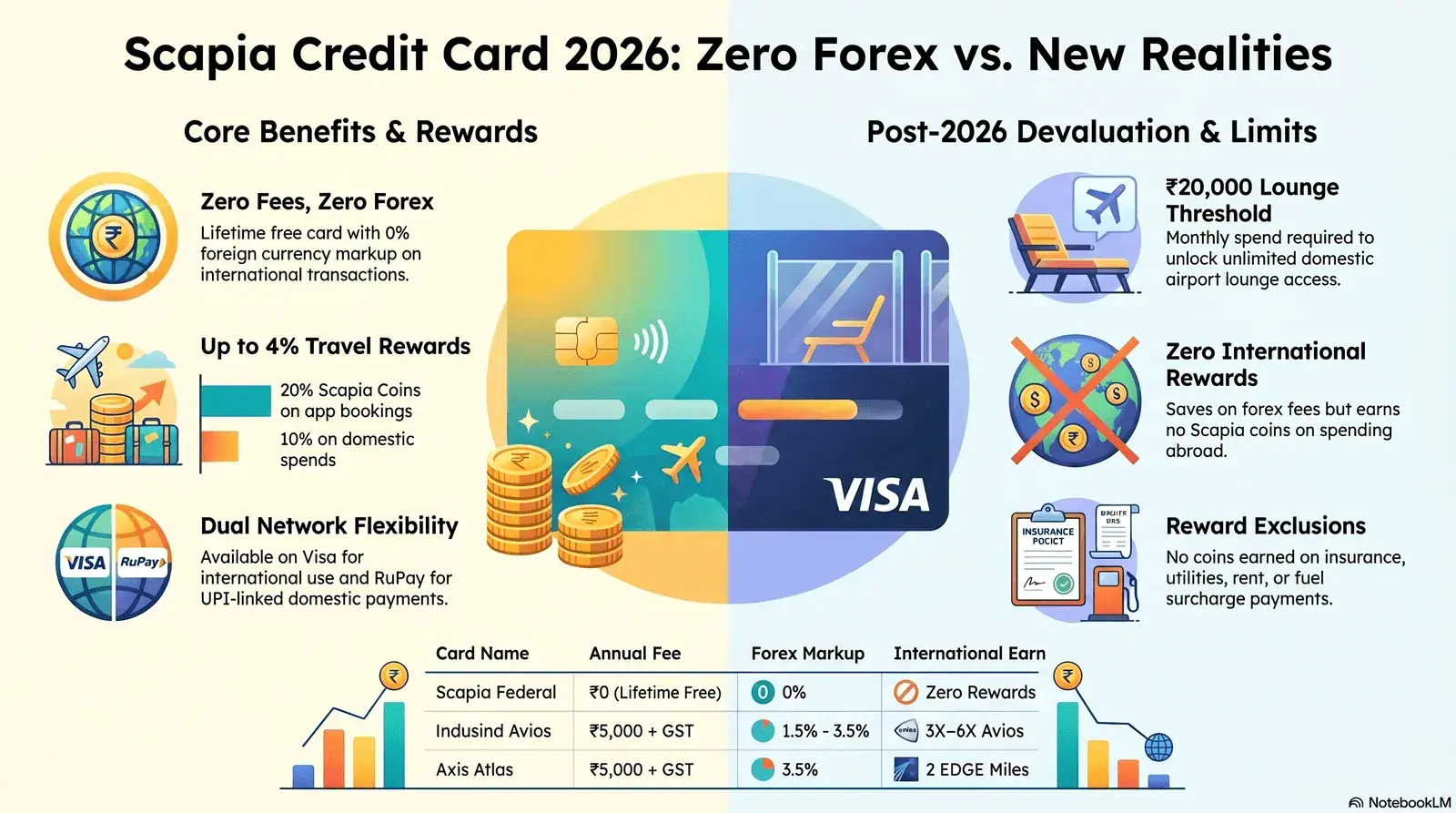

- Zero cost, zero markup: Scapia is lifetime free with no forex fee on international transactions — but earns zero Scapia Coins on those same international spends.

- The February 2026 devaluation matters: The monthly spend threshold for domestic lounge access doubled to ₹20,000, and rewards on insurance and utilities were removed. Light spenders may no longer qualify.

- Best role for NRIs: Use Scapia for domestic Indian flight bookings (20% coins via app) and a Wise card abroad. Do not expect Scapia to replace a premium miles card if you fly internationally more than twice a year.

₹0 — Lifetime free

0% — No conversion surcharge

20% Scapia Coins = 4% travel cashback

10% Scapia Coins = 2% travel cashback

0 coins — Nil rewards abroad

Unlimited — requires ₹20,000 spend previous month

- What makes Scapia different: zero forex + lifetime free

- Earn structure: 10% rewards + 20% on Scapia travel bookings

- Key limitation: zero earn on international spends

- Lounge access: domestic only and the ₹20,000 spend threshold

- The February 2026 devaluation: what changed

- Best use case for NRIs: domestic India vs Wise card abroad

- Verdict: Scapia vs IndusInd Avios vs Axis Atlas

- Eligibility and how to apply

What makes Scapia different: zero forex + lifetime free

The Federal Bank Scapia credit card is one of the only travel credit cards in India that combines a permanent ₹0 annual fee with a 0% forex markup fee — making it structurally different from every other premium travel card in the market. Most travel cards either charge an annual fee of ₹1,000–₹10,000 or apply a foreign currency markup of 1.5%–3.5% on international transactions. Scapia removes both costs entirely.

The card is issued by Federal Bank in partnership with the fintech platform Scapia and is available on both Visa and RuPay networks. That dual-network design is deliberate: the Visa card handles international transactions (contactless, chip-and-pin, and online purchases on foreign websites), while the RuPay card enables UPI-linked spending in India. Both operate under a single credit account and a single monthly statement.

For a frequent domestic traveller who books flights through the Scapia app, the savings are real and compounding. If you were previously using a card with a 3% forex markup and paying a ₹5,000 annual fee, Scapia eliminates both costs while adding lounge access and a 4% effective travel cashback. The only thing you give up is the aspirational premium card experience — airport concierge, international lounge access, and the ability to transfer points to airline miles programmes.

Earn structure: 10% rewards + 20% on Scapia travel bookings

Every ₹100 you spend on eligible domestic transactions earns 10 Scapia Coins; every ₹100 spent booking flights, hotels, trains, or buses through the Scapia app earns 20 Scapia Coins. Each coin is worth ₹0.20 when redeemed for travel bookings (5 coins = ₹1). This translates to an effective cashback of 2% on regular spending and 4% on Scapia app travel bookings — competitive with paid mid-tier travel cards that cost ₹2,500–₹5,000 per year.

The earn rate applies to every purchase of ₹20 or more — groceries, dining, retail, online shopping. There is no monthly or annual cap on coin accumulation, and coins never expire as long as the card account remains active. Redemption happens exclusively through the Scapia app and can cover up to 100% of a travel booking. You cannot convert coins to cash, statement credits, or gift vouchers — they are strictly a travel currency within the Scapia ecosystem.

- ₹10,000 spent on groceries and dining → 1,000 coins → ₹200 off next flight booking

- ₹10,000 booked on Scapia app (flights/hotels) → 2,000 coins → ₹400 off next travel booking

- Monthly spend of ₹30,000 (mix of shopping + travel via app) → ~3,500–4,000 coins → ₹700–₹800 redeemable per month

What earns coins: all standard retail, dining, online purchases, fuel (check current terms), and travel booked via the Scapia app. What does not earn coins since the February 2026 update: insurance premium payments, utility bills (electricity, gas, water, broadband, mobile recharge), and rent payments. International transactions earn no coins at all — covered in detail in the next section.

User experience — Scapia app booking: "I book all my IndiGo and Air India domestic tickets through the Scapia app now. The fare is exactly the same as what I see on the airline website. The 20% coins add up to roughly ₹300–₹500 per ticket on a ₹7,000–₹10,000 domestic booking. Over six months, my coins covered the full cost of a short domestic trip." — Priya M., Bengaluru-based traveller, February 2026

🧮 Scapia Zero-Forex & Travel Rewards Savings Calculator

Calculate your annual savings and travel reward cashbacks with the lifetime free Federal Bank Scapia Card based on your spending profile. Defaults are illustrative — ₹15,000 a month of domestic spend — not figures published by Federal Bank.

Comparison: Estimated Annual Value (INR)

Key limitation: zero earn on international spends

The single biggest structural limitation of the Scapia card is that all international transactions earn zero Scapia Coins — you save on forex fees but receive no rewards whatsoever for spending abroad. This is an intentional design choice. Scapia positions the card as a domestic travel optimiser: the benefit of using it internationally is purely cost-avoidance (no 3% markup), not reward accumulation.

For Indian professionals travelling frequently between India and Europe or the US, this gap matters significantly. If you spend €2,000 per month abroad — on accommodation, grocery runs, dining, transport — you earn nothing on that spend. A Wise debit card or a card like the IndusInd Avios Infinite (1.5% forex markup, but earns Avios on international spends) might generate more long-term value on international segments despite the slightly higher foreign currency cost.

The math is clear: on a ₹1,50,000 round-trip ticket from Dublin to Delhi booked on a foreign airline website, Scapia saves you approximately ₹4,500 in forex markup (3% avoided) compared to a standard Indian bank card — but earns ₹0 in coins. An IndusInd Avios card charges ₹2,250 in markup (1.5%) but earns Avios miles worth approximately ₹2,500–₹4,000 on that same transaction. Depending on redemption, the premium card can actually produce a better net outcome on high-value international bookings.

Lounge access: domestic only and the ₹20,000 spend threshold

Scapia cardholders get unlimited access to domestic airport lounges across 60+ airports in India — but only if they spend ₹20,000 or more in the previous calendar month across both their Visa and RuPay Scapia cards combined. Hit the threshold in May and you get unlimited lounge access throughout June. Miss it in June and lounge access is suspended for July.

The lounge programme goes beyond a simple waiting room. Scapia markets it as "Airport Privileges" — a broader network covering 72 airports where cardholders get access to dining outlets, retail shops, and spa services (up to ₹1,000 in rewards redeemable at these merchants), not just the 32 airports with dedicated lounges. This is genuinely useful if you fly regularly through smaller tier-2 airports that do not have traditional lounges.

There is no international lounge access on Scapia — not even through a Priority Pass or DreamFolks network. If you transit through Dubai, Doha, or London Heathrow, you will need to buy a day pass or carry a separate card with international lounge access. This is one area where the IndusInd Avios Infinite (2 international visits per quarter via Priority Pass) and Axis Atlas clearly outperform Scapia.

The February 2026 devaluation: what changed and what it means for you

On 27 February 2026, Scapia made its first major change since launch, effectively reducing the card's value for a significant portion of its user base — particularly light spenders and those who relied on insurance and utility payments to hit the lounge-access threshold.

| Feature | Before Feb 2026 | From 27 Feb 2026 | Impact |

|---|---|---|---|

| Lounge access spend threshold | ₹10,000/month | ₹20,000/month | High — threshold doubled |

| Rewards on insurance premiums | 10% Scapia Coins earned | 0 coins, excluded | High for those with large premium payments |

| Rewards on utility bills | 10% Scapia Coins earned | 0 coins, excluded | Moderate — loses routine earn |

| Utilities toward milestone | Counted toward ₹10,000 | Does not count toward ₹20,000 | High for utility-heavy bill payers |

| Zero forex markup | Yes | Yes — unchanged | None — retained |

| Lifetime free | Yes | Yes — unchanged | None — retained |

| 20% earn on Scapia app bookings | Yes | Yes — unchanged | None — retained |

The devaluation hurt casual spenders most. A cardholder spending ₹8,000–₹12,000 per month on groceries, dining, and utility bills previously crossed the ₹10,000 lounge threshold with ease. After February 2026, the same cardholder — with utilities excluded — may only have ₹6,000–₹9,000 in eligible spend, well short of ₹20,000. For this segment, the card's most attractive perk (unlimited lounges) is now effectively locked out.

For higher-volume spenders — those naturally spending ₹25,000–₹40,000 per month on travel, dining, retail, and online purchases — the devaluation changes little. The threshold is higher, but their discretionary spend crosses it without effort, and the zero forex and 20% travel earn remain intact.

Community reaction (TechnoFino forum, February 2026): "The lounge threshold doubling is a real hit. I was using Scapia as my primary card for utility payments specifically to keep the lounge access active. Now those don't even count. I need to either spend more on discretionary categories or accept that the lounge benefit is gone for me." — Forum member, TechnoFino Credit Card Community, 27 January 2026

Best use case for NRIs: domestic India bookings vs Wise card abroad

For Indian professionals based in Ireland, the Scapia card is genuinely useful — but only for the India side of their financial life, not the European side. The optimal stack for an Ireland-based NRI in 2026 looks like this: Scapia for all domestic Indian travel and spending when visiting home, and a Wise multi-currency card or your Irish bank debit card for all European spending.

When you fly Dublin to Delhi — whether on Aer Lingus to London and then Air India onwards, or direct on Etihad through Abu Dhabi — the Scapia card saves you the 3% forex fee on your international ticket if booked via a foreign platform. But it earns you nothing in coins. Once you land in India, everything flips: use the Scapia app to book your onward domestic connections (Mumbai to Chennai, Delhi to Hyderabad), earn 20% coins, access the lounge with your ₹20,000 threshold met from previous month's Indian spending, and pay for hotels and restaurants with the card to accumulate further coins.

- In Ireland (daily spending): Use your Irish bank debit card or Revolut — no need for Scapia here, and it earns nothing anyway.

- International flight booking (Dublin–Delhi): Use Scapia Visa to avoid the 3% forex markup. Save ~₹4,500 on a ₹1.5L ticket. Earn ₹0 in coins.

- Domestic India bookings (via Scapia app): Book all connections, hotel stays, and local travel through the Scapia app. Earn 20% coins = 4% back on travel spend.

- Everyday Indian spending (restaurants, retail): Use Scapia card. Earn 10% coins = 2% back.

- Airport lounge access in India: Unlock with ₹20,000 combined spend the previous month. Unlimited visits across 60+ airports.

One nuance worth flagging for NRIs: Scapia is a resident Indian credit card, not an NRI banking product. You will need an Indian address, a valid PAN, and an Indian mobile number to apply and maintain the account. If your Indian address and documentation are current, this is not a barrier. If you have let your Indian financial footprint lapse, you may need to update details with the bank before applying.

Verdict: Scapia vs IndusInd Avios vs Axis Atlas for Ireland-India travellers

Each card targets a different spend profile and travel pattern — the right choice depends entirely on your annual spend volume, the proportion of that spend on international transactions, and how much you value airline miles versus cash-equivalent travel credits.

| Feature | Scapia Federal Bank | IndusInd Avios Infinite | Axis Atlas |

|---|---|---|---|

| Annual fee | ₹0 — Lifetime free | ₹5,000 + GST | ₹5,000 + GST |

| Forex markup | 0% | 1.5% (chosen destination); 3.5% elsewhere | 3.5% |

| International earn | Zero coins | 3X–6X Avios per ₹200 (strong) | 2 EDGE Miles per ₹100 (competitive) |

| Domestic earn | 10% coins (2% cashback) | 3X Avios per ₹200 (~0.9% cashback equiv.) | 4–5 EDGE Miles per ₹100 (tier-dependent) |

| Travel booking earn | 20% coins via Scapia app (4% back) | 5X Avios on British Airways / Qatar Airways | 5 EDGE Miles per ₹100 on travel portals |

| Domestic lounge access | Unlimited (spend ₹20,000/month) | 2 per quarter + Priority Pass domestic | Tier-based: 4–12 international + domestic |

| International lounge access | None | 2 per quarter via Priority Pass | 4–12 per year depending on tier |

| Minimum income | ₹3 lakh/year; CIBIL 700+ | ₹10 lakh/year; CIBIL 750+ | ₹9–12 lakh/year; CIBIL 750+ |

| Miles transferable to airlines | No — travel cashback only | Yes — British Airways, Qatar Airways | Yes — 20+ airline/hotel partners |

| Best for | Frequent domestic traveller, cost-conscious spender | Europe/Gulf frequent flyer, business class redeemer | High-volume spender seeking miles flexibility |

- Occasional international traveller (1–2 trips/year, spend under ₹2L/year internationally): Scapia is the clear winner. Save on fees, earn on domestic spending, and keep ₹10,000 in annual fee costs in your pocket.

- Frequent flyer between Ireland and India (4+ trips, high hotel and flight spend): IndusInd Avios or Axis Atlas produce better value through transferable miles, despite the annual fee and higher forex markup. The business class redemption potential outweighs the fee delta.

- Hybrid traveller (mix of domestic India + occasional Europe): Carry both — Scapia for domestic India (no annual cost), and apply for IndusInd Avios or Atlas when income and credit score qualify. The cards serve different purposes and do not overlap.

Eligibility and how to apply for the Scapia credit card in 2026

The Scapia credit card has among the most accessible eligibility requirements of any travel card in India — a minimum annual income of approximately ₹3 lakh and a CIBIL score of 700 or above, compared to ₹9–12 lakh and CIBIL 750+ for premium cards. This makes it genuinely attainable for younger professionals, students on internship income, or those early in their credit-building journey.

The application process is entirely digital through the Scapia app, available on both the App Store and Google Play. There is no branch visit, no paper form, and no courier of physical documents in most cases. The app uses Aadhaar e-KYC and a live CIBIL pull to evaluate your application in minutes. If approved, a virtual card is activated immediately within the app, and your physical Visa and RuPay cards are delivered within 5–7 working days.

Key eligibility requirements as of June 2026:

- Age: 21–65 years for salaried applicants; 25–65 years for self-employed

- Residency: Indian resident or NRI with valid Indian address, PAN, and mobile number

- Income: Minimum approximately ₹3 lakh per annum (the app's credit model uses CIBIL rather than a strict documented income threshold)

- Credit score: CIBIL 700+ recommended; the card has been reported approved at lower scores for applicants with a Federal Bank account history

There is no joining fee, no first-year fee, and no spend-based waiver to track. The card is free permanently — which also means there is no renewal fee reminder to worry about if you use the card lightly for a few months. The credit limit is set by Federal Bank based on your CIBIL profile and can be reviewed upward after 6–12 months of responsible usage.

Frequently Asked Questions

Does the Scapia credit card charge a forex markup fee?

No. The Federal Bank Scapia credit card has a zero forex markup fee on all international transactions. You pay the standard Visa network exchange rate with no additional conversion charge.

Do I earn Scapia Coins on international spends?

No. International transactions earn zero Scapia Coins. The card saves you money on forex fees but does not reward you with coins for spending abroad. Domestic spends earn 10% coins; travel bookings via the Scapia app earn 20% coins.

What is the lounge access spend requirement on Scapia in 2026?

From 27 February 2026, you must spend ₹20,000 in the previous calendar month (across your Visa and RuPay cards combined) to unlock unlimited domestic airport lounge access for the following month. The threshold was doubled from the previous ₹10,000 requirement.

How much is one Scapia Coin worth?

5 Scapia Coins = ₹1, so each coin is worth ₹0.20. Redeeming 20% earned on ₹100 gives you 20 coins worth ₹4 - an effective travel cashback of 4% on Scapia app bookings.

Is the Scapia credit card good for NRIs who travel between Ireland and India?

For the India-leg of the journey - booking domestic flights, earning lounge access, and earning 10%-20% rewards on Indian spends - yes, Scapia is excellent and free. For the international leg (Europe-India), use a Wise card or another zero-forex debit card since Scapia earns zero coins on international transactions.

Ready to find the cheapest India fares from Dublin or London?

Once you have your Scapia card set up for the domestic India leg, use MyFlightOffers to compare live fares for the international segment — Dublin to Delhi, London to Mumbai, and more.

All card features, reward rates, fee structures, and eligibility criteria are based on publicly available information from Federal Bank, Scapia, and established financial review platforms as of June 2026. Card terms change — always verify current terms directly at scapia.cards and federal.bank.in/scapia before applying. MyFlightOffers is not affiliated with Scapia, Federal Bank, or any other financial institution mentioned. This article does not constitute financial advice.

- NEW Federal Bank Scapia Credit Card 2026 — This guide: zero forex, lifetime free, lounge access rules and NRI verdict

- Axis Bank Credit Cards for Flight Bookings 2026 — EDGE Miles, Atlas vs Magnus, Travel EDGE portal and April 2026 partner changes

- Transfer Indian Credit Card Points to Airline Miles 2026 — How to move HDFC, Axis, ICICI and IndusInd points to BA, Qatar, Air India and more

- Dublin to Delhi: Best Indian Bank Card Offers 2026 — Route-specific card discounts on Air India, EaseMyTrip and MakeMyTrip

- Airport Lounge Access Credit Card Guide 2026 — Domestic and international lounge networks compared across all major Indian cards