passport linkage. Your OCI registration must reference your current foreign passport. Every time you obtain a new foreign passport, you must update your passport details on the OCI Services portal within three months of the new passport's issuance date. Failure to do so now attracts a fine of USD 25 (or local currency equivalent) under the 2026 rules — and more practically, airlines may deny boarding if your OCI does not match the passport you present.

1. Current valid foreign passport (the one linked to your OCI registration). 2. OCI card — physical booklet or digital wallet credential. 3. Electronic Arrival Card (mandatory from 2026 — must be completed online before boarding). You do NOT need to carry the old passport on which your OCI visa stamp was originally issued, as long as the OCI details have been updated to reflect your current passport. Arriving without the updated OCI link can trigger secondary screening of 1–3 hours at Indira Gandhi International Airport (DEL) and Chhatrapati Shivaji Maharaj International Airport (BOM).

For NRIs booking return flights from Ireland to India, note that Aer Lingus and Ryanair codeshare routes to India are operated via Middle Eastern hubs (typically Dubai or Abu Dhabi). Emirates and Etihad both perform document verification at Dublin Airport before departure — carry both your foreign passport and OCI card visibly accessible, not buried in your checked-in luggage.

6. TCS and LRS 2026: Does It Apply to NRIs Booking International Flights?

Tax Collected at Source (TCS) under the Liberalised Remittance Scheme (LRS) does not apply to NRIs, because LRS is a facility available exclusively to resident individuals in India under the Foreign Exchange Management Act (FEMA). NRIs operating NRE or NRO accounts are already classified as non-residents and are governed by FEMA's NRI remittance rules — not LRS.

However, NRIs who purchase international travel from Indian travel agents or OTAs should be aware of the following 2026 Budget changes that affect packages sold by resident Indian entities:

| Transaction Type | TCS Rate (Budget 2026) | Threshold | Applies to NRIs? |

|---|---|---|---|

| Standalone airline ticket (domestic or international) | 0% — No TCS | N/A | ❌ No |

| Overseas tour package (bundled flights + hotels) | 2% from first rupee | No minimum threshold | ⚠️ May apply if booked via Indian agent |

| General LRS outward remittance (resident individuals) | 2% above ₹10 lakh/year | ₹10 lakh per financial year | ❌ No — LRS not available to NRIs |

| Education remittance (student abroad) | 0.5% above ₹10 lakh | ₹10 lakh | ❌ No — LRS not available to NRIs |

The practical implication: if you are an NRI and you book a standalone flight ticket — directly on an airline website or via an OTA that charges you per-ticket — zero TCS is collected regardless of the amount. If you purchase a packaged holiday through an Indian travel agent (holiday package with bundled flights, hotels, and tours) worth say ₹2,00,000, the agent may collect TCS at 2% = ₹4,000. This amount is credited to your PAN and is fully refundable during your Indian income tax filing if your overall tax liability is lower — but NRIs with no Indian taxable income may find the refund process cumbersome, as it requires filing an Indian ITR. The cleanest solution: book flights and hotels separately to avoid the tour-package TCS trigger altogether.

7. Best Payment Strategy: NRE Card vs Indian Credit Card vs Wise vs Niyo

The optimal payment method for NRI international flight bookings in 2026 depends on three factors: the booking currency (INR vs foreign currency), your existing card portfolio, and whether you need mile-earning potential. For most NRIs, a zero-forex fintech card (Niyo Global or Wise) used with the airline's local currency payment option delivers the lowest total cost — saving ₹1,500–₹7,000 on a typical India–Europe fare versus a standard NRE debit card.

True Cost = Fare in INR + Forex Markup Fee + DCC Surcharge (if applicable)

Worked example: A Dublin–Delhi (DUB–DEL) round trip fare on Emirates priced at €1,200 (approximately ₹1,12,000 at mid-market rate on 1 July 2026):

- Standard NRE debit card (3.5% + 18% GST = ~4.13% effective): ₹1,12,000 + ₹4,626 = ₹1,16,626 total cost

- HDFC Regalia Gold NRI Credit Card (2.0% + GST = ~2.36%): ₹1,12,000 + ₹2,643 = ₹1,14,643 total cost

- IDFC FIRST WOW! NRI Card or Niyo Global (0% markup): ₹1,12,000 + ₹0 = ₹1,12,000 total cost

| Payment Option | Forex Markup | Reward Points on Flights | OTP Abroad? | Best For | Key Con |

|---|---|---|---|---|---|

| NRE Debit Card (HDFC / ICICI / SBI) | 3.5% + GST | None typically | App push OTP (if enabled) | Quick fallback option | High forex cost; daily limits may be low |

| HDFC Regalia Gold NRI Credit Card | 2.0% + GST | 4 reward points per ₹150 | App push OTP | Frequent flyers wanting points | ₹2,500 annual fee; forex markup still applies |

| IDFC FIRST WOW! NRI Credit Card | 0% | 3x on travel spends | App OTP / email OTP | Zero-cost international bookings | Requires IDFC FIRST NRE account; FD-backed |

| Niyo Global Zero Forex Card | 0% | Niyo Coins (limited value) | Email OTP / in-app | Best for occasional international bookings | Card must be loaded in advance; limited lounge access |

| Wise Multi-Currency Card | 0% (mid-market rate) | None | Email / app OTP | Multi-currency holders (EUR, GBP, AED) | Small conversion fee above monthly free limit (~2%); not accepted on all Indian OTAs |

Point of Sale Arbitrage: Does Booking Currency Make a Difference?

Yes — booking your ticket on an airline's regional website in local currency (e.g., Emirates UAE site in AED, Air India India site in INR) can produce meaningfully different base fares for the same flight and dates, independent of any forex markup. This is because airlines use different fare inventory and pricing algorithms by Point of Sale (PoS) region. An Air India DUB–DEL ticket booked on the Indian site (airindia.com/in) in INR may price at ₹52,000, while the same ticket on the .com international site in EUR might convert to ₹56,000 at the card network rate. Always check two or three PoS options — Indian site in INR, the site of the airline's home country, and the site of your country of residence — before committing to a booking.

NRIs using an NRE debit card can legitimately use the Indian site PoS since the card is denominated in INR — the card will process an INR transaction with no cross-currency markup. This alone can save ₹3,000–₹8,000 on a typical India–Europe round trip compared to booking on a foreign-currency site.

Fintech Options vs Bank Cards for Flight Booking: Full Comparison

Beyond the cards in the table above, NRIs frequently ask about BookMyForex multi-currency cards and the Jupiter/Fi zero-forex debit cards. BookMyForex cards let you lock in forex rates in advance for currencies like EUR, GBP, and USD — useful if you want price certainty on a fare quoted in foreign currency. However, they require loading the exact amount, and unspent foreign balance must be reconverted on return, potentially at a less favourable rate. Jupiter and Fi provide zero-markup debit cards for resident Indians but are not available to NRIs with foreign addresses. The bottom line for NRIs based in Ireland or the UK: Wise (which fully supports international residents with Indian-origin accounts) or Niyo Global remain the two most practical zero-forex options for flight booking as of July 2026.

On-the-Ground Insight: "I used to just pay on the airline website with my HDFC NRE debit card and not think about it. After reading about forex markup I calculated I'd paid an extra ₹18,000 over 3 flights in 2025 — just in bank charges. I got the IDFC FIRST WOW! card linked to my NRE account. Zero markup. The application was online, took about 10 days. The card works on Air India, Emirates, and MakeMyTrip without any OTP trouble. I wish I'd switched years ago." — Vikram S., Dublin 4, IT Professional, Ireland since 2022

Compare live fares on your next flight to India

Now you know the best payment strategy — find the best fare to match. Our monthly fare calendar tracks DUB–DEL, DUB–BOM, DUB–BLR, and Dublin to every major Indian city so you book at the right price, not just the right time.

All information in this article is based on publicly available official sources, bank schedule of charges, RBI master circulars, and FEMA regulations as of July 2026. Forex markup percentages, transaction limits, TCS rates, and OCI rules are subject to change. Always verify current rates and conditions directly with your bank, the RBI, or the OCI Services portal before booking. MyFlightOffers is not affiliated with any bank or financial institution mentioned. This article does not constitute financial, tax, immigration, or legal advice.

- NEW Dublin to Delhi: Best Indian Bank Card Offers 2026 — HDFC, ICICI, and Axis Bank card deals on DUB–DEL fares, with exact discount codes and validity dates.

- How to Transfer Indian Credit Card Points to Airline Miles (2026) — Move HDFC Regalia, ICICI Emeralde, and Axis Atlas points to Air India Flying Returns, IndiGo 6E Rewards, and more.

- HDFC Credit Card Flight Offers 2026 — Full breakdown of Regalia Gold, Infinia, and Diners Club Black travel benefits for Indian passengers.

- Axis Bank Credit Cards Flight Booking Guide 2026 — Atlas, Vistara, and Magnus card benefits for NRIs booking India and international flights.