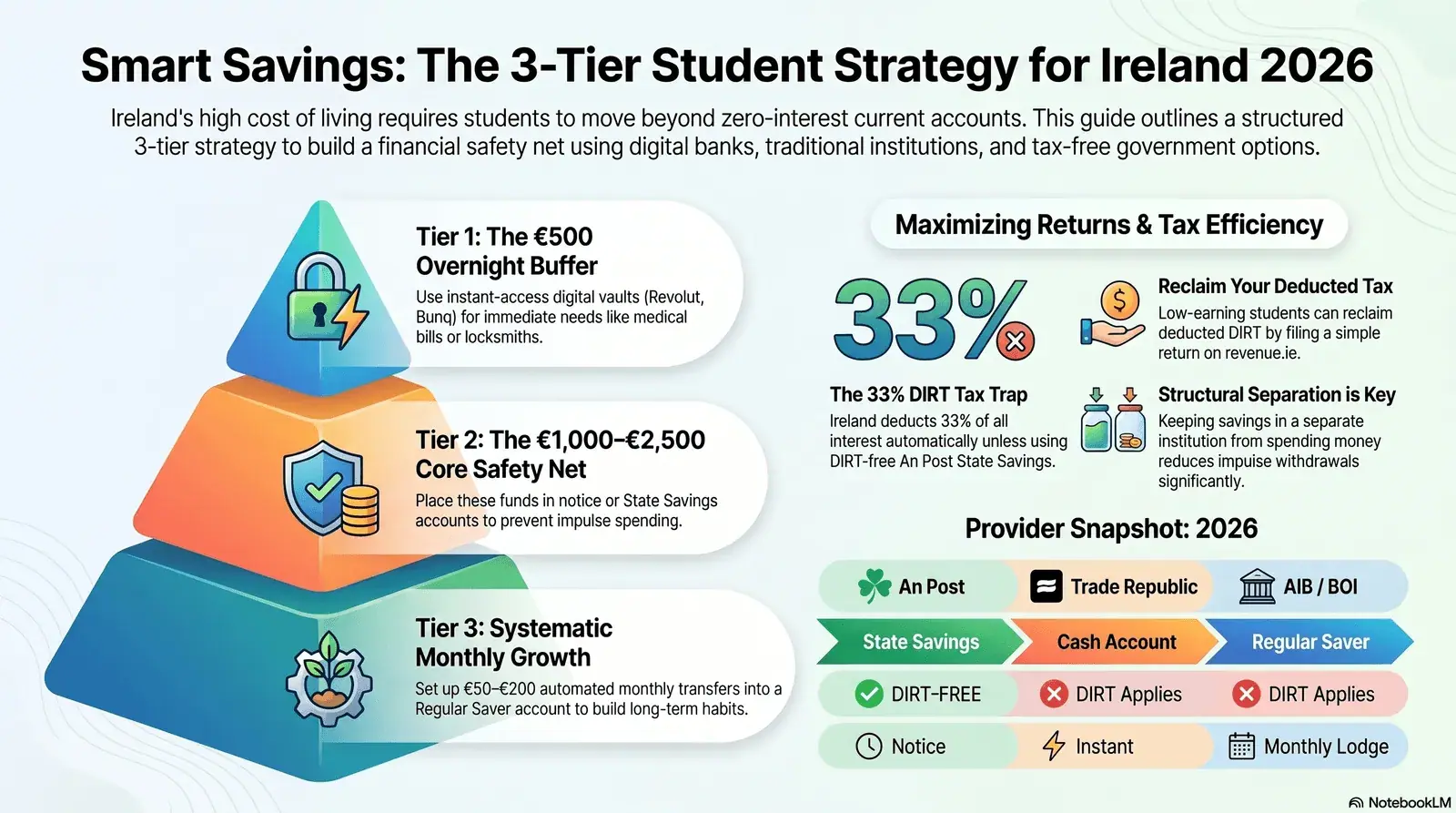

- DIRT costs you 33% of every euro of interest: a 2.0% AER account pays you 1.34% after tax — but An Post State Savings and certain credit union accounts are DIRT-free, making them the highest real-return options for students.

- Separate your emergency fund structurally: keep Tier 1 (€500 overnight buffer) in an instant-access digital vault (Bunq, Trade Republic, or Revolut Savings) and Tier 2 (€1,000–€2,500) in a notice account — the friction stops impulse withdrawals.

- Low-income students can reclaim DIRT: if your total Irish income falls below the personal tax credit threshold, file a return on Revenue's myAccount to get the deducted DIRT refunded directly to your bank account.

🏦 Best instant-access savings

Bunq Easy Savings / Trade Republic Cash

EU-licensed · Instant withdrawal · DIRT applies

🇮🇪 Best government-backed option

An Post State Savings

100% Irish Government backed · DIRT-free returns

🏛️ Best traditional bank saver

AIB Online Regular Saver

Structured monthly saving · Competitive AER

💸 DIRT rate (2026)

33% on all savings interest

Deducted automatically · Low earners can reclaim via

revenue.ie

12 questions answered in this guide

- The 2026 student financial reality check

- Why your emergency fund needs its own home

- How do notice accounts and savings accounts work in Ireland?

- DIRT — Ireland's savings tax and how students can reclaim it

- The 2026 provider showdown — digital challengers

- The 2026 provider showdown — traditional banks

- An Post State Savings — the government-backed option

- Credit unions — Ireland's overlooked student option

- Full provider comparison table

- Fine print traps to avoid

- The 3-tier emergency fund strategy

- Opening an account as an international student

📈 Student Savings Yield & DIRT Tax Calculator

Estimate your annual savings growth, calculate the interest you'll earn, and see the impact of Ireland's 33% DIRT tax.

💰 12-Month Savings Projections

The 2026 Student Financial Reality Check

Dublin rents for a shared room average €900–€1,500 per month. Groceries, transport, and course materials absorb whatever is left. Students managing on part-time wages or remittances from home cannot afford financial surprises — a broken laptop, an unexpected medical bill, or a flight home in an emergency — without a dedicated cushion that is safe, accessible, and not silently losing purchasing power.

The problem is that most students park any surplus in the same current account they spend from. That account earns effectively zero interest, there is no psychological barrier to spending it, and every week of inflation quietly erodes its real value. In 2026, with ECB benchmark rates meaningfully above the near-zero levels of 2021–22, a properly chosen savings vehicle can earn 1.5% to 2.5% AER on money you were earning nothing on before. For a €2,000 emergency fund, that is €30–€50 per year — small in absolute terms, but the habit and structure it creates are the real value.

The European Central Bank began cutting interest rates from its 2023 peak of 4.0% in June 2024. Rates have continued downward since then. By mid-2026, the ECB deposit facility rate is estimated in the 1.75–2.25% range. Irish retail savings rates track this benchmark — meaning returns are lower than the 2023–24 peak but still meaningfully positive. The comparisons in this guide use indicative ranges; always verify current rates directly with each provider before opening an account.

Why Your Emergency Fund Needs Its Own Home

The single most effective student savings technique is structural separation — keeping your emergency fund in a different account, at a different institution, from your spending money. Research in behavioural economics consistently shows that even a minor barrier (logging into a separate app, waiting for a transfer, giving notice) significantly reduces impulse withdrawals on non-emergencies.

The target for a student safety net in Ireland in 2026 is €1,500 to €3,000 — enough to cover one to two months of rent and basic living expenses if income is interrupted. Students arriving from India, China, or other countries with parents sending money through remittance channels should fund this buffer on arrival, before any discretionary spending begins.

How Do Notice Accounts and Savings Accounts Work in Ireland?

Irish savings accounts divide into three main types:

- Instant-access accounts: Withdraw at any time with no notice or penalty. Usually offered digitally by neobanks or as current-account savings "pots." Rates are competitive in 2026 but typically slightly lower than notice accounts.

- Notice accounts: You must notify the bank a fixed number of days (typically 7 to 90 days) before withdrawing. When you request a withdrawal, the timer starts and the money arrives when the period closes. This friction protects genuine emergency funds from casual dipping. Offered by AIB, Bank of Ireland, and Permanent TSB.

- Regular saver accounts: Require a set monthly lodgment (usually €50–€500) and restrict or penalise ad-hoc withdrawals. Higher rates reward consistent saving behaviour. Best for students who want to build savings methodically over an academic year.

DIRT — Ireland's Savings Tax and How Students Can Reclaim It

DIRT (Deposit Interest Retention Tax) is a 33% tax that Irish financial institutions automatically deduct from any interest you earn on savings deposits before crediting it to your account. If your savings account advertises 2.0% AER, you receive 1.34% AER after DIRT. You do not pay it yourself — the bank handles the deduction — but it is real money that reduces your return.

DIRT applies to essentially all interest-bearing deposit accounts held with Irish banks and EU neobanks operating in Ireland. The main exceptions are An Post State Savings products and certain credit union accounts, both of which offer DIRT-free returns.

DIRT Maths on a €2,000 Student Emergency Fund

Gross interest at 2.0% AER = €40.00 / year

DIRT at 33% = − €13.20

Net interest credited to your account = €26.80 / year

─────────────────────────────────────────

An Post State Savings at equivalent gross rate = €40.00 / year (DIRT-free)

Annual DIRT saving by choosing State Savings = €13.20

How Students Can Reclaim DIRT Paid

If your total Irish income is low enough that you owe no income tax after applying your standard personal tax credits, you may be entitled to a refund of the DIRT your bank deducted. The process is straightforward but requires a PPSN and registration on Revenue's myAccount:

- Register for Revenue myAccount at revenue.ie using your PPSN, mobile number, and either an Irish bank account or a passport or driving licence.

- At year end, request your bank statement showing interest earned and DIRT deducted — most banks provide this digitally.

- File an annual income tax return (select "Review your tax" in myAccount). Enter the DIRT amount from your bank statement.

- If your income tax liability for the year is nil (as is common for students earning only part-time income well below personal credit thresholds), Revenue will refund the DIRT directly to your bank account.

Students on Stamp 2 who spend more than 183 days in Ireland in a tax year are ordinarily Irish tax-resident for that year. Tax residency affects both your PPSN obligation and your entitlement to Irish personal tax credits. The specific rules for DIRT refund eligibility for non-EU students vary. Always verify your position directly at revenue.ie/DIRT or via a Citizens Information Centre before filing.

The 2026 Provider Showdown — Digital Challengers

Digital banks and EU neobanks operating in Ireland typically offer the most accessible instant-access savings products for students, with no minimum deposit, strong mobile apps, and competitive rates. All are covered by EU deposit protection up to €100,000 under their home-country scheme.

Bunq Digital · EU Licensed

Bunq holds a Dutch banking licence passported across the EU, meaning Irish residents have the same legal protections as with any European regulated bank. The Easy Savings feature (or equivalent current product name — check bunq.com for the latest) credits interest regularly to your account and is fully digital. Note that Bunq's higher-rate savings features may require a paid account tier; the free tier offers lower rates. Students should calculate whether the subscription cost is justified by the additional interest on their balance before upgrading.

Revolut Digital · Irish HQ

Revolut is headquartered in Dublin and holds a Lithuanian banking licence operative across the EU, with Irish deposit protection applying to balances. The Savings Vaults feature allows students to ring-fence money from their main spending balance within the same app. Rates increase with account tier — Standard accounts earn a lower rate; Premium, Metal, and Ultra accounts earn progressively more. For students on a budget, the Standard tier savings rate is modest but beats zero in a current account. Revolut's Round-Up feature automatically moves spare change (the difference between your spend amount and the next euro) into your savings vault, building the habit without conscious effort.

Trade Republic Digital · EU Licensed

Trade Republic operates across the EU under its German banking licence and is available to Irish residents. Its cash savings feature applies interest to uninvested cash balances at a competitive rate for all account holders, including those on the free tier. For students who want a savings account separate from their main banking app without paying subscription fees, Trade Republic is one of the stronger options in Ireland in 2026. Check current rates at traderepublic.com/ie.

The 2026 Provider Showdown — Traditional Banks

Ireland's main retail banks offer structured savings products that suit students who want a formal regular saving habit and a clear separation from their digital spending accounts.

AIB Online Regular Saver Traditional Bank

AIB's Online Regular Saver requires a monthly lodgment between €10 and €1,000 and offers one of the more competitive regular saver rates among Ireland's main banks. The structured nature — you commit to a monthly deposit — makes it ideal for students who receive a predictable income from part-time work or a parental remittance. Check the current rate at aib.ie/savings.

Bank of Ireland Regular Saver Traditional Bank

Bank of Ireland's Regular Saver allows lodgments from €1 to €1,000 per month. The bank also offers demand deposit accounts for more flexible access. Existing Bank of Ireland student current account holders can link a savings account through the mobile app and set up automated monthly transfers from their current account. Rates and specific products change — check bankofireland.com for current terms.

Permanent TSB (PTSB) Traditional Bank

PTSB offers both demand deposit (instant access) and notice-based savings accounts. Their online savings products can be opened and managed entirely digitally. For students who already hold a PTSB current account, switching surplus funds into a linked savings account is one of the simplest ways to start earning interest. Current rates are available at permanenttsb.ie/savings.

All three main Irish retail banks pay effectively zero interest on standard current account balances. Every week your emergency fund sits in an AIB, Bank of Ireland, or PTSB current account rather than a linked savings account is money you are giving up. Moving it takes under five minutes in each bank's app.

An Post State Savings — The Government-Backed, DIRT-Free Option

An Post State Savings products are the only mainstream DIRT-free savings option available to all Irish residents, including international students on Stamp 2. Returns are exempt from DIRT because they are backed directly by the Irish Government — the same sovereign credit that backs Irish government bonds. This is the safest savings vehicle available in Ireland in absolute terms.

The product range at statesavings.ie includes:

- Deposit Account: Instant-access savings with a notice option. DIRT-free. Minimum €50. Best for students who want accessible, government-backed savings in a single product.

- Prize Bonds: Bonds entered into weekly prize draws instead of earning regular interest. DIRT-free. Minimum €25. The "interest" comes as tax-free prizes. Not a guaranteed return — but the capital is fully protected.

- Savings Bonds: Fixed 3-year term with a guaranteed fixed return. DIRT-free. Not suitable for an emergency fund but useful for known future costs (end of degree year, travel home after graduation).

- Savings Certificates: 5.5-year fixed term, DIRT-free. Only appropriate for students at the beginning of a long programme who have a surplus they genuinely will not touch for years.

Credit Unions — Ireland's Overlooked Student Option

Ireland has one of the highest credit union membership rates in the world, and many universities have an associated credit union on or near campus. Credit unions are member-owned cooperative financial institutions and are regulated by the Central Bank of Ireland. They offer savings accounts (called share accounts) with competitive interest, and savings interest may be exempt from DIRT in certain structures — verify with your specific credit union.

- Campus credit unions: Check whether your university has a credit union — many do. Examples include credit unions associated with UCC, University of Galway, and TU Dublin campuses.

- Community credit unions: Any person living in a credit union's common bond area (typically a geographic area or employer group) can join. International students living in a Dublin, Cork, or Galway residential area typically qualify for at least one local credit union.

- Find your nearest credit union: Use the Credit Union Locator at creditunion.ie.

Credit union savings accounts (share accounts) typically require you to maintain a minimum share balance before accessing loans — a different use case from an emergency fund. DIRT exemption status varies by credit union and product structure. Always confirm specific rates, DIRT treatment, and withdrawal terms with the individual credit union before opening an account.

Full Provider Comparison Table (2026)

Interest rates fluctuate with ECB monetary policy and individual provider decisions. The figures below represent approximate available ranges for mid-2026 based on publicly available information. Always verify the current rate directly on the provider's official website before opening any account. Past rates are not indicative of future rates.

| Provider | Account Type | Approx. Gross AER | After DIRT (33%) | Access | DIRT Status | Min. Balance |

|---|---|---|---|---|---|---|

| Bunq | Easy Savings (paid tier) | ~1.71%–2.0% | ~1.15%–1.34% | Instant | DIRT applies | €1 |

| Revolut | Savings Vaults (Standard) | ~1.0%–1.5% | ~0.67%–1.0% | Instant | DIRT applies | €1 |

| Revolut | Savings Vaults (Metal/Ultra) | ~2.0%–2.49% | ~1.34%–1.67% | Instant | DIRT applies | €1 |

| Trade Republic | Cash (all accounts) | ~1.75%–2.0% | ~1.17%–1.34% | Instant | DIRT applies | €1 |

| AIB | Online Regular Saver | ~2.0%–2.5% | ~1.34%–1.68% | Regular (monthly lodge) | DIRT applies | €10/month |

| Bank of Ireland | Regular Saver | ~2.0% | ~1.34% | Regular (monthly lodge) | DIRT applies | €1/month |

| PTSB | Online Demand / Saver | ~1.5%–2.0% | ~1.0%–1.34% | Instant / Notice | DIRT applies | €1 |

| An Post State Savings | Deposit Account | Varies (check statesavings.ie) | Full rate — DIRT-free | Notice | ✅ DIRT-FREE | €50 |

| An Post Prize Bonds | Weekly Prize Draw | Prizes (not guaranteed) | Capital guaranteed · DIRT-free prizes | Instant (capital) | ✅ DIRT-FREE | €25 |

| Credit Union | Share / Savings Account | Varies by credit union | Varies — verify DIRT status | Varies | Varies | Varies |

Fine Print Traps to Avoid

1. Subscription fees that eat your interest

A Revolut Metal plan costs approximately €13.99 per month (check revolut.com/ie for current pricing). On a €2,000 savings balance at 2.0% AER, your annual gross interest is €40. A €167.88 annual subscription fee loses you money before you earn a cent. Only upgrade to a paid tier if your total balance is large enough that the additional interest outweighs the subscription cost — calculate before you commit.

2. Introductory rates that collapse after 12 months

Some banks offer high introductory rates on new savings accounts that drop sharply after the promotional period. Read the rate schedule in full, not just the headline rate on the advertisement. A 3.0% introductory rate falling to 0.5% after six months is worse over a year than a stable 1.8% account with no introductory window.

3. Locking all your money in a notice or fixed account

A genuine emergency — a medical bill, a flight home, a security deposit for a new room — cannot wait 30 or 90 days for a notice account. Never put 100% of your emergency fund into an account with a notice period. Always maintain an instant-access buffer of at least €300–€500 that can be accessed the same day.

4. Choosing An Post savings for short-term needs

An Post's Savings Bonds and Savings Certificates are fixed-term products. Withdrawing before the maturity date may result in a significantly reduced or zero return. The State Savings Deposit Account is the appropriate product for accessible, DIRT-free emergency savings. Do not conflate the fixed-term products with flexible savings.

5. Ignoring the DIRT refund opportunity entirely

Most students never claim DIRT back because they do not know they are entitled to. If your total Irish income in a tax year is below the threshold at which income tax is payable after personal credits, you have a legal entitlement to reclaim the DIRT your bank deducted. The process is free, fully digital via revenue.ie, and takes approximately 20 minutes to set up for the first time.

The Three-Tier Emergency Fund Strategy

The most effective student savings structure splits your emergency fund across three tiers by access speed and interest rate, rather than holding it all in a single account.

Tier 1 — Instant Emergency Buffer

Account type: Instant-access digital savings vault (Bunq, Revolut Vault, or Trade Republic Cash) — separate from your main spending balance within the same app. This is your overnight emergency fund for medical prescriptions, a locksmith, or a same-day transport cost. It earns whatever rate your chosen neobank pays, which beats zero in a current account.

Tier 2 — Core Safety Net

Account type: An Post State Savings Deposit Account (DIRT-free, government-backed) or a traditional bank notice account with 7–30 day notice. This is for genuine financial crises: a month's rent gap, an unexpected course fee, a flight home. The notice delay is deliberate — it stops you touching it for non-emergencies while your Tier 1 buffer handles smaller costs.

Tier 3 — Systematic Monthly Saving

Account type: Regular Saver (AIB, Bank of Ireland, or PTSB) set up with an automatic standing order from your current account. This builds the fund over time and earns the higher rates regular savers typically offer. Enable the Round-Up feature on your spending card (Revolut or Bunq) to add spare change automatically on top. Once the Tier 3 balance reaches €1,500, move the surplus to Tier 2.

Opening a Savings Account as an International Student in Ireland

International students on Stamp 2 can open savings accounts in Ireland, but the requirements vary by institution. Here is the practical sequence:

Step 1: Get your PPSN

A Personal Public Service Number (PPSN) is required by most Irish banks and by Revenue for DIRT refund claims. Apply in person at a Department of Social Protection Intreo Centre near you. Bring your passport, your university enrollment letter, and proof of your Irish address (a utility bill, a bank statement addressed to you at your Irish address, or a letter from your accommodation provider).

Step 2: Open your current account first

Most savings accounts in Ireland require a linked current account at the same institution. If you do not already have an Irish bank account, the fastest options are neobanks: Revolut can be set up before you arrive using a home-country address, then updated with your Irish address. For a high-street bank account, visit an AIB branch or Bank of Ireland branch with your passport, enrollment letter, and Irish address proof.

Step 3: Open your savings or notice account

Once you have a current account and a PPSN, opening a savings account is typically done through your bank's mobile app in under ten minutes. For An Post State Savings, you can apply online at statesavings.ie or at any An Post branch with your passport and PPSN.

Step 4: Register for Revenue myAccount

Set up your Revenue myAccount at revenue.ie so that you can file a tax return at year end and claim back any DIRT you are entitled to. This takes 10 minutes and prevents you losing money you are legally owed.

- Valid passport (photo page)

- University enrollment letter or student ID card

- Proof of Irish address (utility bill, bank letter, or letter from accommodation provider dated within 3 months)

- PPSN (required for most bank savings accounts and DIRT claims)

- Stamp 2 immigration permission (some banks may ask to see this)

Frequently Asked Questions

What is the best savings account for international students in Ireland in 2026?

For instant-access savings, Bunq Easy Savings or Trade Republic Cash are the most accessible options with competitive rates and no minimum deposit. For DIRT-free safety, the An Post State Savings Deposit Account (minimum €50) is the best risk-free option. For structured monthly saving, an AIB or Bank of Ireland Regular Saver offers a higher rate in exchange for consistent monthly lodgments. Most students benefit from holding all three as part of the 3-tier strategy above.

Can I reclaim DIRT if I am an Indian or Chinese student in Ireland?

Potentially yes, if you are Irish tax-resident for the year (typically the case for students spending more than 183 days in Ireland) and your total Irish income — from part-time work and any other taxable Irish sources — is low enough that income tax after personal credits is nil. Verify your specific situation at revenue.ie or via a Citizens Information Centre. Citizens Information is free, walk-in, and available in Dublin, Cork, Galway, and Limerick.

Do I need a PPS Number to open a savings account in Ireland as an international student?

Most traditional Irish banks require a PPSN to open any account. Neobanks such as Revolut and Bunq may allow account opening without a PPSN initially, but you will need one for any DIRT reclaim, for Irish tax compliance, and for many employer payroll processes. Apply for your PPSN as soon as you arrive at a local Intreo Centre.

Is my money safe in Bunq or Revolut if something goes wrong?

Bunq is licensed by the Dutch central bank (DNB), so balances up to €100,000 are protected under the Dutch Deposit Guarantee Scheme. Revolut holds a Lithuanian banking licence; balances up to €100,000 are protected under the Lithuanian state deposit insurance scheme. Both schemes are EU-standard. An Post State Savings are backed directly by the Irish Government — the strongest possible sovereign guarantee.

Should I use Revolut or a traditional bank for my student savings?

Revolut is better for flexibility, instant access, Round-Ups, and keeping savings in the same app as your spending. A traditional bank (AIB, Bank of Ireland, PTSB) is better if you want a structured regular saver with a disciplined monthly lodgment and a clear separation from your spending account at a different institution. Both approaches are valid; the 3-tier strategy in this guide uses both for complementary purposes.

What is the minimum I need to start an emergency fund as a student in Ireland?

There is no minimum — Revolut, Bunq, and Trade Republic all accept deposits of €1 or less. An Post State Savings Deposit Account requires €50 to open. For the emergency fund to be meaningful, aim to build it to at least one month's rent (€500 outside Dublin, €900–€1,500 in Dublin) before allocating money to any other savings goal.

What is DIRT tax and do students in Ireland have to pay it?

DIRT (Deposit Interest Retention Tax) is a 33% tax automatically deducted by Irish banks from interest earned on savings accounts. Yes, students pay DIRT unless they hold a DIRT-exempt account such as An Post State Savings or a credit union share account. Students whose overall Irish income is low enough that they owe no income tax can potentially reclaim DIRT paid through Revenue's myAccount portal at revenue.ie by filing an annual income tax return.

What is a notice account and how does it work for students?

A notice account requires you to give advance written notice - typically 7 to 90 days - before withdrawing your money. You request the withdrawal, the bank starts the notice period, and your funds arrive in your current account when the period closes. For students, this deliberate friction is a feature: it prevents impulse withdrawals for non-emergencies while still offering a higher interest rate than a standard current account.

Are An Post State Savings really DIRT-free?

Yes. An Post State Savings products - including the Deposit Account, Prize Bonds, Savings Bonds, and Savings Certificates - are exempt from DIRT. They are backed by the Irish Government, making them among the safest savings vehicles available to anyone resident in Ireland, including international students. Returns and terms vary by product. Verify current rates and conditions at statesavings.ie.

How do I reclaim DIRT as a student in Ireland?

Register for Revenue's myAccount at revenue.ie, then file an annual income tax return (Form 12 equivalent). If you earned below the threshold at which income tax is payable after personal tax credits, Revenue may refund the DIRT deducted from your savings interest. The process is completed fully online. You need a valid PPSN and your bank interest statements for the tax year.

Can I open a Revolut or Bunq savings account in Ireland as a non-EU student?

Yes. Both Revolut (headquartered in Dublin) and Bunq (Dutch banking licence, passported across the EU) accept residents of Ireland regardless of nationality, including non-EU students on Stamp 2. You will need proof of Irish address and a valid passport. Revolut accounts can often be opened before you arrive in Ireland using a home-country address, then updated when you get your Irish address.

What is the difference between a regular saver and an instant-access savings account?

A regular saver requires you to lodge a fixed amount every month (typically €50 to €500) and usually restricts or penalises withdrawals. It typically offers higher interest rates as a reward for consistent saving behaviour. An instant-access account lets you deposit and withdraw at any time with no notice or penalty, but generally offers a lower rate. Students should hold an instant-access account for emergencies and a regular saver for medium-term goals.

Also planning your journey to Ireland?

Savings strategy sorted. Now find the best flight fare and make sure your Indian bank card is set up for international use before you travel.

Part of the MyFlightOffers International Students series:

- Study in Ireland 2026: Universities, Costs & Flights (Part 1) — universities, tuition fees, GOI-IES scholarships, cost of living, and flights from India and China.

- Finding Affordable Flights from Dublin to Delhi — how to fly home during holidays, cheapest booking windows, and baggage allowance comparison.

- Best HDFC Bank Cards for Flights & Travel 2026 — if you are using an Indian credit card to book your flight to Ireland.

- Best SBI Credit Cards for Flights & Travel 2026 — SBI Miles Elite offers 1.99% forex markup, relevant for international students booking from Ireland.

All savings rates, account features, DIRT rates, tax thresholds, deposit protection limits, An Post State Savings terms, credit union features, and provider details described in this article are based on publicly available information from the relevant institutions' official websites, the Revenue Commissioners (revenue.ie), Citizens Information (citizensinformation.ie), the Central Bank of Ireland (centralbank.ie), and An Post (statesavings.ie) as of June 2026. Interest rates fluctuate with ECB monetary policy decisions and individual provider strategies. Tax thresholds, DIRT rates, and PPSN procedures may change annually. Always verify the current rate, terms, and your personal tax position directly with the provider and with Revenue before opening any account or making any financial decision. MyFlightOffers is not affiliated with any bank, credit union, An Post, Revenue, or financial institution mentioned in this article. This article does not constitute financial or tax advice.