- No-cost EMI is not truly free: The bank's interest is absorbed by the merchant as an upfront discount — but processing fees (₹99–₹299), GST on waived interest, and forfeited instant coupons mean the real cost is ₹500–₹2,000 on a ₹30,000–₹60,000 ticket.

- Six banks, four platforms: HDFC, ICICI, Axis, SBI, IDFC FIRST, and Kotak all offer 3–12 month no-cost EMI on at least one of MakeMyTrip, EaseMyTrip, ixigo, or Yatra — with minimum booking amounts of ₹2,500–₹10,000 depending on route type.

- No credit card? Use Bajaj Finserv: The Bajaj Finserv Insta EMI Card works on partner travel platforms for up to ₹3 lakh with tenures up to 60 months — no traditional credit card required, though a processing fee applies.

₹2,500–₹5,000 depending on bank

₹5,000–₹10,000 depending on bank

₹99–₹299 + GST per transaction

3–6 months on most platforms

- How no-cost EMI on flights actually works

- Bank-by-bank comparison: HDFC, ICICI, Axis, SBI, IDFC FIRST, Kotak

- Platform comparison: MakeMyTrip, EaseMyTrip, ixigo, Yatra

- BNPL without a credit card: Bajaj Finserv Insta EMI Card

- Hidden costs of no-cost EMI — the real maths

- NRI strategy: booking from Ireland on Indian EMI

- When to use EMI vs paying outright — decision framework

- Verdict: which bank and platform is best in June 2026

1. How No-Cost EMI on Flights Actually Works

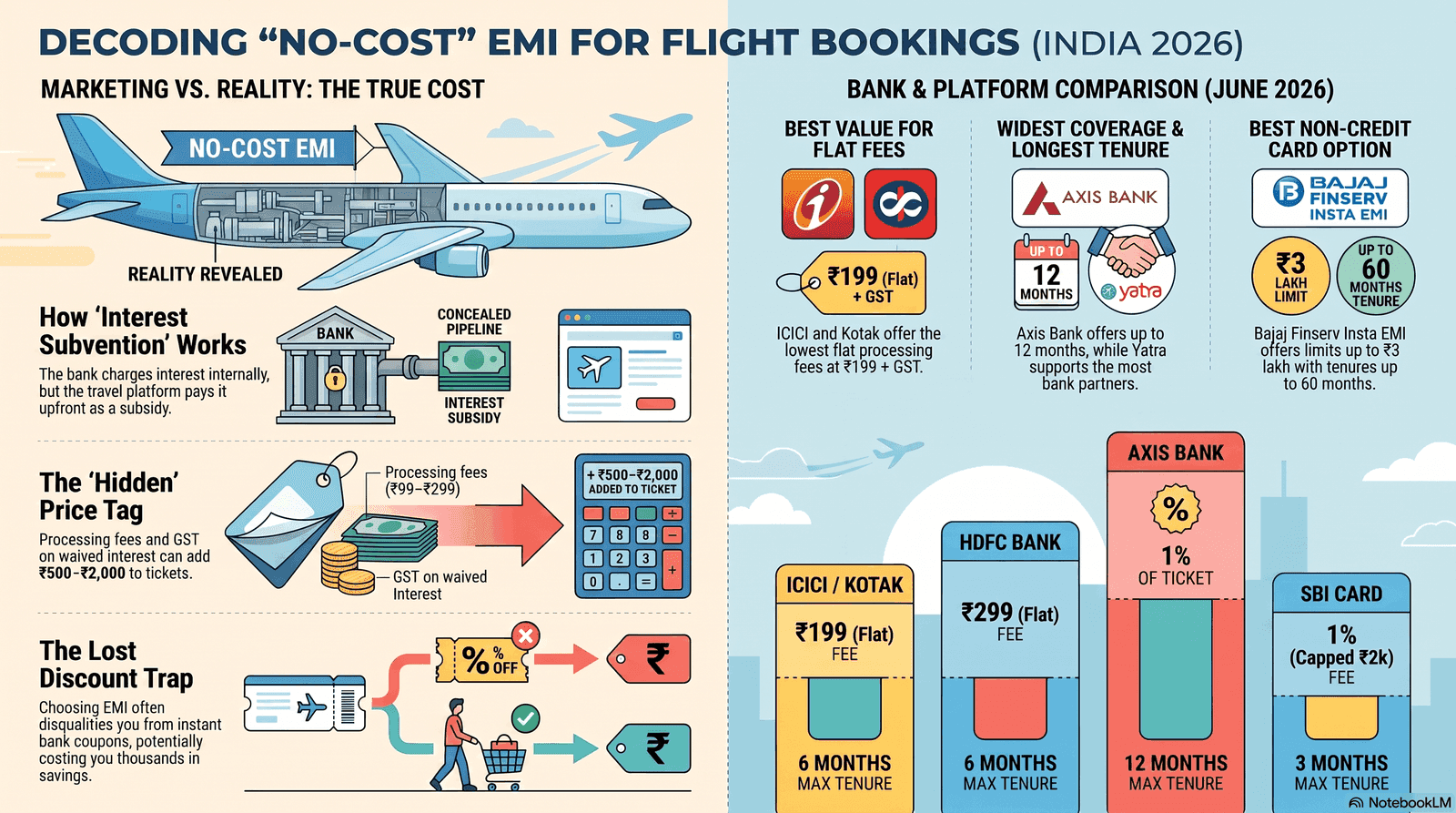

No-cost EMI means the bank books a standard interest-bearing loan internally, but the OTA or airline pays that interest to the bank upfront as a "merchant subsidy" — so your statement shows zero interest charged across the EMI tenure. The mechanism is called interest subvention. You pay the exact ticket price split into equal monthly instalments, nothing more — in theory.

Here is the actual payment flow when you select "No Cost EMI – 3 months" at checkout on MakeMyTrip:

- Your credit card is initially charged the full ticket amount (say ₹54,000) and blocked on your account.

- The issuing bank converts this transaction to a 3-month EMI within 4–7 working days.

- An upfront discount equivalent to the total interest for those 3 months is applied at the time of conversion. This discount is funded by the OTA, not your bank — the OTA effectively pre-pays the interest to your bank on your behalf.

- Your three monthly payments: ₹18,000 + ₹18,000 + ₹18,000. Total paid: ₹54,000. Exactly the ticket price.

The standard interest rate underlying no-cost EMI transactions is typically 15–18% per annum, depending on your bank and card variant. This is what the merchant pays on your behalf. On a ₹54,000 ticket split over 3 months at 15% p.a., the merchant pays roughly ₹670 to your bank. You see none of this cost — but the OTA does, and it factors it into the offer terms (including minimum booking amounts and restricted coupon stacking).

2. Bank-by-Bank Comparison: HDFC, ICICI, Axis, SBI, IDFC FIRST, Kotak

As of June 2026, six banks offer structured no-cost EMI programmes for flight bookings on major Indian OTAs — but the processing fees, maximum tenures, and minimum amounts vary significantly, with HDFC and IDFC FIRST currently the most widely available.

| Bank | Processing Fee | No-Cost Tenures | Min. Booking (Domestic) | Min. Booking (Intl) | Key Platforms |

|---|---|---|---|---|---|

| HDFC Bank | ₹299 + GST (flat) | 3, 6 months | ₹3,000 | ₹5,000 | EaseMyTrip, ixigo, Yatra, MakeMyTrip |

| ICICI Bank | ₹199 + GST (flat) | 3, 6 months | ₹3,000 | ₹10,000 | Yatra, MakeMyTrip, ixigo |

| Axis Bank | 1% of txn (min ₹99) + GST | 3, 6, 9, 12 months | ₹5,000 | ₹10,000 | MakeMyTrip, Yatra, ixigo |

| SBI Card | 1% of txn (max ₹2,000) + GST | 3 months | ₹5,000 | ₹10,000 | Yatra, MakeMyTrip |

| IDFC FIRST Bank | ₹249 + GST (flat) | 3, 6 months | ₹3,000 | ₹5,000 | EaseMyTrip, ixigo, Cleartrip, Yatra |

| Kotak Mahindra | ₹199 + GST (flat) | 3, 6 months | ₹3,000 | ₹5,000 | Yatra, MakeMyTrip |

Sources: Official OTA offer pages (EaseMyTrip, Yatra, ixigo, MakeMyTrip) — verified June 2026. Offers are time-limited and subject to change; always confirm at checkout.

HDFC Bank EasyEMI — Widest Platform Coverage

HDFC Bank's EasyEMI programme is the most widely available no-cost EMI option for Indian flight bookings in 2026, running on EaseMyTrip, ixigo, Yatra, and MakeMyTrip simultaneously, with a flat processing fee of ₹299 + GST per transaction.

The offer was active on EaseMyTrip from 11 April to 30 June 2026 (coupon codes HDFCEMI for 3 months, HDFC6EMI for 6 months). On ixigo, HDFC EasyEMI on credit cards offered up to ₹2,000 off domestic flights and up to ₹7,500 off international flights when booking on EMI. The no-cost window on MakeMyTrip ran through May 2026 with similar discount caps.

One important limitation: HDFC's no-cost EMI offer is valid once per card per category per month. If you booked a domestic flight with HDFC EMI in May, you cannot use the same card for another domestic EMI flight booking until June. Also note that any HDFC instant coupon or cashback offer cannot be combined with the no-cost EMI conversion — the EMI terms state that additional discounts are void if EMI is selected.

ICICI Bank — Strong on OTAs, Lower Processing Fee

ICICI Bank credit cardholders pay a flat ₹199 + GST processing fee for no-cost EMI on flights, making it ₹100 cheaper per booking than HDFC — and the offer runs on Yatra, MakeMyTrip, and ixigo for both domestic and international routes.

On Yatra, ICICI Bank's no-cost 3-month and 6-month EMI offers apply to both domestic flights (minimum ₹3,000) and international flights (minimum ₹10,000). The international minimum is higher than HDFC's ₹5,000, which matters for students booking short regional routes like Mumbai–Colombo or Chennai–Kuala Lumpur. Before booking any international flight with ICICI Bank internationally, confirm that your card has international transactions enabled — ICICI Bank disabled international usage by default on all cards post the RBI 2020 e-mandate order, and you must re-enable it via iMobile or net banking.

Axis Bank — Longest Tenures, Percentage-Based Fee

Axis Bank offers the widest range of no-cost EMI tenures among Indian banks for flight bookings — up to 12 months on select cards — but its processing fee is percentage-based at 1% of the transaction amount (minimum ₹99) plus GST, which makes it expensive on larger bookings.

On a ₹60,000 international flight, Axis Bank's 1% processing fee works out to ₹600 + GST (₹708 total at 18% GST) — versus HDFC's flat ₹299 + GST (₹353 total). For high-value tickets, HDFC or IDFC FIRST is cheaper. However, for students or NRIs booking on a debit card equivalent through Axis Atlas or Axis Magnus, the longer 9- or 12-month tenure allows spreading a Dublin–Delhi fare over the entire academic year. Axis EMI was confirmed available on MakeMyTrip and Yatra as of March 2026.

SBI Card Flexipay — Widest Card Base, Highest Fee on Large Amounts

SBI Card offers a 3-month no-cost EMI through its Flexipay scheme with a fee structure of 1% of the transaction amount (capped at ₹2,000) plus GST — which is the most expensive option for bookings above ₹20,000 but offers zero processing fee on 24- and 36-month tenures.

On a ₹30,000 ticket, SBI's 1% fee = ₹300 + GST = ₹354 total. On a ₹60,000 international ticket, the fee caps at ₹2,000 + GST = ₹2,360 — making it by far the most expensive of the six banks on large-value bookings. However, the Flexipay 24-month and 36-month tenures carry zero processing fees, which is ideal if you are spreading a very large vacation package or multi-city booking over two or three years. The no-cost 3-month EMI was active on Yatra with minimum values of ₹5,000 for domestic and ₹10,000 for international flights.

IDFC FIRST Bank — Best Value for Regular EMI Users

IDFC FIRST Bank's ₹249 + GST flat processing fee combined with a low minimum booking of ₹3,000 on domestic and ₹5,000 on international routes makes it one of the best-value no-cost EMI options for frequent Indian flyers in 2026.

IDFC FIRST was active on EaseMyTrip through June 2026, on ixigo for international routes (up to ₹10,000 off), on Cleartrip, and on Yatra. Notably, IDFC FIRST also integrates with Amazon Pay Later — backed by IDFC FIRST Bank — which offers zero interest for next-month payments for purchases under a threshold.

3. Platform Comparison: MakeMyTrip, EaseMyTrip, ixigo, Yatra

All four major Indian OTAs support no-cost EMI in 2026, but EaseMyTrip has the broadest bank coverage and most active offers during mid-2026, while MakeMyTrip provides the most flexible EMI tenor options ranging from 3 to 24 months.

| Platform | Banks with No-Cost EMI | Tenures Available | Processing Fee Charged By | Offer Validity (June 2026) |

|---|---|---|---|---|

| MakeMyTrip | HDFC, ICICI, Axis, IDFC FIRST, Bajaj | 3–24 months | Bank (charged with first EMI) | Ongoing (bank-specific terms) |

| EaseMyTrip | HDFC, IDFC FIRST, SBI, Kotak | 3, 6 months | Bank (flat fee) | Active through 30 Jun 2026 |

| ixigo | HDFC, ICICI, IDFC FIRST | 3, 6 months | Bank (flat fee) | Active June 2026 |

| Yatra | HDFC, ICICI, Axis, SBI, Kotak, IDFC FIRST, IndusInd, RBL, HSBC | 3–12 months | Bank (flat or percentage) | Ongoing (rolling) |

Yatra has the widest bank coverage. MakeMyTrip has the longest EMI tenures. Data from official OTA offer pages, June 2026.

On MakeMyTrip, the EMI conversion can also be requested post-purchase — any transaction of ₹1,500 or above can be converted to EMI within 30 days of the booking date, for tenures of 3, 6, 9, 12, 18, or 24 months. This is useful when you miss the no-cost EMI offer at checkout but later decide you want to spread the cost.

4. BNPL Without a Credit Card: Bajaj Finserv Insta EMI Card

The Bajaj Finserv Insta EMI Card is the only widely accepted BNPL instrument in India that allows flight bookings on partner travel platforms without a traditional credit card — with credit limits up to ₹3 lakh and repayment tenures up to 60 months.

Unlike a credit card EMI that converts an existing card transaction, the Insta EMI Card is a pre-approved, prepaid credit line issued by Bajaj Finance Limited. At checkout on partner platforms (including MakeMyTrip), you select "Bajaj Finserv EMI" as the payment method, enter your registered mobile number, and choose your tenure. No physical card swipe is required for online purchases.

Eligibility requirements as of June 2026:

- Indian citizen aged 21 to 70 years

- Regular source of income (salaried or self-employed)

- Good credit score (no minimum salary threshold published, but CIBIL score matters)

- Valid PAN card and Aadhaar

A processing fee applies at checkout — the exact amount depends on the product, scheme, and OTA, and is displayed at the time of purchase. Bajaj Finance does not publish a single flat rate for flights; expect ₹99–₹499 depending on the ticket value. The Insta EMI Card is not available to NRIs as it requires Indian residential address and Aadhaar KYC.

Other Active BNPL Options: LazyPay and Simpl

LazyPay (backed by PayU India) and Simpl both operate active BNPL services for Indian travel purchases in 2026, though their flight booking coverage is narrower than Bajaj Finserv.

LazyPay is accepted on select travel platforms and allows you to split purchases into 3 equal instalments interest-free, or opt for a longer pay-later plan at a published interest rate. Simpl similarly offers a 3-payment split on partner platforms including HappyFares. Neither LazyPay nor Simpl reaches the same breadth of airline booking coverage as credit card EMI across MakeMyTrip or Yatra — for large international flight bookings, a bank credit card EMI remains more reliable.

5. Hidden Costs of No-Cost EMI — The Real Maths

No-cost EMI has three real costs that never appear in the marketing headline: a processing fee of ₹99–₹299 per transaction, GST charged on the interest component that the bank waives, and the silent forfeiture of any instant coupon or cashback offer you would have received if you had paid the full amount upfront.

Let us work through a realistic example. You are booking a Delhi–Dublin flight in October 2026 for ₹58,000 on EaseMyTrip using your HDFC Regalia credit card. You see two options at checkout:

- Option A — Pay full amount: Apply coupon HDFCSAVE for 8% off (up to ₹4,000). You pay ₹54,000. No processing fee. Done.

- Option B — No-cost EMI (3 months): No instant coupon (EMI and instant cashback cannot be combined per HDFC offer terms). Processing fee ₹299 + 18% GST = ₹353. Total paid over 3 months: ₹58,353.

True EMI Cost = Ticket Price + Processing Fee + GST on Processing Fee + Forfeited Coupon Value

In this example: ₹58,000 + ₹299 + ₹54 + ₹4,000 forfeited = ₹62,353 effective cost vs ₹54,000 for paying outright. EMI cost you ₹8,353 more.

The comparison flips when you do not have an applicable coupon or if the cash flow benefit matters more than the absolute cost. If your bank account genuinely cannot absorb ₹58,000 in one month without affecting rent or bills, paying ₹19,451 per month across 3 months at a true extra cost of ₹353 is perfectly rational.

What Is GST on Waived Interest?

Even when your bank charges zero interest on a no-cost EMI transaction, RBI rules require that GST at 18% be applied on the interest amount that was waived — meaning you still pay a small GST charge typically of ₹120–₹450 on a ₹30,000–₹60,000 booking.

According to ClearTax's GST guidance on no-cost EMI, the taxable event is the merchant's act of funding the interest subsidy — but the GST incidence falls on the financial transaction leg, which some banks pass through to consumers as a line item on the first EMI instalment. HDFC Bank, for example, may show a small "GST on interest waiver" line of ₹80–₹200 in the EMI breakup sheet displayed at checkout. Always check the breakup before confirming.

On-the-Ground Insight: "I was booking my Hyderabad–Dublin ticket for ₹62,000 on MakeMyTrip in March 2026 and chose the HDFC 3-month no-cost EMI because I thought it was free. I later noticed that the instant ₹3,500 discount I had used on a previous booking was not available when I selected EMI — the T&Cs say EMI and instant discounts cannot be combined. I ended up paying ₹353 more in processing fees and lost ₹3,500 in discount potential. I should have compared both options at checkout instead of just clicking EMI automatically." — Priya R., University of Limerick, MSc Data Science, Sep 2025 Intake

6. NRI Strategy: Booking from Ireland on Indian EMI

NRIs in Ireland can use Indian credit card EMI on OTAs by booking via Indian OTA websites in INR, provided they hold an NRE (Non-Resident External) credit card — NRO cards are restricted to domestic Indian transactions only and cannot be used for cross-border payments.

The key distinction: an NRE credit card is linked to your NRE account (funded from foreign income), can be used internationally, and earns rewards on global spend. An NRO credit card is tied to income earned in India and generally restricted to domestic Indian transactions under RBI's FEMA regulations. If you are accessing MakeMyTrip or Yatra from an Irish IP address and booking in INR using your NRE card, the transaction is processed as a domestic Indian transaction even though you are physically abroad — no forex markup applies.

Popular NRE credit cards available to Indian students and professionals living in Ireland in 2026 include:

- ICICI Bank NRI Sapphiro Credit Card — rewards on international spend, no-cost EMI on partner OTAs

- IDFC FIRST Bank NRI WOW Credit Card — zero forex markup on international transactions

- Kotak NRI Royale Signature Credit Card — reward points transferable to airline miles

How to Access Indian OTA Prices from Ireland

Indian OTA platforms (MakeMyTrip, EaseMyTrip, ixigo, Yatra) do not geo-restrict their prices based on your location, so you can access INR fares and EMI offers from Ireland simply by visiting the Indian version of the website directly.

Step-by-step:

- Go directly to makemytrip.com (not the UK or international version). The site detects your location but defaults to INR if your account is registered with an Indian mobile number.

- Log in with your Indian mobile number OTP. If you no longer have access to your Indian SIM, use your email-based login instead.

- Select your flight. At checkout, choose your Indian NRE credit card as the payment method.

- If the no-cost EMI option appears, check the processing fee, tenure, and whether any applicable instant coupon is being blocked. Compare both options.

- Complete the transaction. Your bank will send an OTP to your registered mobile number — ensure your Indian number is active or that you have forwarded it via an e-SIM or dual-SIM setup.

7. When to Use EMI vs Paying Outright — Decision Framework

Use no-cost EMI when you do not have an active instant coupon that would be forfeited, the processing fee is flat and low (₹199–₹299), and the cash flow relief over 3–6 months is genuinely useful for your budget — otherwise, paying outright with a cashback card typically saves more money.

| Scenario | Recommended Choice | Why |

|---|---|---|

| ₹25,000 domestic flight, active 10% coupon | Pay outright | Coupon saves ₹2,500; EMI processing fee + forfeited coupon = net loss |

| ₹60,000 international flight, no active coupon | 3-month EMI (HDFC or IDFC FIRST) | Only ₹353 processing fee; cash flow relief worth it on large ticket |

| ₹15,000 flight, SBI Card | Pay outright | SBI's 1% fee = ₹150 + GST on a small ticket; not worth it |

| ₹80,000 international package, no credit card | Bajaj Finserv Insta EMI | Only viable option without a credit card; up to 60-month tenure |

| NRI in Ireland, booking India–Europe flight in INR | IDFC FIRST NRI card + EMI | Zero forex markup on NRE card + flat ₹249 fee on IDFC platforms |

| Academic year booking: ₹55,000 ticket, 12-month tenure needed | Axis Bank 12-month EMI | Only bank with confirmed 12-month no-cost tenure for flights |

Decision framework based on processing fee comparison and OTA offer terms, June 2026.

One often-overlooked consideration: when you convert a flight booking to EMI, that amount blocks your credit card's available limit for the full booking amount upfront (₹60,000 is blocked, then gradually released as you pay each EMI). If you have a ₹1 lakh credit limit and block ₹60,000 for a flight EMI, your remaining available credit is only ₹40,000 — which could cause a declined transaction if you need to make another large purchase in the same month. Plan your credit utilisation accordingly.

8. Verdict: Which Bank and Platform Is Best in June 2026

For most Indian travellers booking flights in June 2026, HDFC Bank + EaseMyTrip or ixigo offers the best combination of platform availability, flat processing fee (₹299), and consistent no-cost EMI access — followed closely by IDFC FIRST Bank at ₹249 with broader platform coverage including Cleartrip.

The ideal strategy depends on your specific situation:

- Frequent domestic flyer with HDFC Regalia/Millennia: Use EaseMyTrip + HDFCEMI coupon for 3-month no-cost EMI when no instant cash discount is available. Total overhead: ₹353.

- International flight over ₹50,000, Axis Atlas card: Axis Bank's 1% fee on ₹50,000 = ₹590 + GST. Consider HDFC or IDFC FIRST instead to save ₹237–₹360 on the processing fee alone.

- No credit card at all: Bajaj Finserv Insta EMI Card on MakeMyTrip is your best option — apply for the card 5–7 days before your planned booking to ensure activation.

- NRI in Ireland: IDFC FIRST WOW NRI Card on EaseMyTrip or ixigo gives you zero forex markup plus a flat ₹249 processing fee. Ensure your NRE card's international transactions are enabled before booking.

Find the best fare before deciding on EMI

Compare live fares from Indian airlines and international carriers on MyFlightOffers to see the lowest base price — then decide whether EMI or outright payment makes more financial sense for your booking.

All information in this article is based on publicly available official OTA offer pages, bank websites, and RBI regulatory disclosures as of June 2026. No-cost EMI offers are time-limited, bank-specific, and subject to change without notice. Processing fees, minimum booking amounts, and tenure availability may differ from what is shown here by the time you read this. Always verify the exact terms at checkout before confirming an EMI booking. MyFlightOffers is not affiliated with any bank, OTA, or payment provider mentioned. This article does not constitute financial or tax advice.

- HDFC Credit Card Flight Offers 2026 — Every active HDFC Bank discount, EMI, and cashback offer for domestic and international flights

- Card Tokenisation for Flight Booking India 2026 — How RBI's card-on-file tokenisation rule affects your OTA payment experience

- Transfer Credit Card Points to Airline Miles India 2026 — Convert HDFC, Axis, ICICI, and Amex rewards to frequent flyer miles before booking

- Axis Bank Credit Cards Flight Booking Guide 2026 — Full guide to Axis Atlas, Magnus, and Vistara cards for Indian and international flights