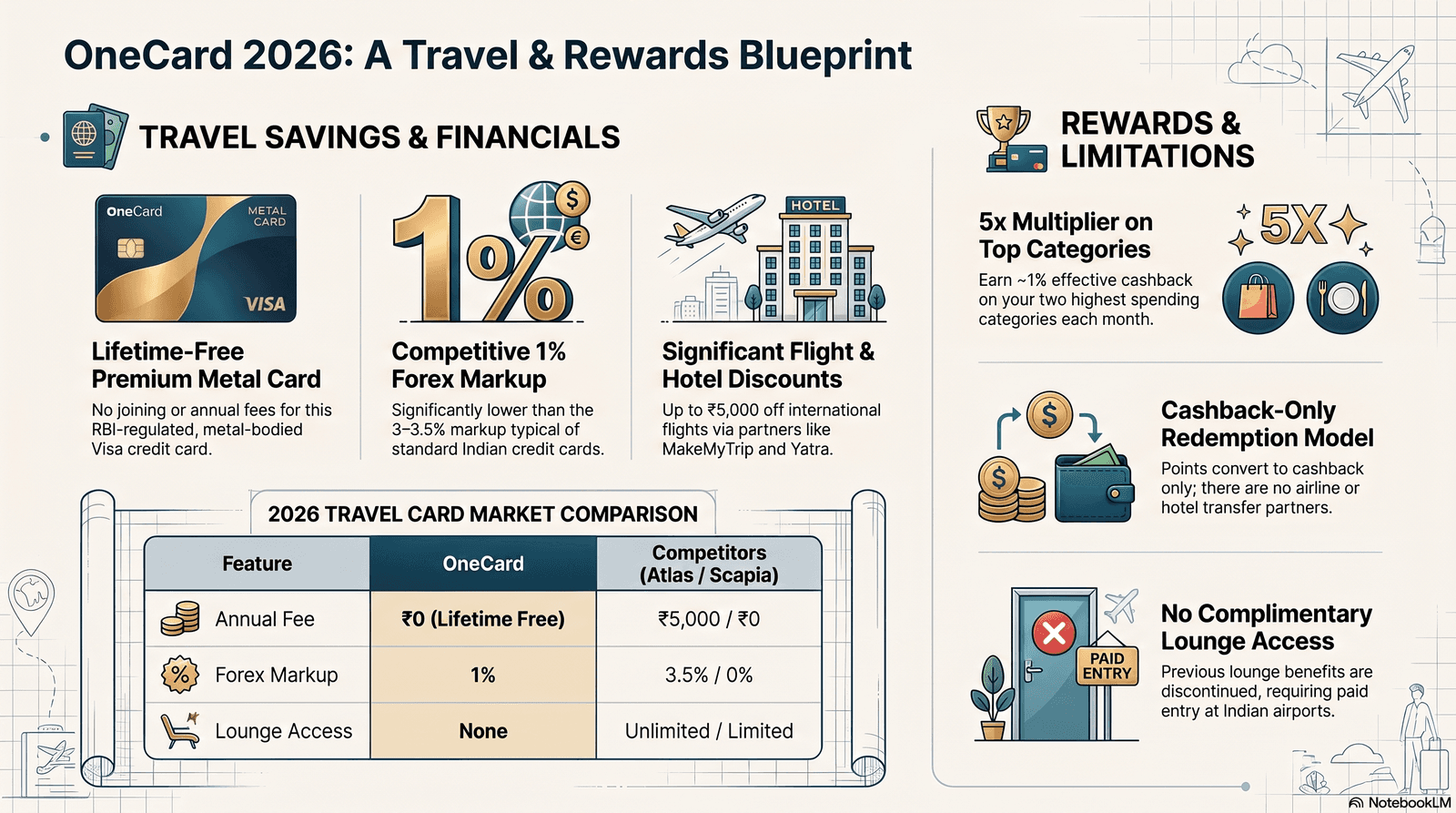

- Zero-fee metal card, low forex: OneCard charges ₹0 joining fee, ₹0 annual fee, and a 1% forex markup on international transactions — one of the lowest among free cards in India.

- 5x points, but no airline transfers: You earn 5x reward points on your top two spend categories each month (value: ~1% cashback), but there are no airline mileage transfer partners — points redeem as cashback only at ₹0.10 per point.

- No lounge access; regulatory note: OneCard does not offer airport lounge access in 2026. Additionally, the RBI directed a pause on new issuance in early 2026 (audit ongoing) — existing cards continue to work normally.

₹0 — Lifetime Free

1% on all international spends

1 pt per ₹50 → ₹0.10/pt = 0.2%

~1% cashback on top 2 categories

15% off domestic (max ₹1,500)

None

In this guide

- OneCard metal credit card: card features and partner banks

- How to earn 5x reward points on flights and travel

- Airline transfer partners: can you convert points to miles?

- Flight discounts: MakeMyTrip, Yatra, and EaseMyTrip offers

- International usage: 1% forex markup explained

- Airport lounge access: the honest picture for 2026

- TCS, OTP blocks, and DCC traps with OneCard

- OneCard vs Axis Atlas vs Scapia: comparison table

- Verdict: who should get the OneCard in 2026?

What is OneCard and which banks issue it in 2026?

OneCard is a lifetime-free metal credit card operated by FPL Technologies and issued in partnership with seven RBI-regulated scheduled commercial banks in India. The card runs on the Visa network and has a single unified rewards programme and app experience regardless of which bank underwrites your specific card.

The seven issuing banks as of July 2026 are BOBCARD (Bank of Baroda), CSB Bank, Federal Bank, IDFC FIRST Bank, SBM Bank India, South Indian Bank, and Indian Bank. When you apply through the OneCard app, an internal algorithm routes your application to the most appropriate issuing bank based on your credit profile and location.

The physical card is made of metal — a selling point that differentiates it from standard plastic credit cards and has historically been associated with premium products. You get a digital card instantly upon approval, with the physical card delivered in 3–5 business days. The card app (rated 4.6 on Google Play and 4.7 on the Apple App Store as of March 2026) lets you control transaction limits, toggle online/offline and domestic/international use, and view a Forex Calculator and Spends Planner in real time.

Key card charges to know upfront: there is no joining fee, no annual fee, and no reward redemption fee. However, an early closure fee of ₹3,000 applies if you cancel within the first six months of activation, and a metal card replacement fee of ₹3,000 applies if you request a new physical card. Fuel surcharge waiver is available up to ₹400 per month (100% surcharge waived).

How to earn 5x reward points on flights and hotel bookings

OneCard gives 1 reward point per ₹50 spent across all categories as the base rate, and 5x reward points (i.e., 5 points per ₹50) on your top two spending categories each month, provided you spend at least ₹750 in three different categories during that billing cycle. The effective cashback value at 5x is approximately 1% per rupee spent (5 pts × ₹0.10 = ₹0.50 per ₹50 = 1%).

For a frequent traveller, the 5x multiplier can apply to flight bookings and hotel stays if those are your biggest two spend categories in a given month. For example, if you spend ₹30,000 on flights and ₹8,000 on dining in a month, both categories qualify for 5x provided you also have a third category with at least ₹750 spend. That ₹30,000 flight spend would earn 3,000 points at 5x — worth ₹300 in cashback.

Reward points on OneCard never expire. Redemption is app-based: open the OneCard app, swipe right on a transaction, and points are applied as cashback against that purchase. There is no minimum redemption threshold and no redemption fee. The cashback is credited to your statement, reducing your outstanding balance.

At the base 1-point-per-₹50 rate (0.2% return), OneCard's reward yield is modest compared to dedicated travel cards. However, for a no-fee card used primarily in two consistent spend categories, the 1% return on those categories is genuinely competitive — especially combined with the low 1% forex markup for international bookings.

True Cost = Base Fare + Forex Markup (1%) + Lost Lounge Value (₹1,000–₹1,500 per visit) − 5x Cashback (up to 1%)

Example: ₹45,000 international ticket booked on OneCard = ₹45,000 + ₹450 (1% forex) − ₹450 (1% cashback at 5x) = net ₹45,000. The forex and cashback cancel out in the best case — but the missing lounge benefit costs you ₹1,000–₹1,500 per airport visit compared to premium travel cards.

Does OneCard have airline transfer partners for points to miles?

No — OneCard does not have any airline frequent flyer programme transfer partners in 2026. OneCard reward points can only be redeemed as cashback at ₹0.10 per point via the OneCard app. There is no option to transfer points to Air India Flying Returns, IndiGo BluChip, InterMiles, Vistara (Club Vistara programme, now merged with Air India), Emirates Skywards, or any other airline mileage programme.

This is a significant limitation for frequent flyers who want to leverage their spend for premium-cabin redemptions. Cards like the Axis Bank Atlas (EDGE Miles transferable to partner airlines) or the HDFC Infinia (SmartBuy points transferable to InterMiles and Singapore Airlines KrisFlyer) are better choices if airline mile accumulation is your priority.

OneCard's reward ecosystem is designed for simplicity: earn points, redeem for cashback. There is no points-to-miles conversion, no partner portals, and no award redemption complexity. For travellers who prefer direct cashback over managing multiple loyalty currencies, this simplicity is actually a feature. But for those who book business class or want premium redemptions, OneCard's closed reward loop means it will never be a primary travel card.

On-the-Ground Insight: "I got OneCard because it's free and the metal looks premium. But when I tried to use my points to book flights for my parents' trip to Dubai, I found out you can't — it's cashback only. I now use my HDFC card for flights to at least get airline points and just keep OneCard for everyday local spending." — Rishi M., Software Engineer, Bengaluru, OneCard user since 2024

OneCard flight discounts on MakeMyTrip, Yatra, and EaseMyTrip (2026)

OneCard has negotiated merchant-specific flight discounts with India's major online travel agencies, giving cardholders percentage discounts and flat-fee reductions on domestic and international bookings — subject to day-of-week and minimum booking amount conditions.

MakeMyTrip offers with OneCard (2026)

OneCard cardholders get 15% off on domestic flights (maximum discount ₹1,500) and 10% off on international flights (maximum discount ₹5,000) on MakeMyTrip, on bookings above ₹10,000, valid on Fridays and Saturdays only. These offers are time-limited and subject to MakeMyTrip's terms — always verify at the MakeMyTrip offers page before booking. The day-of-week restriction (Fri/Sat) means spontaneous mid-week booking plans won't benefit from these discounts.

Yatra offers with OneCard (2026)

On

Yatra, OneCard offers include flat ₹799 off per passenger on

domestic flights, 10% off international flights, 20% off

domestic hotel bookings, and 15% off bus tickets.

Yatra also runs EMI-linked promotional offers: flat 10% off (up to

₹1,500) on bookings above ₹10,000, flat ₹2,000 off on bookings

above ₹25,000, and flat ₹3,500 off on bookings above ₹50,000 — all

with no-cost 3-month EMI. The promo code

ONECARDEMI was valid through June 2026; check Yatra's

current offers page for the live promo code.

EaseMyTrip offers with OneCard (2026)

EaseMyTrip offers OneCard cardholders EMI on flight bookings with reduced interest rates, and periodic flat discounts on domestic and international flights. EaseMyTrip's OneCard page lists current offers — as of mid-2026, EMI-linked discounts of up to ₹1,000 on eligible bookings were available. Check the EaseMyTrip bank offers section before checkout for the current live discount.

Using OneCard internationally: 1% forex markup explained

OneCard charges a 1% forex markup on all international transactions, applied on top of the Visa network's mid-market exchange rate. This is substantially lower than the 3.5% forex markup charged by most standard Indian credit cards (HDFC, ICICI, SBI cards typically charge 3–3.5%), and competitive with dedicated zero-forex travel cards. However, it is not truly "zero-forex" — the 1% is a real cost.

To put this in context: if you book a €500 international flight (approximately ₹45,000 at June 2026 rates) using OneCard, the forex charge is approximately ₹450. With a card charging 3.5% forex (like a standard HDFC credit card), the same booking would cost ₹1,575 in forex markup — a difference of ₹1,125. At the 5x reward rate on this same booking, you'd earn approximately ₹450 in cashback, effectively making the net cost of the forex charge zero.

How to enable international transactions on OneCard

International transactions on OneCard are disabled by default and must be enabled manually through the OneCard app before making a foreign currency booking. Open the OneCard app, navigate to Card Controls (the card icon), toggle on "International Transactions," and set your spending limit. This must be done before attempting any booking on a foreign airline website or OTA that charges in a non-INR currency.

Dynamic Currency Conversion (DCC) trap — always pay in local currency

When booking on a foreign airline website, if the payment page offers to charge you in Indian Rupees (INR) instead of the local currency (USD, EUR, GBP), always decline — this is a DCC offer and typically adds 4–8% above the mid-market rate. On OneCard, paying in INR via DCC means you lose the benefit of the 1% Visa exchange rate and pay the airline's or payment processor's inflated conversion rate instead. The one-word rule: always choose to pay in the local currency of the country where the airline is incorporated.

Example: booking a Lufthansa flight on the German website in EUR at ₹45,000 equivalent, OneCard's 1% forex = ₹450. If you accept DCC and pay in INR at a 5% conversion, that's ₹2,250 — a ₹1,800 avoidable cost.

Does OneCard offer airport lounge access in India? (2026 reality check)

No — OneCard does not provide complimentary domestic or international airport lounge access in 2026. The card previously offered lounge access through DreamFolks, India's primary airport lounge aggregator. However, following disruptions in the DreamFolks ecosystem and OneCard's own product evolution, this benefit was discontinued and was not reinstated as of July 2026.

This is one of the most significant practical limitations of the OneCard for regular flyers in India. Domestic airport lounge access at Tier 1 airports typically costs ₹1,000–₹1,500 per visit (at Chennai, Hyderabad, or Delhi T2) to ₹2,000+ at international terminals. A frequent flyer taking four round trips per year (eight lounges) would spend ₹8,000–₹16,000 that a premium travel card user would access free.

If lounge access is important to you, OneCard is the wrong primary travel card. Alternatives with free lounge access include the HDFC Regalia (12 domestic visits/year), Axis Bank Magnus (unlimited via DreamFolks/Priority Pass), or the ICICI Sapphiro (8 domestic visits/year). For a no-fee card, the Federal Bank Scapia (covered in our Scapia review) offers no-fee lounge access in limited form.

TCS on international flight booking with OneCard: what you need to know

Tax Collected at Source (TCS) at 20% applies to overseas remittances above ₹7 lakh per financial year under the Liberalised Remittance Scheme (LRS), but direct airline ticket purchases using a domestic credit or debit card at face value are generally exempt from TCS — you pay the fare and the payment is settled domestically.

The distinction matters significantly for OneCard users: if you book a ₹45,000 international flight directly on an airline website or an Indian OTA (MakeMyTrip, Yatra), no TCS applies — you are simply paying a rupee-denominated invoice. TCS is triggered for overseas remittances (sending money abroad), forex card loading, and certain overseas tour packages. The Income Tax Department of India's 2023 amendment clarified that direct purchases of international airline tickets via Indian debit/credit cards do not fall under the LRS umbrella and are not subject to TCS.

However, if you load a forex card using OneCard (which is not directly possible — OneCard is not a forex card loading method), or if you transfer money abroad to pay for tours, TCS at 20% would apply above the ₹7 lakh annual threshold. Reclaiming TCS paid is possible by claiming it as advance income tax paid when you file your annual ITR.

- Direct airline ticket booking (Indian OTA or airline direct): No TCS, regardless of amount.

- Overseas tour package (hotel + transport bundled by agent): TCS at 5% on the first ₹7 lakh, 20% above ₹7 lakh.

- Foreign currency remittance under LRS (Liberalised Remittance Scheme): TCS at 20% above ₹7 lakh/year. This is not triggered by a standard OneCard flight booking.

- Education remittance via loan: 0.5% TCS above ₹7 lakh.

OneCard vs Axis Atlas vs Scapia (Federal Bank): full comparison table 2026

The right card depends on whether you prioritise zero cost of ownership, airline miles accumulation, or lounge access. The table below compares OneCard against the Axis Bank Atlas (the benchmark premium travel card) and the Federal Bank Scapia (the main zero-forex competitor also targeting the no-fee segment).

| Feature | OneCard (FPL Tech) | Axis Bank Atlas | Federal Bank Scapia |

|---|---|---|---|

| Annual Fee | ₹0 (lifetime free) | ₹5,000 + GST | ₹0 (lifetime free) |

| Forex Markup | 1% | 3.5% | 0% |

| Reward Rate (Base) | 0.2% (1 pt / ₹50) | 2 EDGE Miles / ₹100 | 2% in Scapia coins (travel) |

| Reward Rate (Boosted) | ~1% on top-2 categories | 5 EDGE Miles / ₹100 on travel | Up to 4% on travel partners |

| Airline Transfer Partners | None | Air India, Singapore Airlines, IndiGo, others | None |

| Airport Lounge Access | None | Unlimited (Priority Pass + DreamFolks) | Limited (spend-linked, select airports) |

| Card Material | Metal | Metal | Plastic |

| Network | Visa | Visa | Visa |

| Welcome Benefit | None | 2,500 EDGE Miles on first transaction | One complimentary lounge visit |

| Fuel Surcharge Waiver | Up to ₹400/month (100%) | Yes (1% surcharge, varying cap) | Not specified |

| Application Status (Jul 2026) | Paused (RBI audit) | Paused (Axis closed new apps) | Open |

| Best For | First free metal card, everyday cashback | Premium travel, airline miles, lounges | Zero-forex international spends |

Sources: OneCard official website, Axis Bank Atlas card page, Magnify Club OneCard review 2026, Forbes Advisor India OneCard review 2026.

Point of Sale (PoS) arbitrage — does it work with OneCard?

Yes, PoS arbitrage — booking on a foreign regional version of an airline website to access lower published fares — works with any Visa card including OneCard, as long as international transactions are enabled. For example, British Airways' India website (ba.com/in) sometimes shows different fares in INR compared to the UK site (ba.com) in GBP. With OneCard's 1% forex, the GBP fare might still be cheaper even after conversion. Always run the comparison manually: check the fare in local currency on the airline's home-market website, convert at the current Visa rate, add 1%, and compare against the Indian site's INR price.

🧮 OneCard Annual Travel Value Calculator

Estimate your annual cashback and forex savings from OneCard based on your spending profile — and compare it to a paid travel card.

Verdict: who should get the OneCard credit card in 2026?

OneCard is the best free entry-level metal credit card for Indian consumers who want a no-cost travel companion for OTA flight discounts, low-forex international spending, and cashback on everyday categories — but it is the wrong choice for frequent flyers who need lounge access or airline miles.

Get OneCard if: You are a moderate traveller taking 2–4 flights per year, primarily booking on MakeMyTrip or Yatra where the merchant discounts provide genuine value. You prefer cashback simplicity over managing multiple loyalty currencies. You want a low-forex card for occasional international spending without paying an annual fee. You are building your credit history and want a premium-looking metal card that costs nothing to hold.

Do not make OneCard your primary travel card if: You fly frequently (more than 6 times per year) and need lounge access — the absence of lounge benefits will cost you ₹8,000–₹16,000 in paid lounge fees annually. You want to accumulate airline miles for premium cabin redemptions — OneCard's no-transfer policy means you cannot access business class award seats via points. You need a truly zero-forex card — the 1% markup is low but not zero; consider the Scapia card (0% forex) as a companion or replacement.

- Pros: Zero annual fee, metal card, 1% forex markup, 5x rewards on top-2 categories (~1% cashback), MakeMyTrip and Yatra flight discounts, lifetime-free with no reward expiry.

- Cons: No lounge access, no airline transfer partners, 2026 RBI-mandated new issuance pause, 0.2% base reward rate is modest, 5x requires disciplined spend in three categories, ₹3,000 early closure fee.

- Best paired with: The HDFC Regalia (lounge access) or Axis Bank Atlas (airline miles) for a two-card travel wallet that covers what OneCard lacks.

Find the cheapest fares on your next international route

Compare live flight prices across airlines for your route from Dublin, London, or India — and combine with the right card offer to maximise savings.

All card features, fees, reward rates, and promotional offers cited in this article are based on publicly available official sources as of July 2026. Credit card terms change frequently; always verify current fees, reward rates, and OTA offers directly on the OneCard official website, MakeMyTrip, and Yatra before booking. The 2026 RBI audit status may affect card availability — confirm issuance status before applying. This article does not constitute financial advice. MyFlightOffers is not affiliated with OneCard, FPL Technologies, or any issuing bank mentioned.

- NEW Federal Bank Scapia vs RBL World Safari: Best Zero-Forex Card for Flights 2026 — head-to-head on zero-forex cards for international flight bookings

- Axis Bank EDGE Miles, Atlas & Magnus: Complete Flight Booking Guide 2026 — airline transfer partners, lounge access, and the Atlas EDGE Miles earn rate compared to OneCard

- Airport Lounge Access India 2026: Which Credit Cards Get You In Free? — the full lounge access landscape since OneCard removed the benefit

- How to Transfer Indian Credit Card Points to Airline Miles (2026) — alternatives to OneCard's cashback-only model for frequent flyers