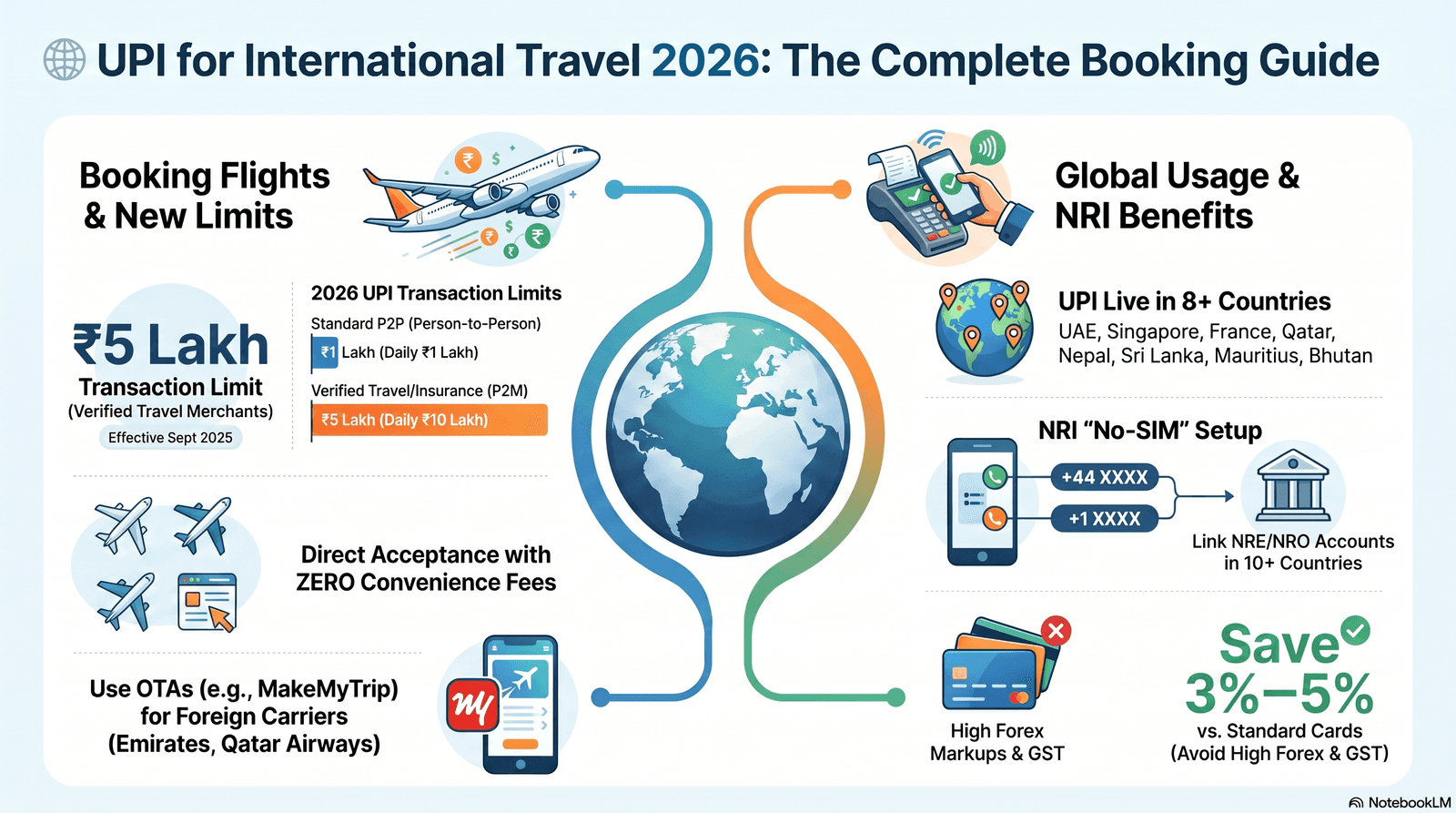

- UPI limit for travel is now ₹5 lakh per transaction (up from ₹1 lakh) for verified merchant categories including flights — effective 15 September 2025 per NPCI.

- Indian airlines accept UPI directly (Air India, IndiGo, Akasa, SpiceJet); foreign carriers (Emirates, Qatar Airways) do not — book them via MakeMyTrip, EaseMyTrip or Paytm instead.

- NRIs in 10+ countries can link NRE/NRO accounts to PhonePe, Google Pay, or Paytm using an international mobile number and pay in INR with zero forex markup.

₹5 lakh per transaction

Effective 15 Sep 2025 — NPCI circular

₹10 lakh per day

For verified travel merchant category

8+ countries (June 2026)

UAE, Singapore, France, Qatar, Nepal, Sri Lanka, Mauritius,

Bhutan

10+ countries

UK, USA, UAE, Singapore, Australia, Canada, Oman, Qatar,

Malaysia, Saudi Arabia

- Which Indian airlines accept UPI for international flights?

- Can I use UPI on Emirates, Qatar Airways, or Lufthansa's website?

- UPI transaction limits for flight payments in 2026

- NRI UPI: how to link your NRE/NRO account and book from abroad

- Where can you use UPI abroad in 2026?

- UPI vs credit card: true cost comparison for international bookings

- Step-by-step: how to pay with UPI before and during travel

1. Which Indian airlines accept UPI for international flights?

All four major Indian airlines — Air India, IndiGo, Akasa Air, and SpiceJet — accept UPI payments with zero surcharge on their own websites and mobile apps for both domestic and international bookings. Air India goes further, actively offering a promo code (UPIPROMO) that delivers up to ₹2,000 off international flight fares when paying by UPI on their app.

Air India's UPI offer, verified on airindia.com as of June 2026, provides a minimum flat ₹300 discount on international flights paid via UPI on the Air India App, rising to up to ₹2,000 depending on the fare and route. The same UPIPROMO code delivers up to ₹2,500 on student fares and up to ₹2,000 per passenger for senior citizens on international routes.

IndiGo accepts UPI via both QR code scan and UPI ID entry on goindigo.in and the IndiGo app. There is no convenience fee on UPI payments. For international legs operated by IndiGo (for example, Bengaluru–Bangkok or Delhi–Kathmandu), UPI works identically to domestic bookings — select UPI at checkout, enter your UPI ID or scan the QR, and authenticate in your UPI app within 60 seconds.

Akasa Air, which launched international operations in 2024 and expanded significantly in 2025–26, supports UPI across all fare types including their international routes. SpiceJet accepts UPI and runs periodic UPI-specific cashback offers through PhonePe and Google Pay, typically ₹100–₹200 cashback on bookings above ₹5,000.

| Airline | UPI on own website? | UPI on app? | International bookings? | Promo / discount? |

|---|---|---|---|---|

| Air India | ✅ Yes | ✅ Yes | ✅ Yes | Up to ₹2,000 off with UPIPROMO |

| IndiGo | ✅ Yes | ✅ Yes | ✅ Yes (intl routes) | Zero convenience fee |

| Akasa Air | ✅ Yes | ✅ Yes | ✅ Yes | Standard cashback via apps |

| SpiceJet | ✅ Yes | ✅ Yes | ✅ Yes (intl routes) | Periodic PhonePe / GPay cashback |

| Air India Express | ✅ Yes | ✅ Yes | ✅ Yes | Zero convenience fee on UPI |

2. Can I use UPI on Emirates, Qatar Airways, or Lufthansa's website?

No — Emirates, Qatar Airways, and Lufthansa do not support UPI directly on their booking websites, because their payment gateways operate outside the NPCI UPI rails. However, there are three reliable workarounds that let you effectively use UPI to book these airlines while still pricing the fare in Indian rupees.

The cleanest workaround is to book through a major Indian OTA — MakeMyTrip, EaseMyTrip, Cleartrip, or Paytm Travel. All four list international flights from Emirates, Qatar Airways, Lufthansa, British Airways, and dozens of other foreign carriers, and all four accept UPI at checkout. Your payment is processed in INR by the OTA, which then issues the ticket under its IATA accreditation. This also means you benefit from any active UPI platform discount — for example, Yatra was running up to ₹1,500 OFF with code YTUPI for UPI bookings in June 2026.

The second workaround is a UPI-linked RuPay credit card. RuPay credit cards issued by HDFC Bank, SBI, ICICI Bank, and others can now be linked to PhonePe or Google Pay's UPI system. When you pay via UPI on the foreign airline's India site using a RuPay credit card, the charge appears as a UPI transaction in your app but is processed as a card transaction by the airline — bridging both systems.

When you book Emirates.com/in or Qatarairways.com/in using a credit or debit card, the payment page may ask: "Do you want to pay in INR ₹85,342 today?" This is Dynamic Currency Conversion (DCC). Your card issuer is bypassed — instead, the airline's payment gateway applies their own INR conversion rate, which is typically 4–8% above the mid-market rate. On an ₹85,000 international ticket, that DCC markup costs you ₹3,400–₹6,800 extra. Always pay in the local currency of the destination country (EUR, GBP, AED) using a zero-forex card — or better yet, book via an Indian OTA with UPI to avoid DCC entirely.

3. UPI transaction limits for flight payments in 2026

As of 15 September 2025, NPCI raised the UPI Person-to-Merchant (P2M) per-transaction limit to ₹5 lakh for verified merchant categories including travel, insurance, capital markets, government payments (GeM), and collections. The daily aggregate for these verified categories was simultaneously raised to ₹10 lakh. This change was enacted following an RBI directive asking NPCI to explore higher UPI limits to enable high-value digital payments without forcing users to split transactions.

Before this change, UPI P2M transactions — including flight bookings — were capped at ₹1 lakh per transaction, which created a genuine problem for business-class or long-haul international bookings that routinely exceed ₹1 lakh for a single passenger. The new ₹5 lakh ceiling covers the vast majority of international bookings, including premium economy and business class fares on routes like Delhi–London, Mumbai–New York, and Bengaluru–Melbourne.

| UPI payment type | Per-transaction limit | Daily aggregate limit | Effective date |

|---|---|---|---|

| P2P (person-to-person) | ₹1 lakh | ₹1 lakh | Unchanged |

| P2M — standard merchants | ₹1 lakh | ₹1 lakh | Unchanged |

| P2M — verified travel / insurance / capital markets | ₹5 lakh | ₹10 lakh | 15 September 2025 |

There is an important caveat: the higher ₹5 lakh limit applies only to merchants who have been verified under the relevant category by their acquiring bank and NPCI. Major airlines (Air India, IndiGo) and the large OTAs (MakeMyTrip, EaseMyTrip, Cleartrip, Paytm) are all registered verified travel merchants and benefit from the higher limit. However, small independent booking agencies or newly registered OTAs may still operate under the standard ₹1 lakh P2M cap. If a booking fails for a large amount, check whether the merchant is verified — if not, split the booking (individual tickets per passenger) or switch to net banking or a credit card.

NPCI sets the network ceiling, but individual banks can set their own lower limits on UPI transactions. HDFC Bank, ICICI Bank, and Axis Bank allow up to ₹1 lakh per transaction for most UPI-linked savings accounts by default, with select accounts or premium customers permitted up to ₹2 lakh. Even after NPCI raised the P2M ceiling to ₹5 lakh, your bank may still cap you at ₹1 lakh unless you upgrade your account type or call the bank to increase your UPI limit. Check your bank's UPI app settings or contact customer care to confirm your personal limit before attempting a high-value international booking.

On-the-Ground Insight: "I tried booking a Mumbai–Dublin economy fare of ₹1,12,000 via Air India's app using UPI — the payment failed immediately because my Axis Bank savings account still had the old ₹1 lakh UPI cap. A two-minute call to Axis Bank's UPI helpline increased my limit to ₹2 lakh within 24 hours. Lesson: call your bank before the fare expires." — Rohan T., Dublin City University, MSc Computing, 2026 Intake

4. NRI UPI: how to link your NRE/NRO account and book flights from abroad

NRIs from more than 10 countries — including the UK, USA, UAE, Singapore, Australia, Canada, Oman, Qatar, Malaysia, and Saudi Arabia — can activate UPI using their international mobile number linked to an NRE or NRO account held with an Indian bank, without needing an active Indian SIM card. This was enabled by a January 2023 NPCI circular allowing non-resident accounts to be onboarded onto the UPI system with international phone numbers — and has become the most popular way for Indian students and professionals abroad to pay for flights home in rupees.

The setup requires three things: an active NRE (Non-Resident External) or NRO (Non-Resident Ordinary) account with an Indian bank that has UPI enabled; an international mobile number registered with that bank account; and a UPI app (PhonePe, Google Pay, Paytm, or BHIM) installed on a smartphone.

- Download PhonePe on your smartphone in your country of residence.

- Open the app and tap "Register." Enter your international mobile number with the correct country code (e.g. +353 for Ireland, +44 for UK).

- PhonePe sends an SMS OTP to your international number. Enter it to verify.

- The app auto-detects your NRE/NRO account linked to that number and shows you a list of eligible bank accounts.

- Select your NRE or NRO account and set your UPI PIN (6-digit, using your debit card details).

- Your UPI ID is created (e.g. yourname@ybl). You can now send money to, and receive money from, any UPI ID in India — and pay on any merchant UPI QR code.

Once set up, an NRI in Dublin can open MakeMyTrip, EaseMyTrip, or Air India's website, search for a Mumbai–Dublin flight, and pay via UPI at checkout — the debit hits their Indian NRE account. No forex conversion, no bank card needed, no OTP failure due to international card restrictions. This completely bypasses the most common pain points NRIs face with international card payments: the RBI e-mandate requirement for international transactions, 3D Secure OTP failures when the OTP is sent to an Indian SIM they no longer carry, and the 2–3.5% forex markup on non-zero-forex cards.

One important limitation: NRI UPI is for payments from an Indian rupee account to Indian merchants. You cannot use your NRI UPI to pay at foreign merchants (e.g., Emirates.com.ae) — the merchant must be an Indian UPI-registered entity. For overseas bookings on foreign airline websites, you still need to use an international card or book via an Indian OTA.

5. Where can you use UPI abroad in 2026?

As of June 2026, UPI is accepted for merchant payments in more than 8 countries: UAE, Singapore, Bhutan, Nepal, Sri Lanka, France, Mauritius, and Qatar, with Thailand having moved from pilot to wider acceptance in May 2026 via the UPI-PromptPay linkage. The international rollout is managed by NPCI International (NIPL), the global arm of NPCI, through bilateral agreements with partner payment networks and central banks.

For Indian travelers, this means you can tap-and-pay at merchants using your Indian UPI app in these countries — no currency exchange, no forex card, no international card DCC markup. The payment is debited from your Indian bank account in rupees and converted at the interbank rate at the moment of transaction, typically the best available rate.

| Country | UPI status (June 2026) | Partner network | Notable acceptance points |

|---|---|---|---|

| UAE | ✅ Live — 60,000+ merchants | NEOPAY / Mashreq | Malls, supermarkets, restaurants, taxis |

| Singapore | ✅ Live — 12,000+ merchants via PayNow | PayNow / HitPay | Hawker centres, Mustafa Centre, Changi Airport shops |

| France | ✅ Live — Lyra network | Lyra | Eiffel Tower, tourist attractions, select shops |

| Qatar | ✅ Live — Qatar Duty Free & select merchants | QNB | Hamad International Airport Qatar Duty Free, LuLu Hypermarket |

| Nepal | ✅ Live — 200,000+ POS terminals | NIPL / NPS (Nepal) | Supermarkets, pharmacies, hotels |

| Sri Lanka | ✅ Live | NIPL / LankaPay | Selected retail, hospitality |

| Bhutan | ✅ Live — first foreign country | Royal Monetary Authority | Nationwide UPI QR acceptance |

| Mauritius | ✅ Live | NIPL / MCB | Hotels, tourist zones |

| Thailand | ✅ Wider rollout May 2026 | UPI-PromptPay linkage | Bangkok malls, airports, tourist areas |

Countries with signed MoUs or in active expansion as of June 2026 include Oman, Japan, Greece, Cyprus, Saudi Arabia, Australia, and Canada. Travelers on India–Ireland routes should note that Ireland is not currently in the UPI acceptance network — UPI payments do not work at Irish merchants. For expenses in Ireland, you will need a zero-forex international card or a Wise/Revolut account.

One practical tip for travelers stopping over in Dubai (DXB) or Doha (DOH): both the UAE and Qatar have live UPI networks, so you can pay for airport lounges (if the lounge operator has UPI QR), duty-free shopping, and airport restaurants using your Indian UPI app — eliminating the need to carry AED or QAR cash for a transit stop.

6. UPI vs credit card: true cost comparison for international flight bookings

For international flight bookings made through Indian OTAs, UPI is usually 2–5% cheaper than paying by credit card once you account for convenience fees and forex markup, assuming a fare above ₹30,000. The True Cost Formula below shows exactly where the savings come from.

True Cost = Base Fare + Convenience Fee + Forex Markup Fee + GST on Markup

Let's apply this to a realistic booking scenario: a Mumbai–Dublin Economy Class fare of ₹72,000 booked via MakeMyTrip.

| Cost component | UPI payment | Standard credit card (3.5% forex markup) | Zero-forex credit card (0% markup) |

|---|---|---|---|

| Base fare | ₹72,000 | ₹72,000 | ₹72,000 |

| Convenience fee | ₹0–₹150 | ₹250–₹350 | ₹250–₹350 |

| Forex markup | ₹0 | ₹2,520 (3.5%) | ₹0 |

| GST on forex markup (18%) | ₹0 | ₹454 | ₹0 |

| Total true cost | ₹72,150 | ₹75,324 | ₹72,350 |

| Reward points earned | None (no credit card) | 720–2,160 pts (~₹720–₹2,160 value) | 720–2,160 pts (~₹720–₹2,160 value) |

| Net cost after rewards | ₹72,150 | ₹73,164–₹74,604 | ₹70,190–₹71,630 |

The analysis shows UPI is significantly cheaper than a standard credit card (saving ₹1,014–₹2,454 on a ₹72,000 fare). However, a zero-forex credit card with strong reward points (e.g., HDFC Infinia at 3.3% effective reward rate or Axis Magnus) can actually beat UPI once rewards are factored in — saving you ₹480–₹1,960 more than UPI over the same ₹72,000 booking. The right choice depends on whether you hold a premium rewards card. If you don't, UPI is your cheapest option by a significant margin.

One additional dimension: OTA-level UPI cashback. Yatra offered ₹1,500 off with code YTUPI in June 2026. Air India offered ₹2,000 off with UPIPROMO. These promotions are not available on credit card payments, making UPI the absolute cheapest option when a promo code is active.

Some OTAs display international fares in USD or EUR with a "pay in USD" option. If you choose this option and pay via UPI, your bank will convert at the bank's TT (telegraphic transfer) selling rate — which is typically 1–2% above the mid-market rate. This is not the same as zero forex markup. Always ensure the OTA is charging you in INR before proceeding with UPI payment.

7. Step-by-step: how to set up and use UPI for travel before and during your trip

Setting up UPI for seamless international travel — both for booking flights and paying abroad — takes about 20 minutes before your trip and requires confirming your UPI limit with your bank, enabling international transaction permissions, and installing a secondary UPI app as backup.

Before booking: check your UPI limit and account type

Call your bank or check your UPI app settings to confirm your current per-transaction UPI limit before booking a high-value international ticket. Many Indian savings accounts default to ₹1 lakh per transaction even though NPCI raised the ceiling for travel merchants to ₹5 lakh in September 2025. To increase your limit, log in to your bank's mobile banking app, navigate to "UPI settings" or "Transfer limits," and request an increase — or call customer care. HDFC, ICICI, and Axis typically process limit increases instantly via their apps or within 24 hours by phone.

Enable international usage on your linked account

If you are booking an international airline through an Indian OTA, your savings account used for UPI must have international merchant payments enabled — this is a separate toggle from your UPI limit. Since the RBI's 2020 directive, international online transactions (including on Indian platforms that use international payment processors) are disabled by default on most Indian debit cards and accounts. Log in to your bank app, go to "Card settings" or "Manage card," and enable "International merchant transactions (online)" before attempting a large OTA booking. This step is distinct from — but complementary to — checking your UPI per-transaction limit.

- HDFC Bank: MobileBanking app → Cards → Manage Card → International Transactions → Enable Online International

- ICICI Bank: iMobile → Cards → Card Settings → Online International Transactions → Enable

- SBI: YONO app → My Cards → Card Controls → Enable International Use

- Axis Bank: Axis Mobile → Cards → Enable/Disable Features → International Transactions

During booking: selecting UPI at checkout

When you reach the payment page on MakeMyTrip, EaseMyTrip, Air India's website, or any other UPI-enabled platform, select "UPI" from the payment method dropdown, then choose between entering your UPI ID (VPA) or scanning a QR code. On desktop, most platforms show a QR code you can scan with your phone's camera using any UPI app. On mobile, the platform deep-links directly to your installed UPI apps (PhonePe, Google Pay, Paytm, BHIM) and you choose which one to authenticate with. Complete the payment by entering your 6-digit UPI PIN. You have 60 seconds before the QR or intent link expires — have your phone and PIN ready before initiating.

While abroad: using UPI at international merchant locations

In UPI-accepting countries (UAE, Singapore, Qatar, Nepal, France, Thailand as of June 2026), look for the BHIM UPI QR sticker at merchant counters — it looks identical to Indian UPI QR codes. Open your PhonePe, Google Pay, or Paytm app, tap "Scan QR," scan the merchant's code, enter the amount in the local currency, and confirm with your PIN. The exchange rate applied is the real-time interbank rate — no DCC, no forex markup from a card issuer. At Dubai Airport's duty-free (DXB), for example, you can pay in AED via UPI and your Indian bank debits the rupee equivalent at the live rate.

NRI travelers: booking India flights from Ireland or the UK

NRIs based in Ireland, the UK, or other eligible countries can use their NRI UPI (linked to NRE/NRO account) to book India-origin flights on Indian OTAs without any forex markup or international card OTP issues. The entire payment flow happens in INR, from an Indian bank account, using a UPI ID linked to an international mobile number. This is particularly useful for booking India-to-Dublin or India-to-London return legs that are priced in INR on Air India, MakeMyTrip, or EaseMyTrip — you pay the rupee price directly from your Indian account with no conversion loss.

Compare live fares before you book

UPI works best when you lock in the right fare first. Compare live prices across Indian and international carriers on MyFlightOffers before heading to checkout.

All information in this guide is based on publicly available official sources including NPCI circulars, airline payment pages, and OTA offer pages as of June 2026. UPI limits, airline payment acceptance, NRI eligibility countries, and international UPI acceptance territories can change without notice. Always verify current information directly with NPCI, your bank, and the relevant airline or OTA before booking. MyFlightOffers is not affiliated with any organisation mentioned. This article does not constitute financial or payment advice.

- Card Tokenization for Flight Bookings India 2026 — How RBI's tokenization mandate affects saved card payments on OTAs and airline apps

- TCS on International Travel Spend 2026 — When TCS applies to flight bookings, how much is deducted, and how to claim it back in your ITR

- HDFC Credit Card Flight Offers 2026 — Current HDFC bank card discounts on MakeMyTrip, EaseMyTrip, and Cleartrip

- Indian Card Declined on Foreign Airline Website? Here's How to Fix It (2026) — Step-by-step guide to enabling international usage and bypassing 3D Secure failures