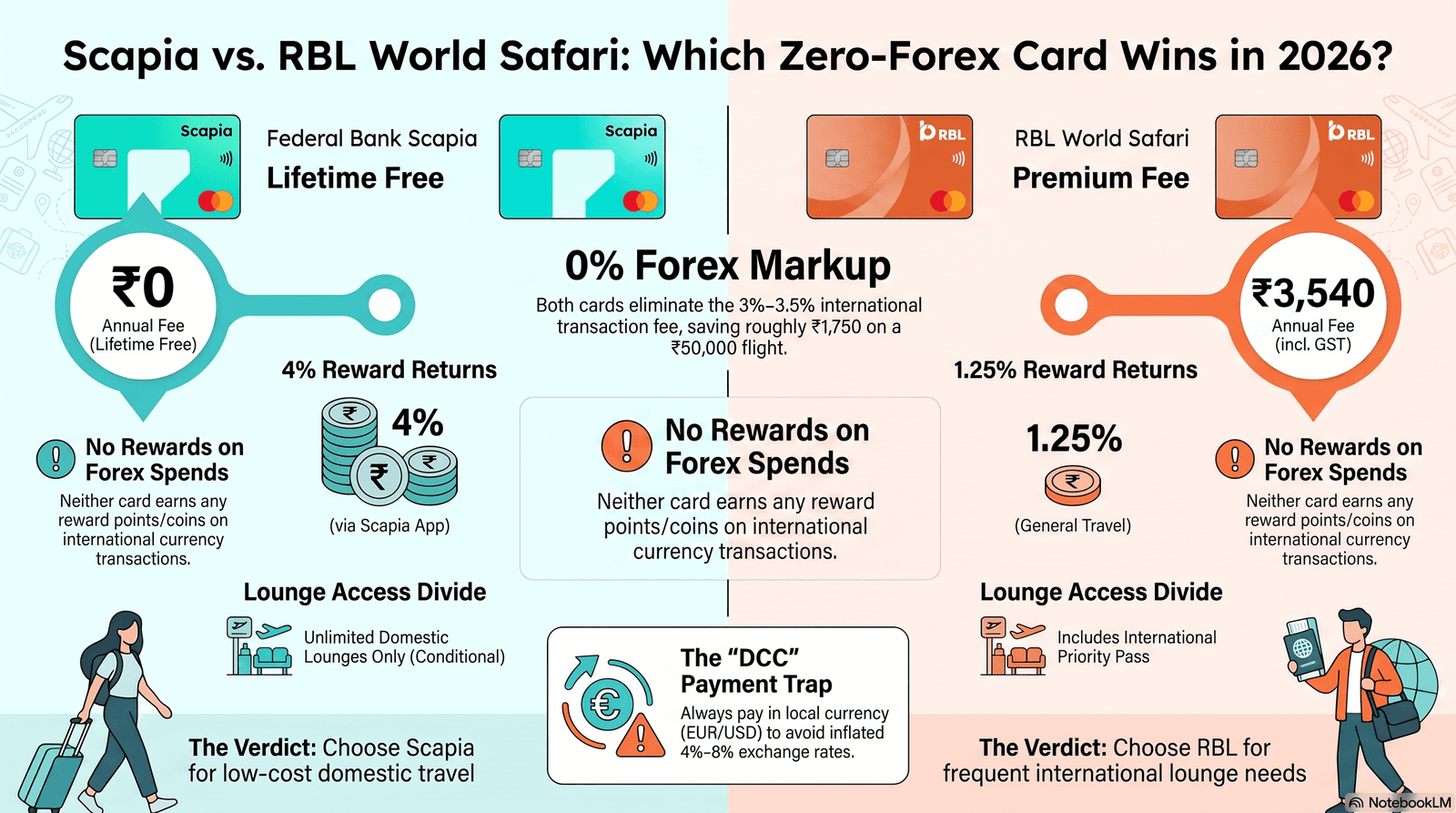

- Both cards charge 0% forex: You save 3%–3.5% on every international booking compared to a standard Indian card — but neither earns reward points on those international spends.

- Scapia is lifetime free; RBL Safari costs ₹3,540/year: Scapia earns 20% coins on bookings via its app; RBL Safari earns a modest 1.25% effective return on travel but bundles Priority Pass international lounge access.

- Verdict in one line: Choose Scapia if you book mostly through OTAs and want zero cost. Choose RBL World Safari if you value Priority Pass lounges and spend ₹3L+ per year on the card to justify the fee.

Quick Comparison

Scapia: ₹0 lifetime free

RBL Safari: ₹3,000 + GST

Both: 0% on all international spends

Scapia: 20% coins (Scapia app)

RBL Safari: 1.25%

effective (travel)

Scapia: None

RBL Safari: 2–6 free visits (Priority Pass)

In this guide

- Zero-forex card overview: what both cards actually do

- Fees and annual cost comparison

- Reward rates: Scapia Coins vs RBL reward points

- Airport lounge access rules 2026

- Flight discount portals and OTA offers

- Hidden charges: cash advance, late payment, redemption fees

- DCC trap and PoS arbitrage with zero-forex cards

- TCS and Indian cross-border payment rules (2026)

- Verdict: which card wins for Indian travellers in Europe and the US?

What do these zero-forex cards actually do for flight bookings?

Both the Scapia Federal Bank Credit Card and the RBL Bank World Safari Credit Card eliminate the foreign currency markup fee, which on a typical Indian card runs between 3% and 3.5% of every overseas transaction — saving you roughly ₹1,500–₹1,750 on a ₹50,000 international flight booking. This single feature is the primary reason both cards are popular among Indian travellers booking flights from Ireland or the UK to India, or booking European carriers directly on their foreign-currency websites.

However, the "zero-forex" label covers only the markup component. Both cards still convert your spend at the Visa/Mastercard mid-market rate published on the transaction date. Neither card earns any reward points or coins on international currency (forex) transactions — a critical caveat the marketing material buries in the fine print. Where they diverge sharply is in annual cost, reward architecture, lounge access, and which type of Indian traveller they are designed for.

What are the fees on each card in 2026?

The Scapia Federal Bank Credit Card is genuinely lifetime free — zero joining fee, zero annual fee, and no renewal charges — making it one of the rare premium travel cards in India with absolutely no cost of ownership. The RBL World Safari carries a joining fee of ₹3,000 and an annual renewal fee of ₹3,000 (plus 18% GST on each, totalling approximately ₹3,540 annually), partially offset by a MakeMyTrip welcome voucher worth ₹3,000 in the first year.

| Fee Type | Federal Bank Scapia | RBL World Safari |

|---|---|---|

| Joining Fee | ₹0 (lifetime free) | ₹3,000 + GST (~₹3,540) |

| Annual Renewal Fee | ₹0 | ₹3,000 + GST (~₹3,540) |

| Welcome Benefit | None (no fee to offset) | MakeMyTrip voucher ₹3,000 |

| Foreign Currency Markup | 0% (from 27 Feb 2026) | 0% |

| Cash Advance Fee | 2.5% (min ₹500) | 2.5% (min ₹500) |

| Interest Rate | Not disclosed in public KFS | 3.99%/month (47.88% APR) |

| Utility Bill Surcharge | 1% on bills >₹50,000 | Nil |

The effective cost of RBL World Safari in year 2 onwards is ₹3,540 with no guaranteed welcome benefit. To break even purely on fee recovery, you would need to extract at least ₹3,540 of value from reward points or lounge access — which, as we show in the sections below, is achievable but requires deliberate spend management.

How do the reward systems compare: Scapia Coins vs RBL points?

Scapia's reward architecture is more generous on the surface — 20% Scapia Coins on travel booked through the Scapia app and 10% on all domestic retail spends of ₹20 or more — but the coins are locked inside Scapia's own booking ecosystem, redeemable only for travel within the app. Every 5 Scapia Coins equals ₹1 (i.e. each coin = ₹0.20), so 20% coins equates to a genuine 4% effective return on Scapia-app travel bookings — a headline rate that beats virtually every other lifetime-free card in India in 2026.

RBL World Safari earns 5 reward points per ₹100 on eligible travel spends and 2 points per ₹100 on all other domestic retail. Each point is worth ₹0.25 when redeemed for flights or hotels via the RBL Rewards portal, making the effective return 1.25% on travel and 0.5% on general spend. A ₹99 + GST redemption processing fee is charged once per redemption day, and flight bookings via the portal attract a ₹200 convenience fee per passenger per sector.

| Earn Category | Federal Bank Scapia | RBL World Safari |

|---|---|---|

| Travel bookings (own app) | 20% Scapia Coins (= 4% effective return) | N/A — no own app |

| Travel spend (OTA/airline direct) | 10% coins (= 2% effective return) | 5 pts/₹100 (= 1.25%) |

| General domestic retail | 10% coins (= 2%) | 2 pts/₹100 (= 0.5%) |

| International (forex) spends | 0 coins | 0 points |

| Redemption options | Scapia app travel only | Flights, hotels, merchandise via RBL Rewards portal |

| Point/coin value | 5 coins = ₹1 | 1 point = ₹0.25 |

| Milestone bonuses | None specified | 10,000 pts on ₹2.5L; 15,000 pts on ₹5L; ₹10,000 voucher on ₹7.5L spend |

On-the-Ground Insight: "I've been using my Scapia card for six months for all my OTA bookings. The 10% coins on Cleartrip and EaseMyTrip add up surprisingly fast — I've already redeemed ₹4,200 back as travel credit. The catch is you're locked into their app, but for domestic routes it genuinely works." — Priya R., MSc Data Analytics, Dublin City University, Sept 2025 intake

Scapia Coins cannot be converted to airline miles, redeemed for cash, or transferred to third-party loyalty programs — a meaningful constraint for travellers who want to accumulate points towards a business-class award redemption. RBL World Safari points likewise have no airline transfer partner programme, but offer broader redemption flexibility including merchandise and gift vouchers.

What airport lounge access does each card provide in 2026?

This is the starkest difference between the two cards: RBL World Safari includes a complimentary Priority Pass membership granting access to over 1,400 international airport lounges worldwide, while Scapia provides no international lounge access at all.

RBL World Safari's lounge structure in 2026:

- International lounges: 2 complimentary visits per calendar year via Priority Pass. Spend ₹50,000 or more in the previous calendar quarter to unlock one additional free visit for that quarter — potentially 6 free visits per year for cardholders hitting the spend threshold every quarter. Additional visits cost $27 per visit.

- Domestic lounges: 8 visits per year (maximum 2 per quarter), conditional on spending ₹35,000 in the previous quarter. Covers all major DreamFolks-networked Indian airports.

Scapia's lounge structure in 2026:

- International lounges: None. This is a firm gap in the product.

- Domestic lounges: Unlimited domestic lounge access at 72 airports (expanded from the original 32 lounge-only network following Scapia's "Airport Privileges" launch), conditional on spending ₹20,000 in the preceding calendar month. Scapia extends this beyond traditional lounges to include dining, shopping, and spa at airport outlets.

- International airport benefits: Book an international flight of ₹50,000 or more through the Scapia app to get up to ₹2,000 back as rewards on duty-free shopping and dining at Indian international departure terminals.

| Lounge Benefit | Federal Bank Scapia | RBL World Safari |

|---|---|---|

| International lounges | ❌ None | ✅ Priority Pass — 2 free/year (up to 6 with quarterly spend) |

| Domestic lounges | ✅ Unlimited at 72 airports (₹20,000/month spend required) | ✅ 8/year (₹35,000 previous quarter spend required) |

| Network | Scapia Airport Privileges (lounges + dining + spa) | DreamFolks (domestic) + Priority Pass 1,400+ (international) |

| Overage cost | N/A | $27 per extra international visit |

For Indian diaspora in Ireland or the UK who transit through Dublin Airport or Heathrow, the Priority Pass benefit on RBL World Safari is practically useful — both airports have multiple Priority Pass lounges. However, many Indian travellers find that the lounge access conditional spend thresholds (₹35,000–₹50,000 per quarter) require genuinely active card use, not just a backup card kept for forex savings.

Which flight booking portals offer discounts for each card?

RBL World Safari cardholders can access live discount codes on ixigo and Yatra that reduce the effective ticket price beyond the zero-forex saving — the ixigo offer gives 10% off international flights (code IXRBLN, up to ₹2,500, minimum booking ₹10,000, once per month), while Yatra offers up to ₹10,000 off on select routes.

Scapia's discount mechanism is different: rather than portal-level coupon codes, Scapia builds the 20% coin earn rate into every booking made through the Scapia app — effectively a 4% price reduction on the booking cost, applicable every time rather than once a month. Scapia's OTA partners include Cleartrip, EaseMyTrip, and several hotel aggregators. The Scapia app also supports EMI conversion on large travel bookings, useful for students splitting a ₹60,000 semester-break flight across 3–6 months.

What are the hidden charges on each card?

Neither card is entirely cost-free beyond the advertised zero-forex promise — both levy a 2.5% cash advance fee (minimum ₹500), and RBL World Safari charges a ₹99 + GST redemption processing fee every time you redeem reward points.

The key hidden costs to know before choosing:

- Scapia utility bill surcharge: A 1% convenience fee applies on utility bill payments exceeding ₹50,000 per transaction via Scapia. This does not affect flight bookings.

- RBL redemption fee: ₹99 + GST is charged once per redemption day regardless of the number of transactions redeemed. Flight bookings via the RBL Rewards portal additionally carry a ₹200 convenience fee per passenger per sector — this can add ₹800 to a family of four on a one-way booking.

- RBL interest rate: At 3.99% per month (47.88% APR), revolving credit on RBL World Safari is expensive — fully clearing the statement balance every month is essential or the zero-forex saving evaporates instantly.

- Scapia coin expiry: Coins are forfeited if the account is closed or inactive. Always redeem before any planned account changes.

- Both cards: No earn on international spends, despite zero forex markup. A ₹1,00,000 international hotel booking earns zero coins/points on either card.

How do these cards handle DCC traps and Point-of-Sale arbitrage?

Dynamic Currency Conversion (DCC) is a payment trap where a foreign airline website or merchant offers to charge your Indian card in INR instead of the local currency — at a heavily inflated exchange rate that can add 4%–8% on top of the mid-market rate, completely negating the zero-forex benefit of either card.

When booking flights on European carrier websites (Aer Lingus, Lufthansa, British Airways) or US carriers, the payment page sometimes pre-selects INR as the billing currency. Always decline DCC and choose to pay in the local currency (EUR, GBP, USD). With Scapia or RBL World Safari, paying in local currency means you pay at the Visa mid-market rate with no markup — the optimal outcome. Accepting DCC means you effectively pay the bank's inflated rate regardless of which card you carry.

Point-of-Sale (PoS) arbitrage — checking whether booking on the Indian version vs. the international version of an airline's website gives a lower fare in INR vs. EUR — can yield savings of ₹2,000–₹5,000 on premium routes. For example, Air India's website shows different fare buckets depending on selected currency. With a zero-forex card, booking in EUR on the international site and converting at the mid-market Visa rate often undercuts the INR fare displayed on the Indian site. Always compare total landed cost in INR before committing.

What are the TCS and payment rules for using these cards internationally in 2026?

Under the Finance Act 2025 and Budget 2026 rules, Tax Collected at Source (TCS) on standalone international airline ticket purchases remains at 0% — there is no TCS on direct flight bookings regardless of which card you use.

The updated TCS thresholds as of 1 April 2026, sourced from the Income Tax Department of India and the Reserve Bank of India (RBI), are:

- Standalone air tickets: 0% TCS (unchanged — never applied to direct purchases).

- Overseas tour packages: Flat 2% TCS with no threshold (reduced from the previous 5%/20% structure by Budget 2026).

- Other LRS remittances (e.g., education, investments): 20% TCS above ₹10 lakh per financial year.

- Self-funded education and medical: 2% TCS above ₹10 lakh.

Both Scapia and RBL World Safari are Indian-issued credit cards falling under RBI's Liberalised Remittance Scheme (LRS) when used for overseas spends. Importantly, TCS collected is not a permanent loss — it is fully creditable against your advance tax liability or refundable when you file your annual income-tax return.

Verdict: which zero-forex card wins for Indian travellers in Europe and the US?

The right card depends entirely on your travel pattern and spending volume — there is no single winner across all profiles.

Net Annual Value = (Reward Coins/Points Earned) − Annual Fee − Redemption Fees

🧮 Zero-Forex Card Value Calculator

Enter your annual spend to see the net value each card delivers after fees and rewards — based on figures stated in this article.

Here is how the cards stack up across three real Indian traveller profiles:

| Traveller Profile | Best Card | Reason |

|---|---|---|

| Indian student in Ireland or UK (1–2 flights/year to India) | Scapia | Zero annual fee, 10%–20% coins on Scapia-app bookings. No lounge needed for 1–2 trips. Domestic Indian purchases earn coins too. |

| NRI professional (3–4 international trips/year, ₹3L+ card spend) | RBL World Safari | Priority Pass covers Dublin, Heathrow, and Indian hub lounges. Milestone bonus of 10,000 pts at ₹2.5L spend partially offsets ₹3,540 fee. |

| Frequent domestic Indian traveller (mostly India routes) | Scapia | Unlimited domestic lounge access on ₹20,000/month spend and 10%–20% coins on every booking beats RBL's capped 8-visit domestic lounge quota. |

| High spender seeking premium rewards (₹5L+/year) | RBL World Safari | 15,000 milestone points at ₹5L spend (= ₹3,750 value) plus Priority Pass effectively covers the annual fee if you hit the threshold. |

For most Indian students and early-career NRIs in Ireland, Scapia is the practical default — it costs nothing, eliminates the forex markup on all international bookings, and returns meaningful rewards on every Scapia-app transaction without any spend thresholds to chase. Its key weakness — no international lounge access — matters most if you have long layovers in hubs like Dubai, Doha, or Abu Dhabi. If that describes your routing, pair Scapia with a one-time Priority Pass day pass (available at most international airports for $30–$40) rather than paying ₹3,540/year for RBL World Safari's more limited 2-visit baseline.

If you are an NRI professional booking 4–6 international flights a year on premium carriers, spending ₹3L+ on the card, and regularly transiting through Priority Pass lounges, RBL World Safari's ecosystem of Ixigo, Yatra, travel insurance, and milestone bonuses can genuinely pay back the annual fee — but requires active management of quarterly spend thresholds to unlock lounge visits and avoid the $27-per-visit overage charge.

On-the-Ground Insight: "I switched from my HDFC Regalia to the Scapia card for all my Europe bookings after realising I was leaking 3.5% on every transaction. The coins add up quickly when you book four or five domestic Indian legs per year. My only regret is no international lounge access — I had to buy a day pass at Changi Airport for my Singapore connection." — Arun K., Software Engineer, relocated to Dublin, 2024

Cons of each card — in the interest of balance

Scapia cons: No international lounge access, coins locked inside Scapia's ecosystem, 0% earn on international spends, limited to Scapia's partner network for redemptions, and the high 20% earn rate requires routing bookings through the Scapia app specifically.

RBL World Safari cons: ₹3,540 annual fee with no guaranteed waiver, 0% earn on international spends, modest 1.25% effective return on travel (vs. Scapia's 4% on-app rate), lounge access conditional on quarterly spend thresholds, and redemption fees erode point value. International lounge access caps at just 2 visits without the quarterly spend.

Neither card is a clear winner for every traveller — and there is nothing stopping you from holding both, using Scapia for domestic and OTA bookings (where the coin rate dominates) and RBL World Safari specifically for Priority Pass access on international departures.

Ready to book your next flight? Compare live fares first

Use any zero-forex card to its full advantage — compare live fares across airlines, check cheapest months, and lock in your booking before the price moves.

- Airport Lounge Access India: Full Credit Card Guide 2026 — which cards give the best domestic and international lounge access in 2026.

- Axis Bank Flight Cards 2026: EDGE Miles, Atlas & Magnus — how Axis Atlas and Magnus compare against zero-forex alternatives for frequent flyers.

- How to Transfer Indian Credit Card Points to Airline Miles (2026) — converting reward points to Air India Flying Returns, Vistara Club Vistara, and InterMiles.

- TCS on International Travel Spend India 2026 — complete 2026 guide to TCS thresholds, LRS rules, and how to reclaim TCS at tax filing.

Card features, fees, lounge access conditions, and reward earn rates are sourced from official bank websites, PaisaBazaar, CardInsider, and 1Finance as of July 2026. Credit card terms change frequently — always verify current benefits directly with Scapia and RBL Bank before applying. TCS thresholds are sourced from Finance Act 2025 and Budget 2026 notifications from the Income Tax Department of India. This article does not constitute financial advice. MyFlightOffers is not affiliated with Federal Bank, Scapia, or RBL Bank.