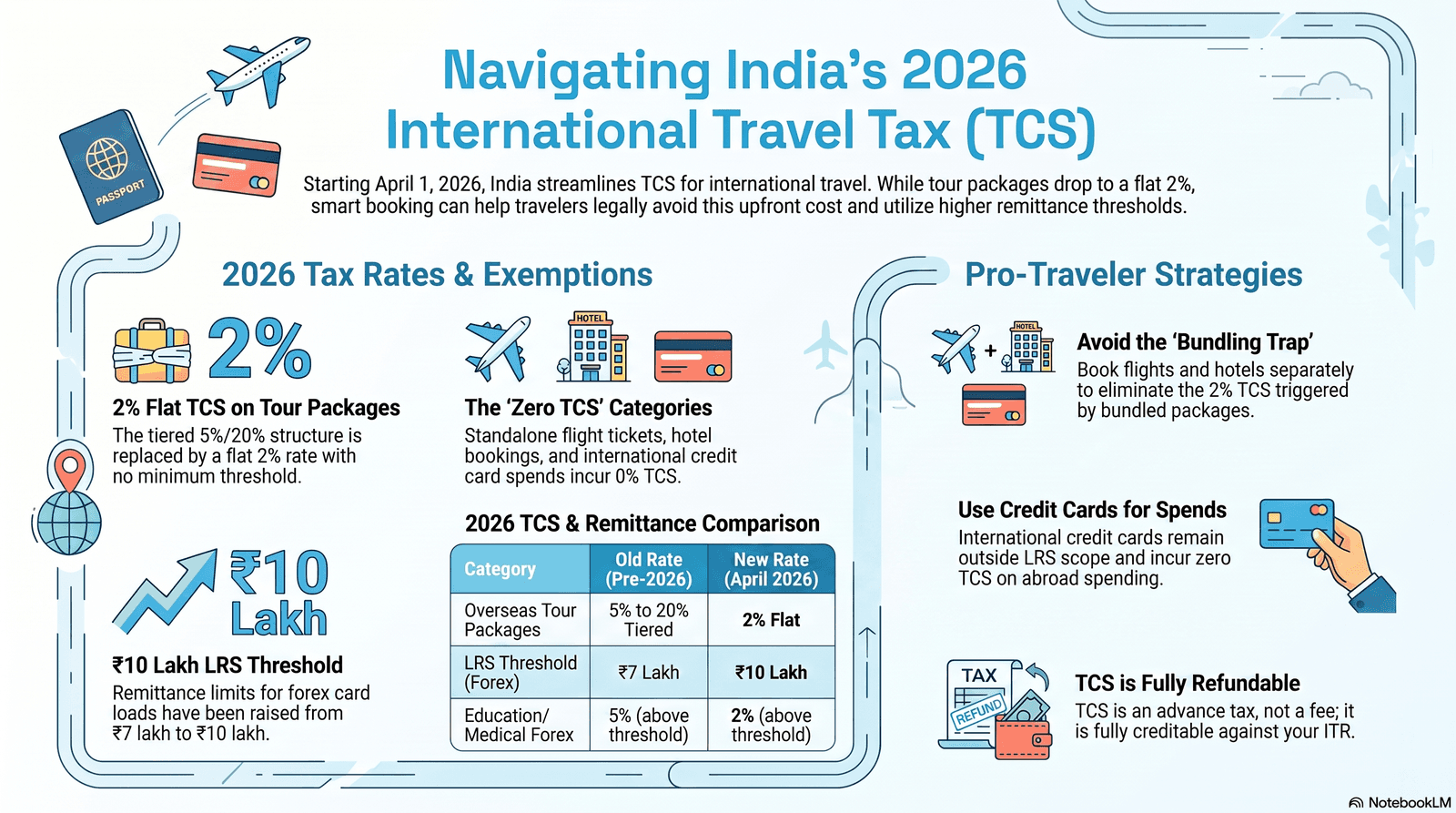

- Budget 2026 slashed TCS to 2% flat: From 1 April 2026, overseas tour packages attract a uniform 2% TCS — down from 5% (up to ₹7 lakh) and 20% (above ₹7 lakh). The ₹10 lakh LRS threshold for other remittances remains unchanged.

- Solo flight tickets do NOT trigger TCS: Buying only an international flight ticket or only a hotel room does not qualify as an "overseas tour package." TCS applies only when two or more elements (travel + accommodation + other services) are bundled together.

- Credit card spends abroad are currently exempt: International credit card transactions made while physically overseas are not classified under LRS and are therefore not subject to TCS as of June 2026. Forex card loads above ₹10 lakh attract 20% TCS for non-education/non-medical remittances.

2% flat — no threshold

₹10 lakh per financial year

Zero — not an overseas tour package

Zero — outside LRS as of June 2026

- What is TCS and when does it apply to travel?

- Which travel transactions trigger TCS?

- Budget 2026 TCS rate changes — full breakdown

- How to claim your TCS refund via ITR

- Impact on NRIs using Indian cards from abroad

- Cards and platforms that auto-deduct TCS

- Practical checklist before booking your international trip

1. What Is TCS and When Does It Apply to International Travel?

Tax Collected at Source (TCS) is an advance tax that an authorized collector — typically your bank, tour operator, or OTA — deducts from your payment at the time of a qualifying transaction and remits to the Income Tax Department on your behalf. It is not an extra cost: TCS is fully creditable against your total income tax liability and refundable if your tax liability is lower than the TCS already paid.

TCS on international travel falls under Section 206C(1G) of the Income Tax Act, 1961, inserted via the Finance Act 2020. This section specifically covers two categories of outbound transactions from India:

- Outward remittances under the Liberalised Remittance Scheme (LRS) — wire transfers, forex card loads, bank drafts, and similar instruments used to move money from India to foreign accounts or foreign currency.

- Overseas tour packages — any bundled package that includes at least two of: international travel, accommodation, meals, or related travel services. The seller (tour operator, OTA, or bank) must collect TCS at the time of payment.

Under the Income Tax Act, an overseas tour package is defined as any arrangement that includes travel to any country outside India combined with at least one of: hotel accommodation, boarding or lodging, meals, or other travel-related expenditure. Purchasing only an international flight ticket or only a hotel room does NOT constitute an overseas tour package. The combination requirement is what triggers TCS.

The important distinction — missed by many travelers — is that TCS is about the nature of the transaction, not simply whether you are spending money on travel. The Reserve Bank of India's Liberalised Remittance Scheme permits Indian residents to remit up to USD 250,000 (approximately ₹2.1 crore) per financial year for any permissible current or capital account transaction. TCS is the Income Tax Department's mechanism to track and ensure these outflows are reported in your tax return.

2. Which Travel Transactions Trigger TCS — and Which Do Not?

Whether a travel spend triggers TCS depends entirely on the transaction type: bundled tour packages always do, standalone flight or hotel purchases never do, and the treatment of forex card loads versus credit cards differs significantly.

| Transaction type | TCS applicable? (2026) | Rate | Threshold | Who collects |

|---|---|---|---|---|

| Overseas tour package (flight + hotel bundled) | ✅ Yes | 2% (from 1 Apr 2026) | No minimum — applies from ₹1 | Tour operator / OTA / bank |

| Standalone international flight ticket | ❌ No | — | — | N/A |

| Standalone international hotel booking | ❌ No | — | — | N/A |

| Forex card load (education/medical purpose) | ✅ Yes — above ₹10 lakh | 2% above ₹10 lakh | ₹10 lakh aggregate per FY | Authorised dealer (bank) |

| Forex card load (other/travel purpose) | ✅ Yes — above ₹10 lakh | 20% above ₹10 lakh | ₹10 lakh aggregate per FY | Authorised dealer (bank) |

| International credit card spends abroad | ❌ No (as of June 2026) | — | — | N/A (pending RBI review) |

| Bank wire transfer abroad (LRS) for travel | ✅ Yes — above ₹10 lakh | 2% above ₹10 lakh (medical/travel) or 20% (other) | ₹10 lakh aggregate per FY | Remitting bank |

| Education loan remittance | ❌ No | 0% | — | N/A |

If you book a flight and hotel together as a package through MakeMyTrip, Yatra.com, or EaseMyTrip, the platform classifies it as an overseas tour package and collects 2% TCS. The same flights and hotel booked separately — in two transactions — do NOT trigger TCS. This is a structural loophole that is entirely legal: book your flights on the airline's website and your hotel on Booking.com or directly, and you pay zero TCS on both.

3. Budget 2026 TCS Rate Changes — Full Breakdown

The Union Budget 2026 (presented 1 February 2026, effective 1 April 2026) made the most significant TCS simplification since Section 206C(1G) was introduced in 2020 — collapsing the complex tiered rate structure into a simpler framework.

The previous structure had multiple rates and thresholds that created confusion and compliance friction. The key changes under the Finance Act 2026 are:

| Transaction category | Rate before 1 Apr 2026 | Rate from 1 Apr 2026 | LRS threshold |

|---|---|---|---|

| Overseas tour packages | 5% (up to ₹7L) / 20% (above ₹7L) | 2% flat — no threshold | No threshold — applies from ₹1 |

| LRS for education (own funds) | 5% above ₹7 lakh | 2% above ₹10 lakh | ₹10 lakh (raised from ₹7L in Budget 2025) |

| LRS for medical treatment | 5% above ₹7 lakh | 2% above ₹10 lakh | ₹10 lakh |

| LRS for other remittances (investments, gifts, travel via wire) | 20% above ₹7 lakh | 20% above ₹10 lakh | ₹10 lakh (threshold raised) |

| Education loan remittance | 0% | 0% | — |

| International credit card spends abroad | Exempt (not under LRS) | Exempt (status unchanged) | N/A |

Source: Income Tax Department, India — Finance Act 2026 provisions, effective 1 April 2026; ClearTax TDS/TCS Changes April 2026.

True Package Cost = Quoted Price + 2% TCS (collected upfront) + Forex Markup (if paid in INR via Indian card)

Example: A ₹1,50,000 bundled India–Europe package booked via MakeMyTrip attracts ₹3,000 TCS (2%). If paid using an HDFC Regalia card (3.5% forex markup via international gateway), add another ₹5,250. Your true out-of-pocket cost is ₹1,58,250 — before the TCS refund at tax time. Booking the same flights and hotel separately eliminates the ₹3,000 TCS entirely.

🧮 TCS on Outbound Travel Spend Calculator (2026)

Estimate the upfront Tax Collected at Source (TCS) on your overseas bookings, forex card loads, and wire transfers based on the new 1 April 2026 Budget rates.

Calculation Breakdown

4. How to Claim Your TCS Refund When Filing Your Income Tax Return

TCS is not a permanent cost — it is an advance tax that is automatically credited to your PAN and fully refundable if your total tax liability is lower than the TCS paid during the financial year.

The refund process works through India's standard ITR filing system. Here is the step-by-step process for FY 2025-26 filers (filing due July 2026):

Step 1 — Verify TCS appears in your tax credit statement

Log in to the Income Tax e-filing portal and confirm that all TCS deductions are correctly reflected in your Form 26AS (for FY 2025-26) or Form 168 (for FY 2026-27 onwards). Navigate to e-File → Income Tax Returns → View Form 26AS. Each TCS entry shows the collector (your bank or tour operator), the amount collected, and the date.

If TCS deducted by your bank or OTA does not appear in Form 26AS, the Income Tax Department will not credit it against your tax liability automatically. This happens when the collector fails to file their TCS return on time. Contact the collecting entity (your bank or OTA) and ask them to file a correction. Do not submit your ITR claiming TCS that does not appear in Form 26AS — it will be rejected during processing.

Step 2 — Select the correct ITR form

Most salaried individuals with TCS on travel use ITR-1 (Sahaj) or ITR-2, depending on their income sources. Choose ITR-2 if you have capital gains, foreign income, or income from more than one house property. The TCS credit from Form 26AS is automatically pre-filled in the tax credit schedule of the ITR.

Step 3 — TCS is offset against your total tax liability

The TCS amount appears as a pre-paid tax credit, identical in treatment to TDS deducted from your salary. If your total income tax liability (after all deductions under Chapter VI-A) is, say, ₹80,000 and you have ₹6,000 in TCS already deducted on a holiday package, your net tax payable is ₹74,000. If the TCS paid exceeds your liability, the difference becomes a refund paid to your bank account within 3–4 weeks of ITR processing.

Step 4 — FY 2026-27 change: Form 26AS replaced by Form 168

From FY 2026-27 (ITR filing due July 2027), the Income Tax Department has introduced Form 168, which replaces Form 26AS as the comprehensive tax credit statement. For the current filing season (FY 2025-26, filing due July 2026), Form 26AS still applies. The process for claiming TCS credit remains identical regardless of which form is used.

On-the-Ground Insight: "I booked a Dubai package through Yatra.com in February 2025 for ₹2.2 lakh. They collected ₹11,000 as TCS (at the old 5% rate). When I filed my ITR-1 in July 2025, the ₹11,000 appeared automatically as a pre-paid tax. My total liability was ₹48,000 but I only had to pay ₹37,000 cash after adjusting the TCS. The refund for the rest came within six weeks. At the new 2% rate from April 2026, it would only have been ₹4,400 TCS — much less to wait to recover." — Nikhil R., IT Consultant, Bengaluru, FY 2025-26 filer

5. Impact on NRIs Using Indian Cards from Abroad

Non-Resident Indians (NRIs) are completely outside the scope of LRS and are therefore not subject to TCS on remittances or spending — the scheme applies only to Indian residents.

This is a critical clarification for the large community of Indian students, workers, and professionals based in Ireland, the UK, and other countries who continue to hold Indian bank accounts and cards. The specific position as of 2026:

- NRE accounts: Funds in an NRE (Non-Resident External) account are already foreign earnings repatriated to India — there is no LRS remittance involved and therefore no TCS applicable on any use of NRE-linked cards.

- NRO accounts: NRO (Non-Resident Ordinary) accounts hold India-sourced income. Repatriation of funds from an NRO account abroad has its own FEMA rules but is not subject to TCS under Section 206C(1G).

- Indian credit cards used abroad by NRIs: Not subject to TCS — the LRS exemption for credit cards abroad applies to all cardholders, and NRIs are additionally outside LRS scope entirely.

- Resident Indians temporarily abroad (students on student visas): A student who recently left India and has not yet established NRI status (less than 182 days outside India in the financial year) technically remains a "resident" for tax purposes. For them, the LRS and TCS rules still apply to remittances made while physically in India.

You are an NRI for tax purposes if you spent fewer than 182 days in India during the financial year (1 April – 31 March). First-year students who left India in August and spent the rest of the year in Ireland will be resident for Indian tax in the year they left (depending on which half they spent in India). From the following financial year, if they remain abroad, they become NRIs and exit the LRS/TCS framework entirely.

6. Cards and Platforms That Auto-Deduct TCS

TCS is collected at source by the authorised dealer or seller — your bank collects it on forex card loads and wire transfers, while OTAs collect it on bundled overseas tour packages. Understanding who collects TCS and when helps you plan around it.

Which OTAs trigger TCS on package bookings?

All major Indian OTAs — MakeMyTrip, Yatra, EaseMyTrip, Cleartrip, and ixigo — are required to collect 2% TCS when you book an overseas tour package through their platforms, even if payment is made in Indian Rupees. The TCS is displayed at checkout and forms part of the total amount charged to your card or deducted from your wallet.

| Platform / Card | TCS collected? | When? | Rate (from Apr 2026) | Notes |

|---|---|---|---|---|

| MakeMyTrip | ✅ Yes — on bundled packages | At checkout | 2% | Flight-only or hotel-only: No TCS |

| Yatra.com | ✅ Yes — on bundled packages | At checkout | 2% | Flight-only: No TCS |

| EaseMyTrip | ✅ Yes — on bundled packages | At checkout | 2% | Separate bookings exempt |

| Direct airline booking (Air India, Emirates, etc.) | ❌ No | — | — | Standalone flights, no TCS |

| Forex card load (HDFC, ICICI, SBI) | ✅ Yes — above ₹10 lakh | At load time | 20% (non-education) | Collected by authorised dealer bank |

| Niyo Global Card (SBM Bank) | ✅ Yes — above ₹10 lakh load | At card load time | 20% (non-education) | Zero forex markup on spends; TCS on loads above threshold |

| International credit card (HDFC Regalia, ICICI Sapphiro, Axis Magnus) | ❌ No — abroad spends exempt | — | — | Credit card spends abroad not under LRS as of June 2026 |

Are there PAN requirements to avoid higher TCS?

Yes — Section 206CC of the Income Tax Act mandates that if you do not provide your PAN (or Aadhaar) to the TCS collector, TCS is levied at double the standard rate or 5% (whichever is higher). For overseas tour packages, that means 4% instead of 2% if your PAN is missing. Always provide your PAN when booking international packages, loading forex cards, or initiating wire transfers.

7. Practical Checklist Before Booking Your International Trip

Following this checklist before booking eliminates TCS surprises and ensures you can reclaim any TCS paid as efficiently as possible.

- Book flights and hotels separately to avoid the overseas tour package definition and eliminate TCS entirely. Use the airline's website for flights and Booking.com or the hotel directly for accommodation.

- If using an OTA package, factor in the 2% TCS at checkout — it will appear as a separate line item and is recoverable via ITR.

- Check your LRS utilisation for the financial year at your bank before loading a forex card. If your aggregate LRS for the year is below ₹10 lakh, no TCS applies to forex card loads.

- Use a credit card (not a forex card) for large travel payments abroad to sidestep the 20% TCS on non-education forex loads above ₹10 lakh.

- Provide your PAN to every TCS collector — OTA, bank, tour operator — to avoid the 4% double-rate penalty.

- Download Form 26AS (or Form 168 from FY 2026-27) from the Income Tax portal after travel and confirm all TCS entries are correctly recorded under your PAN before filing your ITR.

- NRIs (183+ days outside India): TCS does not apply to you — but confirm your residency status for the relevant financial year before the OTA deducts TCS; some platforms may still ask for a self-declaration of NRI status.

- Check your card's forex markup: even if TCS is zero (credit card abroad), a 3.5% forex markup on a ₹3,00,000 trip costs ₹10,500 extra. Use a zero-forex card or settle in the local currency. The Niyo Global Card (0% markup; TCS applies on loads above ₹10 lakh), Fi Money US account debit, and the IDFC FIRST WoW credit card (1% markup) are the most competitive options in mid-2026. Con: Niyo's 20% TCS on loads above ₹10 lakh is a significant drawback for high-volume travelers.

What if you receive a tax notice about TCS?

If the Income Tax Department issues a notice about a mismatch between LRS remittances reported by your bank and your ITR, the most common fix is to verify that your ITR includes the correct TCS credit from Form 26AS and re-file or respond with documentary evidence of the TCS already paid. Notices about TCS mismatches (under Section 133(6)) require a response within 30 days. Keep all OTA receipts, forex card load confirmations, and bank statements for at least 6 years. The TaxBuddy and ClearTax platforms both provide TCS notice handling guidance.

Ready to book? Compare live fares and minimise your travel costs.

Use our fare calendar to find the cheapest windows for India–Europe routes — then book flights separately to avoid TCS on bundled packages.

All information in this article is based on publicly available official sources as of June 2026, including the Income Tax Department of India, the Reserve Bank of India, the Finance Act 2026, and ClearTax / Wise India guidance. TCS rates, LRS thresholds, and credit card treatment rules are subject to change. Always verify current provisions directly with the Income Tax Department or a qualified chartered accountant before acting on this information. MyFlightOffers is not affiliated with any bank, OTA, or tax authority. This article does not constitute tax or financial advice.

- NEW TCS on International Travel Spend 2026 — this article

- HDFC Credit Card Flight Offers 2026 — which HDFC cards give the best rewards on international bookings and how to avoid forex markup

- Card Tokenization for Flight Booking India 2026 — how RBI's card tokenization mandate affects OTP, international transactions, and stored cards on OTAs

- Transfer Credit Card Points to Airline Miles India 2026 — convert HDFC, Axis, ICICI reward points to Air India, Vistara, or international miles

- Dublin to Delhi — Best Indian Bank Card Offers 2026 — card offers, OTA discounts, and TCS-smart booking strategy for the DUB–DEL route