- What it is: A security protocol mandated by the RBI since October 2022 that replaces your 16-digit card number with a merchant-specific digital token.

- Completely free and safe: Tokenization is 100% free and opt-in. Skipped cards are not saved; tokenized cards cannot be compromised if the merchant server is breached.

- No effect on refunds: In case of flight cancellations or modifications, refunds are processed normally back to your original bank account through the card network's vault mapping.

A unique digital code replacing your 16-digit card number

Merchant-specific — mathematically useless anywhere else

100% free, always

RBI-mandated from October 1, 2022 — no hidden charges

No — refunds work identically

Token routes the credit back to your original account

Opt-in — you can skip it

Skip it and you re-enter all card details every booking

- What is the "Secure your card" checkbox and who mandated it?

- What exactly is card tokenization? (The simple explanation)

- Who are the three parties in every tokenized transaction?

- Step-by-step: how tokenization works at flight checkout

- Why flight bookings are higher-risk than other online purchases

- Tokenization vs. no tokenization — what changes for you?

- Does tokenization affect flight refunds or chargebacks?

- Which platforms and card networks support RBI tokenization?

- Managing saved tokens — delete, update, switch devices

- Five card tokenization myths — debunked

1 What Is the "Secure Your Card" Checkbox and Who Mandated It?

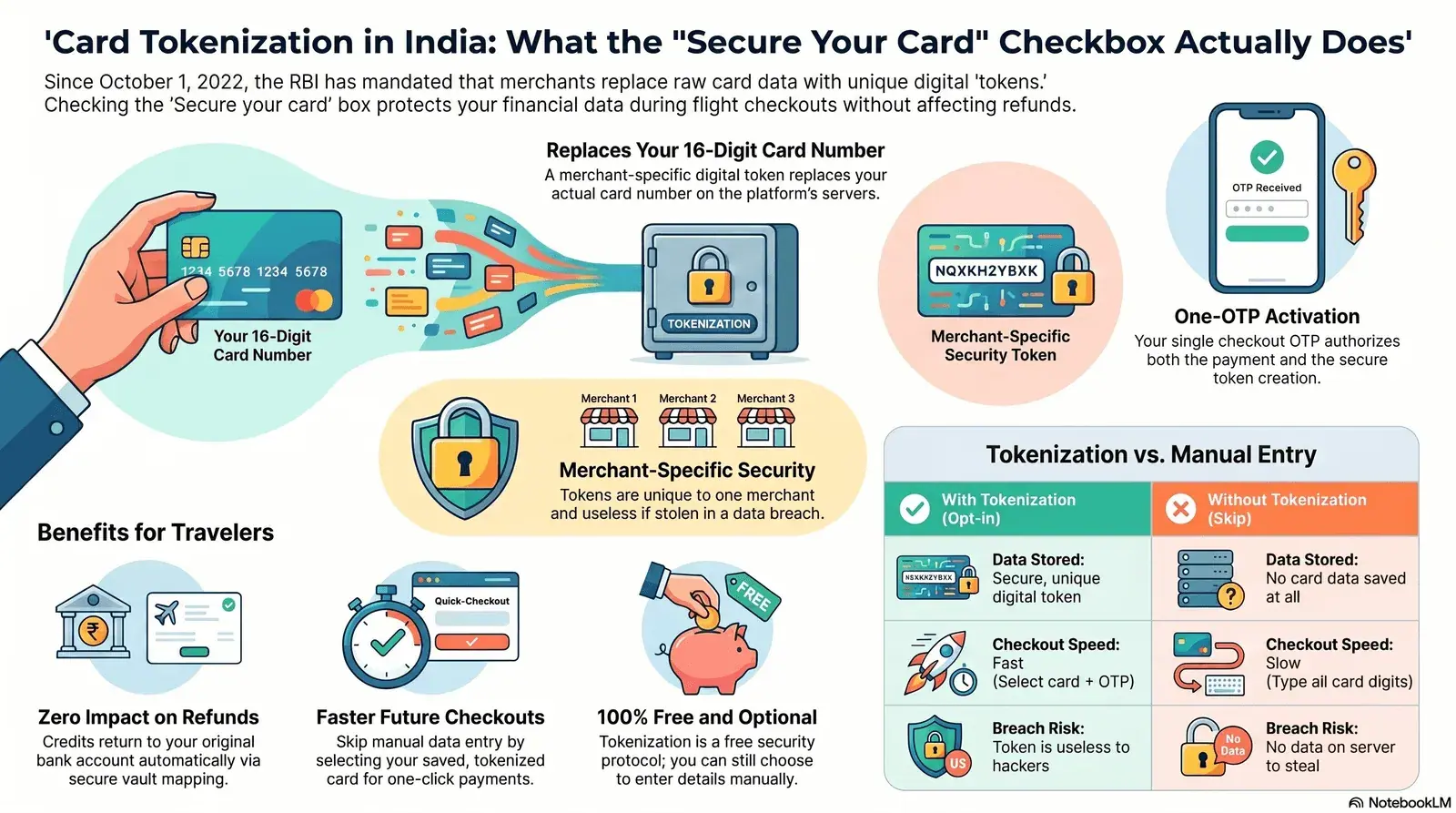

This checkbox is the opt-in trigger for Card-on-File (CoF) tokenization — an RBI-mandated security protocol that permanently replaces your 16-digit card number on that merchant's system with a unique, randomly generated digital code called a token. When you check the box and confirm with an OTP, your card is "tokenized" for that booking platform. From that point, the platform stores only the token — never your real card number.

You will see this checkbox on every major Indian flight booking platform — phrased as "Save card securely as per RBI guidelines," "Tokenize card," or "Secure your card as per RBI mandate." The exact wording varies by platform, but the underlying action is identical.

The Reserve Bank of India issued its original tokenization circular (RBI/2021-22/17) on June 25, 2021, prohibiting merchants from storing raw card data on their servers. After multiple implementation deadline extensions, the mandate became fully and strictly enforceable on October 1, 2022. Since that date, no Indian payment aggregator, payment gateway, or flight booking platform may legally store your actual card number — only the token that replaces it.

2 What Exactly Is Card Tokenization? The Simple Explanation

Card tokenization is the process of replacing your actual 16-digit card number — known as the Primary Account Number (PAN) — with a randomly generated surrogate number called a token that is mathematically linked to your card but cannot be reverse- engineered to reveal it.

Think of it as a coat check at a restaurant. Instead of walking around with your expensive coat (your PAN), you hand it to the attendant and receive a plastic chip (the token). If someone pickpockets your chip, it is useless — it only works at that one coat check counter, and only the counter attendant can exchange it for the real coat. No one else in the building can access your coat with that chip.

In card terms:

- Your actual card number is stored only in the Token Vault — a secure database maintained exclusively by your card network ( Visa, Mastercard, or RuPay / NPCI).

- The booking platform receives and stores only the token — a surrogate number that is unique to your card on that specific platform.

- At payment time, the platform sends the token to the card network, which looks up your real card number in the Token Vault and processes the transaction with your bank.

3 Who Are the Three Parties in Every Tokenized Transaction?

Every tokenized card transaction in India involves three distinct roles, each with a defined responsibility under the RBI framework. Understanding these roles removes the mystery from what happens behind the scenes.

Examples:

MakeMyTrip,

IndiGo,

Air India.

The Token Requestor initiates the tokenization request when you

opt in, receives the token from the card network, and stores it

in place of your real card number. They interact with the token

only — never with your actual PAN after the initial setup.

Examples: Visa (via Visa Token Service), Mastercard (via MDES),

NPCI / RuPay.

The TSP generates the token, maintains the Token Vault (the

secure map between tokens and real card numbers), and acts as

the trusted intermediary in every transaction. They are the only

entity that can convert a token back to a PAN — and only for

authorized transactions.

Examples:

HDFC Bank,

ICICI Bank,

SBI Card,

Axis Bank.

Your bank approves or declines the actual transaction after the

TSP decrypts the token to the real PAN and sends the charge

request. Your bank also sends the OTP that confirms both the

payment and the initial token creation.

4 Step-by-Step: How Tokenization Works During Flight Checkout

The tokenization setup at checkout takes under 30 seconds and requires exactly one OTP from you — the same OTP that authorizes your current payment. Here is every stage, in order:

- You enter your card details at the payment page. Your 16-digit card number, expiry date, and CVV travel securely (via HTTPS and your payment gateway's encrypted connection) to the platform's payment processor. No card data is stored by the merchant at this stage.

- You check the "Secure your card" checkbox. This indicates your consent to tokenize. The platform registers your opt-in with the payment gateway and card network. You will not see this option for the same card again after the process is complete.

- Your bank sends an OTP to your registered mobile number. This single OTP serves dual purpose: it authorizes the current flight booking payment and it approves the creation of the token. One OTP, two actions.

- The card network generates a unique token. Behind the scenes, the payment gateway sends a tokenization request to the card network (Visa, Mastercard, or RuPay). The network generates a merchant-specific token and stores the token-to-PAN mapping securely in the Token Vault.

- The merchant receives and stores only the token. Your actual 16-digit PAN is immediately and permanently removed from the merchant's system. They store the token and display only the last four digits of your card number so you can identify which card is saved.

- All future bookings use the token automatically. The next time you pay on that platform, you select your saved card (shown as last 4 digits), enter a fresh OTP, and the merchant sends the token plus a one-time cryptogram to the card network — which decrypts the token and charges your actual card. You never type your full card details again.

5 Why Flight Bookings Are Higher-Risk Than Other Online Purchases

Flight bookings carry the highest average transaction value and the highest saved-card reuse rate of any consumer e-commerce category in India — making travel platforms the most attractive target for card fraud, and the most critical context in which tokenization applies.

Consider the exposure without the protections tokenization provides:

- An Indian family booking four round-trip tickets to London or Singapore may transact ₹3,00,000 to ₹7,00,000 in a single checkout session.

- A frequent business traveler typically saves the same card on four or five platforms simultaneously — MakeMyTrip, Cleartrip, IndiGo, Air India, and EaseMyTrip.

- Refunds on cancelled or changed bookings take 5–10 business days. During that window, a compromised card can be misused across multiple merchants before the cardholder detects unauthorized transactions.

- Late-night and international flight bookings happen around the clock — outside normal bank-monitoring hours.

Before October 2022, saving a card on five booking platforms meant your raw PAN existed in five separate merchant databases. A single breach at any one platform exposed your card to unauthorized use across all five simultaneously. Tokenization eliminates this systemic risk: even in the worst-case scenario of a platform breach, an attacker receives a merchant-specific token that is cryptographically worthless on any other site or transaction without the matching cryptogram.

6 Tokenization vs. No Tokenization — What Actually Changes for You?

The security difference between opting in and opting out is significant. The practical difference is equally clear: tokenizing makes every future checkout faster and removes the need to re-enter card details on that platform.

| What changes | With tokenization (opt-in) | Without tokenization (skip) |

|---|---|---|

| What the platform stores | A merchant-specific token (worthless without TSP key) | No card data stored — but you cannot save the card at all |

| Future checkout speed | Fast — pick saved card, enter OTP only | Slow — type 16-digit number, expiry, CVV every booking |

| Risk if platform server is breached | Attacker gets a token: useless without cryptogram | No card data on the platform to steal — but no saved card either |

| Refund processing | Automatic via token reverse-mapping to original account | Works normally; may require bank account details in some cases |

| Auto-pay and e-mandates | Supported — recurring charges require tokenization | Not available — recurring charges cannot be set without a token |

| Cost | Free | Free |

| Works across all devices | Yes — token is account-based, not device-based | Irrelevant — no card saved, so re-entry needed on every device |

7 Does Tokenization Affect Flight Refunds or Chargebacks?

No. Tokenization has zero effect on how refunds or chargebacks are processed. If your flight is cancelled, rescheduled, or if you initiate a refund, the credit returns to your original bank account exactly as it would without tokenization — automatically, without any action required from you.

Here is why: when a refund is triggered by the booking platform, they send the token back through the payment gateway to the card network. The network's Token Vault maps the token to your real PAN, and the issuing bank credits the refund to your account. The entire process is invisible to you — no extra steps, no need to enter bank details, no delay caused by the tokenization layer.

Chargebacks — where you formally dispute a transaction through your bank — also work normally on tokenized cards. Your bank retains full transaction records, including the token-to-PAN mapping, for dispute resolution purposes. To raise a chargeback on a flight booking, use your bank's standard process: call customer care, submit via net banking, or raise a dispute through the bank's app. The fact that a token was used in the original transaction does not affect the bank's ability to investigate and resolve the dispute.

8 Which Flight Booking Platforms and Card Networks Support RBI Tokenization?

Since October 1, 2022, all RBI-regulated payment entities processing card transactions in India must support tokenization. In practice, every major Indian flight booking platform is compliant — the "Secure your card" prompt is present across all of them.

| Platform | How "Save card" is phrased | Supported networks | Manage saved cards |

|---|---|---|---|

| MakeMyTrip | "Save card securely as per RBI guidelines" | Visa, Mastercard, RuPay, Amex | My Account → Saved Cards |

| IndiGo | "Save this card" (RBI-compliant tokenization) | Visa, Mastercard, RuPay | My Account → Payment Methods |

| Air India | "Save card as per RBI mandate" | Visa, Mastercard, Amex, RuPay | Manage Booking → Saved Cards |

| Cleartrip | "Securely save card (RBI compliant)" | Visa, Mastercard, RuPay | Profile → Saved Payment Methods |

| EaseMyTrip | "Tokenize card as per RBI guidelines" | Visa, Mastercard, RuPay, Amex | Account → My Saved Cards |

| Yatra | "Save card (secured by RBI tokenization)" | Visa, Mastercard, RuPay | My Profile → Saved Cards |

Which card types are tokenizable?

The RBI framework applies to all card networks operating in India. Every common card type is supported:

- Visa debit and credit cards — tokenized via the Visa Token Service (VTS)

- Mastercard debit and credit cards — tokenized via Mastercard Digital Enablement Service (MDES)

- RuPay cards (debit and credit) — tokenized via NPCI's own token service

- American Express cards — tokenized via Amex's proprietary token service

- Diners Club cards — tokenized where supported by the payment gateway

Prepaid wallets, UPI handles, and net banking do not use card tokenization — the RBI CoF tokenization mandate applies specifically to debit and credit cards bearing a PAN.

9 Managing Your Saved Tokens — Delete, Update, Switch Devices

Your card token is stored by the booking platform, not by your browser, device, or mobile app. Switching phones, clearing browser history, or reinstalling an app has no effect on your saved token — your saved card reappears when you log back into your account on any device. Only explicitly deleting the saved card from your account settings removes the token.

How to delete a saved (tokenized) card

- Log into your account on the booking platform.

- Go to Account Settings → Saved Cards (or Payment Methods).

- Select the card and click "Delete" or "Remove." The platform sends a deletion request to the card network, which removes the token from the Token Vault.

- Once deleted, that merchant no longer has any reference to your card. You will need to re-enter and re-tokenize if you wish to save the card again in the future.

What happens when your card expires?

When your bank issues a renewal card with the same card number but a new expiry date and CVV, most Indian banks and card networks automatically update the expiry associated with your existing token. You will typically see "Card expiry updated" on your saved card without any action from you. If you receive a new card with a completely different card number (not a renewal), you will need to add and re-tokenize the new card on each platform separately.

10 Five Card Tokenization Myths — Debunked

Despite being in force for over three years, several misconceptions about RBI card tokenization persist among Indian cardholders. Here are the five most common — with accurate facts behind each.

Quick-Reference FAQ

What is the "Secure your card as per RBI guidelines"

checkbox?

It is the opt-in for Card-on-File (CoF) tokenization. Checking it

and confirming with an OTP replaces your 16-digit card number with

a merchant-specific token on that platform — permanently.

Is card tokenization free in India?

Yes — always. RBI-mandated and enforceable since October 1, 2022,

with no charge to the cardholder at any stage.

Does tokenization affect flight refunds?

No. Refunds are routed through the token back to your original

bank account automatically. No action is needed from you.

Which flight platforms support RBI tokenization?

All major platforms —

MakeMyTrip,

IndiGo,

Air India,

Cleartrip,

EaseMyTrip, and

Yatra

— are all RBI-compliant.

What happens to my saved token if I switch devices?

Nothing. The token is stored by the platform, not your device.

Your saved card reappears on any device when you log back into

your account.

Can I still book flights without tokenizing?

Yes. You simply re-enter full card details manually at each

checkout. Tokenization is opt-in, not compulsory.

Understand tokenization in context — compare how India's major bank cards earn rewards and handle payments on your next flight booking:

- Indian Card Declined on Foreign Airline Website? Here's How to Fix It (2026 Guide) — RBI's 2020 mandate disabled international usage by default; step-by-step fix for HDFC, ICICI, SBI & Axis cards

- Axis Bank Credit Cards for Flight Bookings 2026 — EDGE Miles, Atlas, Magnus, Travel EDGE Portal & April 2026 partner changes

- Best SBI Credit Cards for Flights & Travel 2026 — Miles Elite, KrisFlyer SBI, IndiGo SBI, 1.99% forex

- Best ICICI Bank Credit Cards for Flights & Travel 2026 — Emeralde Private Metal, MakeMyTrip ICICI, Emirates Skywards

- Airport Lounge Access in India: Complete Credit Card Guide 2026 — DreamFolks vs Priority Pass, spend criteria, guest access

- Kotak Bank Credit Cards for Flight Bookings 2026 — Air+, Air, IndiGo Kotak, forex and transfer ratio analysis

- UPI for International Flight Bookings 2026 — which airlines accept UPI, the new ₹5 lakh P2M limit, NRI setup, and where UPI works abroad

- TCS on International Travel Spend 2026 — What Indian Travelers Must Know Before Booking — Budget 2026 cut TCS on overseas packages to 2% flat from April 2026. Know which transactions trigger TCS, when credit cards are exempt, and how to reclaim it via ITR.

Frequently Asked Questions

What is the 'Secure your card as per RBI guidelines' checkbox I see during flight checkout?

This checkbox is the opt-in for RBI-mandated Card-on-File (CoF) tokenization. When you check it and complete OTP verification, your bank and card network replace your 16-digit card number with a unique digital token specific to that merchant. The merchant stores the token - never your actual card number - making future bookings faster and your card data significantly safer.

Does tokenizing my card affect flight refunds or cancellations?

No. Tokenization has no effect on refunds. When a refund is initiated, the booking platform sends the token back through the payment gateway. The card network's Token Vault maps the token to your original card account, and your bank credits the refund automatically. No extra steps are required from the cardholder.

Which flight booking platforms in India support RBI card tokenization?

All major Indian flight booking platforms are required to comply with RBI tokenization rules since October 1, 2022. This includes MakeMyTrip, Goibibo, IndiGo (goindigo.in), Air India (airindia.in), Cleartrip, EaseMyTrip, and Yatra. The 'Secure your card' prompt appears at checkout when you first save a card on any of these platforms.

What if I do not tokenize my card - can I still book flights in India?

Yes. You can still book flights without tokenizing. If you skip the checkbox, you will need to manually enter your full 16-digit card number, expiry date, and CVV every time you make a booking on that platform. Tokenization is opt-in and strongly recommended for speed and security, but it is never compulsory.

What happens to my saved card token if I switch devices or clear my browser?

Your token is stored by the booking platform, not by your device or browser. Clearing your browser cache, switching phones, or reinstalling the app has no effect on your saved token. Your saved card (identified by the last 4 digits) will reappear when you log back into your account on any device. To remove a token, delete the saved card from within your account settings on that platform.

Now book your next flight with full confidence

You know exactly what the security checkbox does and why your card data is protected. Find the best fare on your route and check out securely.

All information regarding RBI tokenization guidelines, platform implementation details, card network token services, and checkout processes in this article is based on publicly available information from the Reserve Bank of India (circulars RBI/2021-22/17 and subsequent extensions), Visa, Mastercard, NPCI, and official booking platform documentation as of June 2026. Payment platforms update their checkout interfaces periodically. Always verify current implementation details directly with your booking platform or card-issuing bank. MyFlightOffers is not affiliated with any bank, card network, or booking platform mentioned in this article. This article does not constitute financial or legal advice.