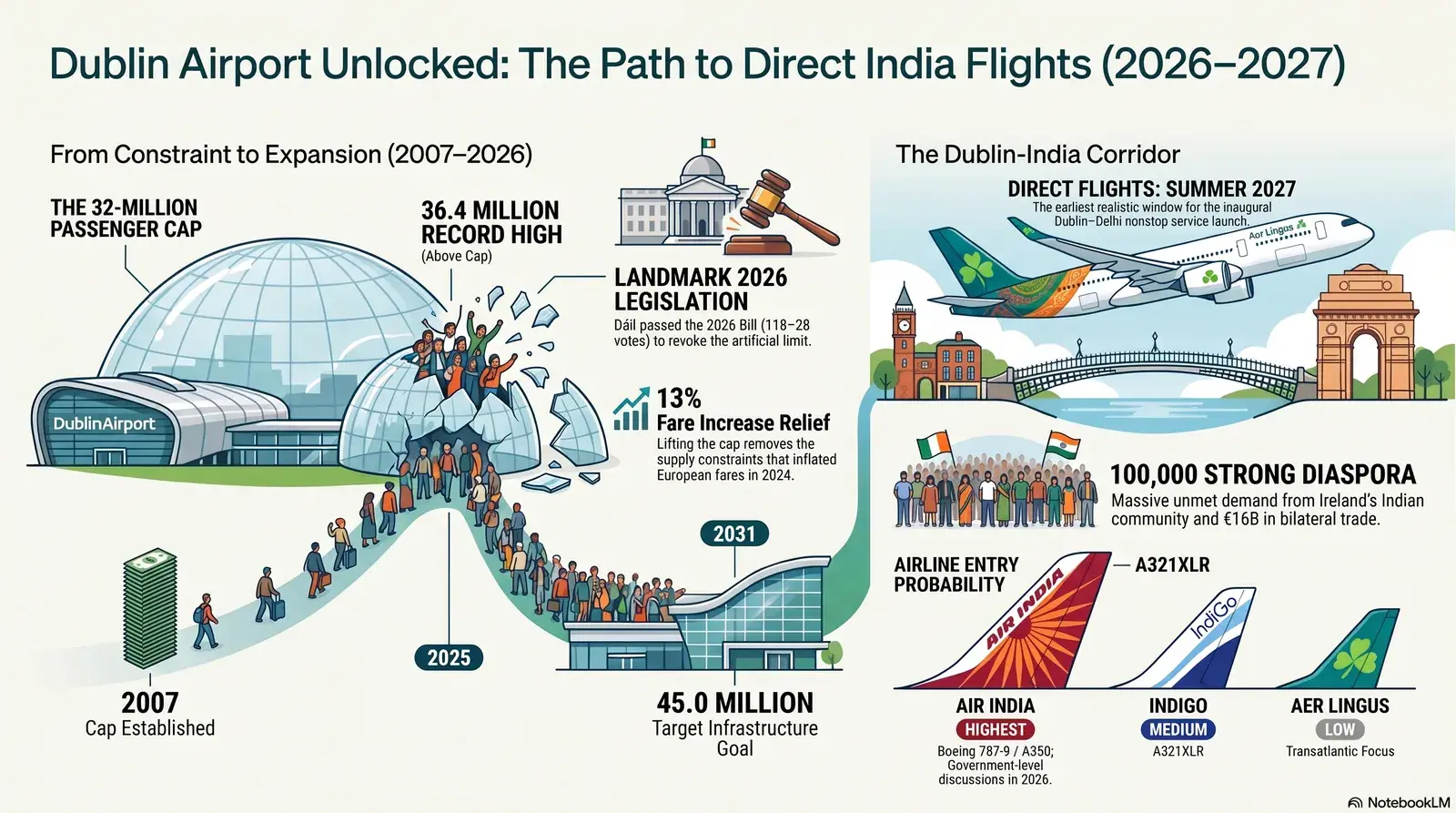

- Cap is effectively gone: Ireland's Dáil passed the Dublin Airport (Passenger Capacity) Bill 2026 on 30 June by 118 to 28 votes. Enforcement was already suspended by the High Court; the new law gives the Minister power to formally revoke the 32‑million limit.

- Direct India flights are possible but not yet confirmed: Minister Chambers met Air India and IndiGo in February 2026 and expressed hope for a direct Ireland–India route within two years. Summer 2027 is the earliest realistic launch window for a Dublin–Delhi service.

- Fares should improve long-term, but don't expect drops overnight: The cap drove a 13% fare increase on European routes in winter 2024/25. Greater capacity removes that artificial floor — but new routes and terminal infrastructure take 18–36 months to materialise.

32 million passengers per year

36.4 million (record high)

118 For — 28 Against

No confirmed launch; Summer 2027 possible

1. The 32‑Million Passenger Cap Story: 2007 Planning Condition to 2026 Dáil Bill

The 32‑million annual passenger cap at Dublin Airport originated in 2007 as a planning condition imposed by An Bord Pleanála when it granted permission to build Terminal 2 — and it was never designed to be permanent. The condition set a ceiling on combined passenger throughput across both terminals until further planning permission was obtained, primarily because the development plan at the time raised concerns about road congestion and airport-related traffic growth in north County Dublin.

The cap was not a standalone capacity law — it was a condition embedded in a single planning permission. It specified that the combined capacity of Terminal 1 and Terminal 2 would not exceed 32 million passengers per annum unless authorised by a further grant of planning permission. The 2006 development plan, which has since expired, had actually envisaged traffic growing to 38 million passengers by 2025 and contemplated a third terminal on the western side of the campus to handle growth above 30 million. That third terminal was never built, the plan elapsed, and the 32‑million cap remained as an orphaned constraint.

For years, the condition was manageable. Dublin Airport's traffic was comfortably below the cap through the 2010s. Then, as Irish aviation rebounded strongly from COVID-19, passenger numbers grew faster than expected — and by 2022 it was clear that the cap would bind within a few years. DAA (Dublin Airport Authority) launched a public campaign to have the cap removed and warned that the planning condition was deterring airlines from committing to new long-haul routes, particularly to India, Brazil, and emerging markets in Asia.

2. Timeline: High Court Stay, Record 36M Passengers, and the July 2026 Legislation

Despite the cap technically remaining in force, Dublin Airport was already operating above 32 million passengers thanks to a series of High Court stays — and the Dáil formally passed legislation to end the limit on 30 June 2026. Here is the sequence of events that brought Ireland to this point.

| Date | Event | Significance |

|---|---|---|

| 2007 | An Bord Pleanála grants permission for Terminal 2 with 32M passenger cap condition | Cap born as planning condition, not standalone law |

| 2022 onwards | Post-COVID recovery pushes DUB traffic toward the cap | Enforcement risk emerges; airlines begin to hesitate on new routes |

| 2023–2025 | Residents' group (St Margaret's The Ward Environmental DAC) applies for enforcement order; DAA seeks High Court stay | High Court grants stays; cap enforcement suspended pending EU Court of Justice (CJEU) referral |

| 2025 full year | Dublin Airport handles 36.4 million passengers — a record, and 4.4M above the cap | Confirms cap is being breached; fares on European routes rise 13% in winter 2024/25 (IAA slot allocation effect) |

| February 2026 | Cabinet approves priority drafting of the Dublin Airport (Passenger Capacity) Bill 2026 | Minister Darragh O'Brien gets statutory power to amend or revoke the cap |

| March–June 2026 | Bill progresses through Oireachtas; US airlines threaten Open Skies implications if cap persists | Political pressure intensifies; Sinn Féin backs government to pass bill |

| 30 June 2026 | Dáil passes the bill 118 to 28 | Bill passes to Seanad; Social Democrats, Labour, PBP, Greens vote against |

| July–September 2026 | Seanad debate; cap formal revocation expected by September 2026 | Minister could sign the order removing the cap once Seanad passes the bill |

The 13% fare rise in winter 2024/25 deserves emphasis because it was directly caused by the Irish Aviation Authority (IAA) applying the cap when allocating slots. Under EU Slot Regulation, available capacity must preferentially be allocated to airlines holding historic slots. An airport constrained by an annual passenger cap cannot facilitate any additional traffic for new routes or new entrants at any time of day or year. The result was that Dublin Airport in winter 2024/25 had the highest fare growth of any top-80 European airport. When the High Court later suspended enforcement, capacity rose and fare growth slowed — a direct demonstration of the cap's cost to passengers.

3. What Cap Removal Means for New Routes: India and South America Connectivity

DAA has explicitly cited "significant unmet demand for connectivity between Ireland and South America, India and other fast-growing destinations," arguing that cap uncertainty is the primary reason airlines have not committed to these routes. With the legislation passed, airlines can now model new routes against a stable, unconstrained airport rather than one that might be forced to reduce traffic mid-summer.

There are two separate mechanisms by which the cap was blocking new routes. First, under EU slot rules, any new airline wanting to launch a new route from Dublin during a constrained season had no available slots to bid for — there simply was no headroom within 32 million. Second, even if a carrier had slots, the legal uncertainty (the CJEU referral, the residents' injunction, the risk that enforcement could be re-imposed) made it impossible to file routes or sell tickets 12–18 months in advance as airlines normally do for new long-haul launches. No commercial airline will commit a widebody aircraft to a brand-new route under those conditions.

A notable early signal of post-cap optimism: China Eastern Airlines launched a three-weekly Dublin–Shanghai nonstop on 20 July 2026 using an A350-900 — Dublin's longest nonstop at approximately 5,800 miles. While the Shanghai route had been in planning before the legislation passed, it demonstrates what became possible once Ireland's political direction on the cap was clear. A direct India route is a different proposition — longer preparation time, different market dynamics — but the precedent is established.

On-the-Ground Insight: "I have been flying Dublin to Hyderabad via Doha every Christmas for five years. Every year it gets harder to get a decent fare because the same Qatar flight gets more popular but there's no new capacity from Dublin. If a direct Air India flight to Delhi launches in 2027, I would switch in a heartbeat — even if it costs a bit more — just for the convenience of not doing a three-hour overnight layover." — Priya R., Senior Engineer, Dublin, Irish resident since 2019

4. Will a Direct Dublin–Delhi or Dublin–Mumbai Flight Finally Happen?

A direct Dublin–India service is not confirmed, but it has moved from speculative to plausible: in February 2026, Minister Jack Chambers met Air India and IndiGo representatives and stated that the government hopes for a direct Ireland–India flight within two years. Summer 2027 is the earliest realistic window, with Dublin–Delhi (DEL) identified as the most likely inaugural route.

The commercial case is genuine. Ireland has an Indian diaspora of approximately 100,000 people — one of Europe's largest relative to national population — and bilateral trade between Ireland and India amounts to over €16 billion. Two-way tourism and business travel is constrained by the absence of a direct link; every passenger must today transit through Dubai (DXB), Doha (DOH), Abu Dhabi (AUH), Frankfurt (FRA), or London Heathrow (LHR).

| Airline | Route probability | Aircraft type likely | Earliest launch window | Key condition |

|---|---|---|---|---|

| Air India | Highest — government-level discussions confirmed Feb 2026 | Boeing 787-9 or Airbus A350 (new order delivery) | Summer 2027 | Aircraft availability; Tata Group fleet delivery schedule |

| IndiGo | Medium — long-haul ambitions stated but limited widebody fleet | A321XLR (not yet confirmed for India–Ireland range) | 2027–2028 | A321XLR range vs DUB–DEL distance (6,750 km) — tight but possible |

| Aer Lingus | Low — no stated India intention; transatlantic focus | N/A | N/A | Would need to source widebody with India range |

| Emirates / Qatar / Etihad | Very Low for nonstop — these carriers benefit from hub connections | N/A | N/A | A nonstop cannibalises their hub transfer revenue |

Travellers should be realistic: cap removal removes a deterrent but does not guarantee a direct route. Airlines need to secure aircraft (Air India's Tata-era fleet modernisation is still in progress), agree commercial terms with DAA, file route applications with regulators, and sell seats across an IATA scheduling cycle. The sequence from "announcement" to "first flight" on a brand-new long-haul route typically takes 12–18 months. If an announcement comes in late 2026, passengers could be booking for summer 2027 by early 2027.

5. Impact on Fares: More Capacity on Gulf Carrier and European Hub Routes

The cap removal is ultimately a supply-side intervention: more capacity tends to put downward pressure on fares, but only once that capacity actually exists on aircraft — which for new long-haul routes can take 18–36 months from legislation to seat. For the India corridor specifically, the short-term picture is more nuanced than "fares will drop."

Here is the mechanism that matters. The cap constrained slot allocation at Dublin Airport, which particularly hurt carriers trying to add new frequencies. Emirates, Qatar Airways, and Etihad Airways all serve Dublin, but each was operating within a constrained airport environment. Gulf carriers have long wanted to add additional frequencies on the DUB–DXB, DUB–DOH, and DUB–AUH routes — more flights mean more connecting passengers reaching Indian cities. With the cap removed, these carriers can apply for additional slots, and if granted, competition on the critical Gulf gateway sector should grow.

More DUB–Dubai, DUB–Doha, or DUB–Abu Dhabi frequencies → more seat capacity to Gulf hubs → more connecting options to India → downward pressure on DUB–India via-Gulf fares. But the structural fare logic still applies: Dublin–India round trips are dominated by married-segment fares in GDS systems, and the DUB–Gulf sector pricing is treated as part of the long-haul fare bucket, not standalone short-haul. You cannot independently compare a DUB–DXB fare to a DXB–BOM fare and add them together — the airline prices the full itinerary as a unit.

For winter 2026/27 specifically, fare conditions are unlikely to change dramatically. The legislation only passed in July 2026; airlines file winter capacity months in advance, and the IATA winter 2026/27 schedule was locked in during the spring. The meaningful change in seat supply on the Dublin–India corridor will most likely first appear in summer 2027 and subsequent seasons, when airlines have had time to act on the new capacity headroom.

One additional fare factor is the EU–India trade deal that was under negotiation through 2026. A bilateral aviation agreement between the EU and India — which would remove flight frequency caps under existing bilateral Air Services Agreements — could further expand the number of weekly frequencies any airline is permitted to operate between Ireland and India. This is a separate process to the Dublin Airport planning cap but complementary to it.

6. Terminal Expansion and North Runway Utilisation: What Travellers Will Notice

Dublin Airport's capacity ambitions do not stop at the legislative cap — DAA submitted a €2.9 billion Infrastructure Application to Fingal County Council seeking permission to expand the airport to 40 million passengers, with a longer-term 2031 goal of approximately 45 million. The planned physical expansions will directly affect the passenger experience for anyone transiting Dublin.

The two headline projects are:

- Pier 5 East — a new pier that could accommodate approximately 3 million additional passengers per year, primarily serving inbound US tourists (benefiting from Dublin's US pre-clearance facility).

- Pier 1 East — an extension that would add up to 7 million passengers per year of capacity, targeted at European and some long-haul traffic.

Combined, these projects would add around 10 million annual passengers of capacity — taking Dublin from its current effective cap of around 36–37 million (in practice) to a theoretical 45–47 million. A new integrated transport centre and expanded aircraft stands are also included in the plans.

The North Runway, which opened in 2022 at a cost of approximately £270 million (equivalent), runs 3,110 metres and sits 1.69 km north of the existing main runway. It was designed to allow simultaneous operations in certain wind conditions, reducing departure delays during peak periods. As passenger volumes grow post-cap, the North Runway's full utilisation — particularly for early-morning long-haul departures and late-night arrivals — will become more important. Indian students arriving on red-eye connections from Dubai or Doha may find a more fluid experience as the airport optimises runway use.

One note of caution: the infrastructure application is separate from the passenger cap legislation and is subject to its own planning process. Ryanair chief executive Michael O'Leary has publicly clashed with DAA over the €5.6 billion broader expansion vision (a figure that includes longer-term phases beyond the initial IA), arguing that DAA's passenger charges and infrastructure costs are too high. The commercial and regulatory process around airport charges — set by the Commission for Aviation Regulation (CAR) — will determine whether capacity expansion actually happens at the pace DAA projects.

7. What Indian Students and NRI Travellers Should Do: Booking Strategy for Winter 2026/27

For the December 2026 / January 2027 travel window — the peak India season for Dublin-based students and NRI families — the practical booking advice is to act as you would in any capacity-constrained environment: book early, know your carrier, and use your Indian bank card strategically.

Here is what has not changed yet. Dublin to India via Gulf hubs (Emirates via DXB, Qatar Airways via DOH, Etihad via AUH) remains the dominant route structure. No direct flight exists. The airlines and their connecting hubs for the current season are the same. Where the cap removal matters most is in the medium term (2027 onwards); for winter 2026/27, book on the same basis as previous years but keep an eye on additional Gulf frequencies that carriers may add for the winter season.

Booking windows for December 2026: fares typically bottom out 3–4 months before departure on the Dublin–India corridor, then climb steeply as seats fill. For Christmas week (22–26 December) and first week of January, the ideal booking window is August–September 2026. Waiting until October or November means paying a significant premium. For Easter 2027, the window opens from November 2026.

Fare strategy given current dynamics: With the cap no longer artificially constraining new Gulf carrier frequencies, you may see new DUB–DXB or DUB–DOH departure times emerge for winter 2026/27. Check Emirates, Qatar, and Etihad directly for schedule updates from August 2026 — their IATA winter 2026/27 schedules become bookable from late July. If a new early-morning Dublin departure to Dubai appears, it opens up same-day connection options to Mumbai, Delhi, Chennai, Hyderabad, and Bengaluru that were not previously feasible.

Indian bank card considerations: If you are booking from India using an Indian-issued card, two things to check before you hit confirm. First, ensure your card's international transaction limit is set high enough — a Dublin–Delhi round trip via a Gulf carrier can easily exceed ₹80,000–₹1,20,000. Call your bank or use mobile banking to raise the daily online transaction cap before booking, as a failed transaction on a popular flight can mean losing the fare while the hold-pending window expires. Second, book in the origin currency (EUR from Irish OTAs, or the airline's own EUR site) rather than allowing dynamic currency conversion (DCC) to convert to INR at the checkout — the DCC rate typically adds 4–8% above mid-market.

Student-specific angle: If you are an Indian student on a Stamp 2 visa in Ireland, your primary Christmas booking concern is seat availability on the 22–24 December departure window, which is the most heavily booked. Consider flying out slightly earlier (17–21 December) or returning slightly later (3–6 January) — fares in those shoulder dates are often 25–40% cheaper than the peak week. Carry-on only is rarely viable on Dublin–India routes given baggage allowance norms; factor in checked-bag costs when comparing total trip price across airlines.

Looking ahead to summer 2027: If Air India or IndiGo files a Dublin route at the IATA Slot Conference in October/November 2026, fares will likely go on sale 3–6 months before the inaugural flight. Set a Google Flights price alert for DUB–DEL and subscribe to MyFlightOffers fare alerts for the Dublin–India route — a new entrant on this corridor historically produces a significant, if temporary, fare reduction as the carrier fills seats in its opening months.

At a Glance: Dublin Airport Cap — Before vs. After

The table below summarises the key changes across dimensions that matter to India corridor travellers, comparing the constrained-cap era to the post-legislation environment.

| Dimension | Under the 32M Cap (pre-July 2026) | Post-Legislation (July 2026 onwards) |

|---|---|---|

| Annual capacity headroom | None — airport already at 36.4M with cap at 32M | Unconstrained; planning applications targeting 40–45M |

| European route fares (winter 2024/25) | +13% year-on-year — highest of Europe's top 80 airports | Expected to stabilise as slot allocation is no longer capped |

| New long-haul routes (India/Brazil) | Deterred by legal/slot uncertainty | Airlines can commit; Air India/IndiGo in talks for Summer 2027 |

| Gulf carrier frequencies (DXB/DOH/AUH) | Constrained by slot availability under the cap | Additional frequencies possible from summer 2027 |

| Dublin Airport infrastructure | North Runway open since 2022; further expansion blocked | €2.9bn IA under planning review; Pier 5E and Pier 1E projects |

| Direct Dublin–India flight | Not possible while cap created slot uncertainty | Plausible for Summer 2027 — Air India/IndiGo priority targets |

Frequently Asked Questions

- Has Dublin Airport's 32 million passenger cap been officially removed?

- Yes. The Dáil passed legislation on 30 June 2026 (118 votes to 28) giving the government power to lift the 32‑million passenger cap. The cap was an An Bord Pleanála planning condition from 2007. The bill removes that statutory constraint, though physical capacity will still expand in stages as infrastructure is built.

- Will a direct Dublin to India flight launch because of the cap removal?

- Minister Jack Chambers met Air India and IndiGo in February 2026 and expressed hope for a direct Ireland–India flight within two years. Cap removal removes a key deterrent for airlines evaluating the route. Summer 2027 is the earliest realistic launch window for a Dublin–Delhi service, but no airline has committed a schedule yet.

- How did the passenger cap affect flight fares at Dublin Airport?

- Fares on European routes at Dublin Airport rose 13% year-on-year in winter 2024/25 — the highest increase among Europe's top 80 airports — because the Irish Aviation Authority applied the cap when allocating slots, preventing new capacity from entering the market. When the High Court suspended enforcement, capacity rose and fare growth slowed.

- What is Dublin Airport's current passenger capacity plan?

- Dublin Airport handled 36.4 million passengers in 2025, already above the now-removed 32M cap. DAA has outlined plans to expand North Runway infrastructure and assess a potential third terminal on the western campus — the same location envisaged in the original 2006 development plan. A formal capacity masterplan is expected from the government in late 2026.

Ready to book your Dublin to India flight? Search live fares now.

Compare all Gulf carrier options — Emirates via Dubai, Qatar Airways via Doha, Etihad via Abu Dhabi — on live fare calendars before you commit. Use the Dublin Fare Calendar to spot the cheapest months.

- NEW Direct Dublin to India Flights — Latest News — Everything known about Air India, IndiGo, and Aer Lingus plans for a nonstop Ireland–India route

- Dublin to Delhi (DEL) Flight Guide 2026 — Full route breakdown, cheapest months, airline comparison, and fare benchmarks for the DUB–DEL corridor

- Finding Affordable Flights from Dublin to Delhi — Booking window strategy, student fares, and fare alert setup for the Dublin–Delhi route

- Best Time to Book Flights 2026 — Data-backed booking windows for Dublin departure routes, including the India corridor

- Compare Fares Across Multiple Airlines — How to search Emirates, Qatar, and Etihad side by side for the cheapest Gulf-hub connection

All information in this article is based on publicly available official sources as of July 2026, including Oireachtas.ie, gov.ie, and dublinairport.com. Aviation legislation, planning permissions, route announcements, and fare conditions can change. Always verify current information directly with the relevant authority, airline, or official government body. MyFlightOffers is not affiliated with any organisation mentioned. This article does not constitute financial, legal, or travel advice.