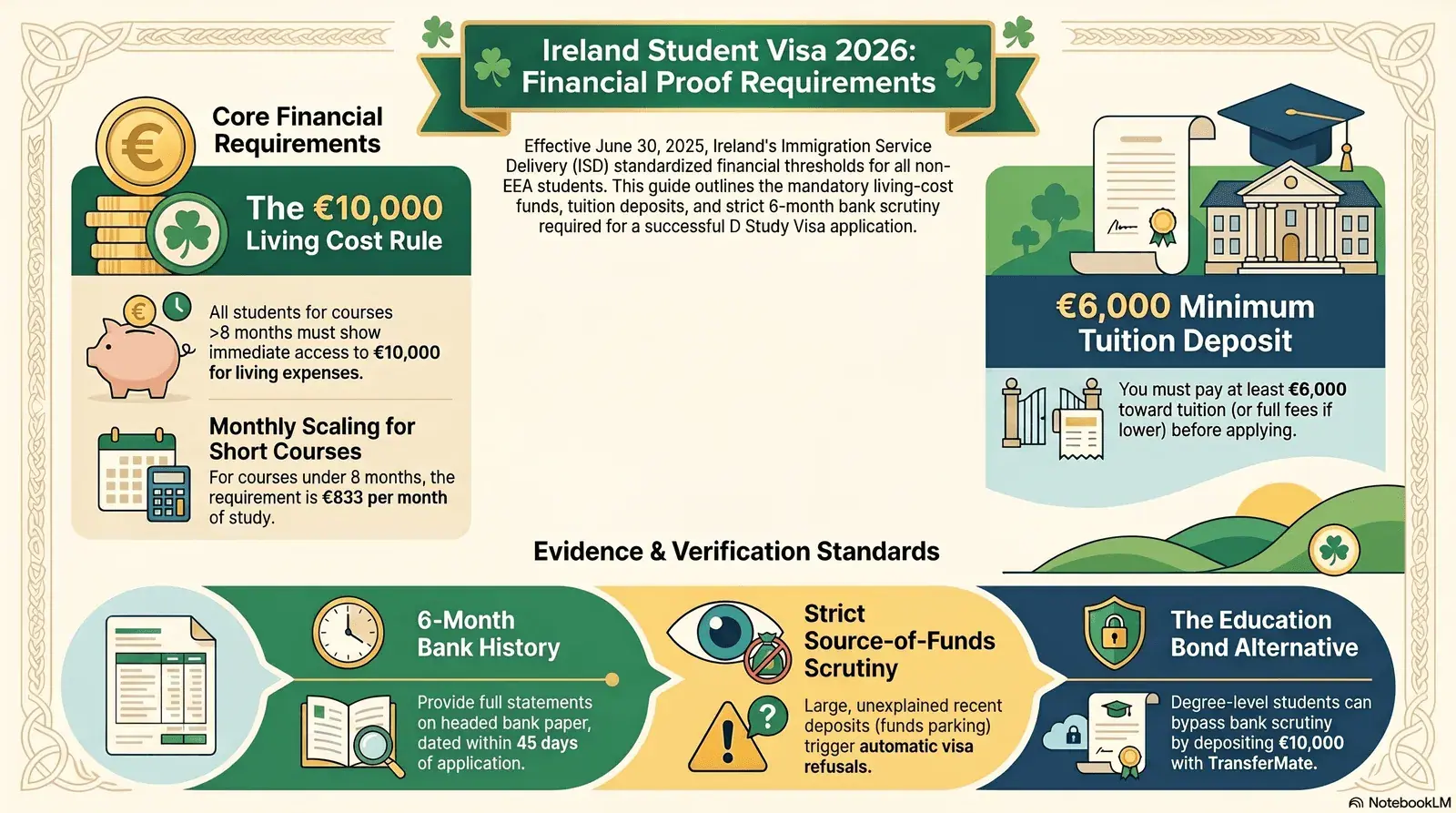

- €10,000 living-cost rule: As of 30 June 2025, all non-EEA students applying for an Irish D Study Visa must show immediate access to €10,000 for courses lasting more than 8 months. There is no longer a separate lower threshold for non-visa-required nationals.

- €6,000 tuition deposit required upfront: You must pay at least €6,000 (or the full course fee if lower) to your college before submitting your visa application. This is a firm pre-application requirement, not a post-arrival one.

- Source of funds is scrutinised heavily: Large, unexplained recent deposits trigger refusals. Your bank statements must cover the last six months in full, on headed bank paper — and every large lodgement must be explained in writing.

Living Expenses Required

€10,000 for courses > 8 months; €833/month for shorter courses

Tuition Deposit Required

€6,000 minimum (or full fee if < €6,000) paid before applying

Bank Statement Period

Full 6-month history on headed bank paper; no older than 30–45 days

Fixed-Term Deposits

Accepted only if bank confirms funds are accessible during studies

In this guide

- What changed in June 2025: the standardised €10,000 rule

- The €6,000 tuition deposit: what it is and how to pay it

- Why source-of-funds checks trip up so many applicants

- Which bank accounts and statement formats are accepted

- Using a sponsor: documentation requirements

- The Education Bond alternative for degree students

- Pre-application financial checklist for June 2026 onwards

1. What Changed in June 2025: The Standardised €10,000 Rule

From 30 June 2025, all non-EEA students applying for an Irish D Study Visa must demonstrate immediate access to €10,000 for the first year of a course lasting longer than 8 months — and the same amount for every subsequent year on top of course fees. This update, announced by Ireland's Immigration Service Delivery (ISD) in March 2025 and confirmed in a reminder published on 23 June 2025, eliminates a previous two-tier system where non-visa-required nationals faced a lower threshold.

The change is the third in a series of phased increases that ISD began in 2023. The progression looked like this:

| Effective date | Visa-required nationals | Non-visa-required nationals |

|---|---|---|

| Before July 2023 | €10,000 | Lower (varied) |

| July 2023 | €10,000 | Incremental increase |

| 30 June 2025 (current) | €10,000 | €10,000 (now aligned) |

For shorter courses, the requirement scales proportionally: €833 per month of study, capped at €6,665 for a course of exactly 8 months. This monthly rate applies equally to visa-required and non-visa-required students, as confirmed in the ISD official reminder of June 2025.

ISD interprets "immediate access" to mean the funds must be in an account you can draw on without restriction at the time of your application — not funds promised from a future salary, not locked in a fixed-term deposit that has not matured, and not contingent on selling an asset. The money must exist in liquid form today.

A common point of confusion is whether €10,000 must be in addition to the tuition fees already paid. The answer is yes: the €10,000 is purely for living expenses. Your paid tuition deposit is counted separately and evidenced by a payment receipt, not by your bank balance at time of application.

Student perspective: "I had €12,000 in my account before applying but had already paid my first semester tuition of €7,500. The visa officer confirmed that my remaining €12,000 bank balance was what mattered for the living-expense test — the paid tuition didn't reduce that requirement." — Priya M., MSc Data Analytics, Dublin, September 2025 intake

2. The €6,000 Tuition Deposit: What It Is and How to Pay It

Before submitting your D Study Visa application, you must pay a minimum of €6,000 toward your course tuition fees — or the full fee amount if the total is below €6,000. This requirement was clarified in ISD's updated guidance for 2026 and serves as proof that your college placement is genuine and financially committed.

Here is how it works in practice:

| Your total course fee | Minimum pre-application payment | Evidence required |

|---|---|---|

| Less than €6,000 | Pay the full course fee | Official college receipt or payment confirmation |

| €6,000 or more | Pay at least €6,000 | Official college receipt or bank transfer confirmation |

| Any amount | Never overpay before visa approval | ISD cautions against paying more than €6,000 pre-visa |

The third row is important. ISD has noted that paying the full year's tuition before your visa is approved creates a significant financial risk if the visa is refused. Pay the required minimum and retain the balance until you arrive.

If your visa is refused after paying full tuition, recovering your money depends entirely on the college's refund policy — and some private colleges have restrictive or slow refund processes. Pay the minimum €6,000 deposit to satisfy the visa requirement; pay the remainder only after you have your visa stamp and are ready to travel.

Acceptable payment evidence includes an official college receipt on institutional letterhead, an electronic bank transfer confirmation showing the college's name and amount, or a college-issued fee acknowledgement letter. Informal payment confirmations (WhatsApp messages from a college representative, unsigned emails) are not sufficient.

🧮 Ireland Student Visa Financial Proof Calculator (2026 Rules)

Estimate the total liquid funds you must show in your bank statements based on your course details and tuition payments.

Required Proof of Funds (Liquid Bank Balance)

3. Why Source-of-Funds Checks Trip Up So Many Applicants

Even if your bank balance exceeds €10,000, your application can be refused if the funds cannot be traced to a legitimate and transparent source — a practice ISD calls "funds parking" scrutiny. Financial adequacy accounts for approximately 30% of all Irish student visa refusals, according to immigration consultants tracking 2025–2026 outcomes.

The core problem is this: students or their families sometimes transfer large sums into a bank account in the weeks before an application to hit the required balance. ISD officers are specifically trained to look for this pattern. When they see a balance that does not reflect the account's normal transactional history, they request an explanation — and if none is forthcoming, they refuse.

What triggers a source-of-funds query?

Any large or irregular lodgement in your six-month statement must be explained. ISD's published guidance is explicit: "Any large or irregular lodgements — for example student loans, lodgement of Savings Certificates, the sale of a property, or any similar type sources — must be fully explained." The key word is "any." There is no threshold above which you are automatically queried; the officer uses judgment about what looks disproportionate to the account's normal pattern.

- A deposit of €10,000–15,000 arriving in a single transaction in the 4–8 weeks before application

- Account normally shows a balance of €500–2,000 suddenly jumping to €12,000 with no explanation

- "Loan cycling" — funds transferred from a relative's account to yours and back, creating artificial balances at key dates

- Bank statements that begin immediately before the six-month window (suggesting the account was opened to park funds)

- Unexplained cash deposits (no record of where the cash originated)

How to document irregular lodgements correctly

Every large lodgement needs a supporting document that proves where the money came from. Accepted explanations include:

- Education loan: Include the full loan sanction letter from a recognised bank or NBFC, showing the loan amount, purpose, and repayment schedule.

- Parental gift: Include a signed, notarised gift letter from the parent, plus the parent's bank statement showing the transfer out of their account on the same date.

- Sale of property or vehicle: Include the sale deed or vehicle transfer document, and the bank entry showing the proceeds received.

- Savings certificate redemption: Include the certificate itself and the bank letter confirming the maturity payout.

- Provident Fund or pension withdrawal: Include the official PF statement and the disbursement letter from the provider.

The single most effective strategy is to build funds gradually over six or more months in your main savings account, without transferring them in from elsewhere. If you are relying on parental support, it is generally cleaner for the parent to appear as a financial sponsor rather than to transfer the funds to you — see Section 5 on sponsor documentation.

4. Which Bank Accounts and Statement Formats Are Accepted

ISD accepts bank statements from standard current accounts and savings accounts — but if you are using a savings or deposit account, you must include a separate letter from your bank confirming you have withdrawal access during your period of study.

Statement format requirements

Bank statements must be on headed bank paper, showing your name, address, account number, and account type. If original paper statements are not available, internet-printed statements are accepted only if every page is notarised by the bank and accompanied by a bank letter confirming authenticity. Handwritten entries or alterations on bank statements are rejected outright.

Statements must cover the full six months immediately preceding your application — not six months of your choosing. The statement date must be no older than 30 to 45 days at the time ISD receives your file.

Fixed-term deposits and locked savings accounts

A fixed-term deposit account is not automatically disqualifying, but it requires a bank letter specifically confirming you can access the funds during your studies. Many standard fixed deposits in India, for example, lock funds for a tenure of 6–36 months with an early-withdrawal penalty. If your FD is still within the lock-in period at the time of application, ISD cannot verify that the funds are truly "immediately accessible" — which is what the standard requires.

| Account type | Accepted? | Additional requirement |

|---|---|---|

| Standard savings account | ✅ Yes | 6-month statement on headed paper |

| Current account | ✅ Yes | 6-month statement on headed paper |

| Fixed-term deposit (matured or breakable) | ✅ With letter | Bank letter confirming funds can be withdrawn |

| Fixed-term deposit (locked, cannot break) | ❌ Not accepted | Does not meet the "immediate access" test |

| Credit card balance | ❌ Not accepted | ISD explicitly excludes credit cards |

| Equity / shares portfolio | ⚠️ Risk | Funds are considered illiquid unless sold; not reliably accepted |

ISD also does not accept statements that show only a closing balance without transaction history. A statement must show all money paid in and out over the six-month period. If your bank's standard statement format omits individual transactions (some online-only banks provide condensed statements), request a full transaction-level statement at a branch.

5. Using a Sponsor: Documentation Requirements

If a parent, relative, or other third party is covering all or part of your living costs in Ireland, ISD requires a detailed documentation package for each sponsor — not just a letter of support. Thin sponsor files are a major source of visa delays and refusals.

For each financial sponsor, you must provide all of the following:

- Evidence of your relationship to the sponsor (birth certificate for parents; marriage certificate if relevant; any other formal link documentation)

- A clear, written statement of the exact amount the sponsor intends to provide for the full duration of your studies in Ireland

- A 6-month bank statement for the sponsor, on headed paper, showing all transactions — meeting the same format rules as your own statement

- Evidence that the sponsor can maintain themselves and any other dependants in addition to supporting you. For employed sponsors: a letter from their employer confirming job title, length of service, and current salary, plus the three most recent payslips

- For self-employed sponsors: a Certificate of Business Registration from the relevant authority in their country, company bank statements, and recent income tax returns

- If the sponsor is receiving funds from a government body or scholarship: full documentation of that funding

ISD does not just check that the sponsor has €10,000 in their account. The officer also assesses whether the sponsor has enough money to maintain themselves and their own household after funding you. A sponsor with €11,000 total savings and three other children is unlikely to satisfy this test. A sponsor with stable salaried employment and €30,000+ in savings is in a much stronger position.

Where a sponsor is funding you via a transfer to your account, note that the transfer itself will appear as a large lodgement in your bank statement and must be explained as described in Section 3. The cleaner approach in many cases is to have the sponsor appear on the visa application directly as a sponsor (with their own financial documentation) rather than transferring money to you — this separates the "source of funds" question from your personal statement.

6. The Education Bond Alternative for Degree Students

Degree programme students enrolled in NFQ Level 7–10 courses on the ILEP (Interim List of Eligible Programmes) can use an Education Bond as an alternative to bank statements for proving living-cost finances.

The bond is operated by TransferMate Education (Education Bond Ireland). Here is how it works:

- You deposit €10,000 with TransferMate through their secure online portal

- TransferMate holds the funds in trust for the duration of your visa application and until you arrive in Ireland

- You receive a receipt, which you submit to ISD as your proof of finances in place of a bank statement

- Once you arrive in Ireland and complete immigration registration, the €10,000 is released into your Irish bank account

- If your visa is refused or you decide not to take up your college place, the bond is returned to you

| Method | Who can use it | Key advantage | Key risk |

|---|---|---|---|

| 6-month bank statement | All students | Flexible; no upfront commitment of €10,000 | Source-of-funds scrutiny; format requirements |

| Education Bond (TransferMate) | Degree students (NFQ 7–10, ILEP-listed) only | Eliminates source-of-funds scrutiny; clean single receipt | €10,000 must be liquid and transferred upfront; contractual with TransferMate |

The bond must be held continuously from the day you submit your visa application through to the day you register with immigration authorities in Ireland. If you withdraw the bond prematurely, ISD may consider this a breach of financial conditions. ISD also notes that it may, at its discretion, request additional financial evidence even if a bond receipt is presented — so the bond is not an absolute shield against further scrutiny, though it is far less frequently queried than personal bank statements.

Only students enrolled on degree programmes (Ordinary Bachelor, Honours Bachelor, Higher Diploma, Postgraduate Diploma, Master's, or Doctoral degree) that are listed on the ILEP are eligible. English-language students and students on Level 5–6 professional courses must use standard bank statements.

7. Pre-Application Financial Checklist for June 2026 Onwards

Use the checklist below at least 3 months before your intended visa application date. Most common refusal reasons are avoidable with 90+ days of lead time.

- ☐ Confirm your course is on ILEP — check ILEP list before paying any fees

- ☐ Pay your €6,000 tuition deposit to the college and get an official receipt or payment confirmation on institutional letterhead

- ☐ Check your 6-month bank balance — does the average monthly balance support an ending balance above €10,000 without a large artificial deposit?

- ☐ Identify any large lodgements in the past 6 months and prepare supporting documents now (loan letters, gift letters, sale documents)

- ☐ Request headed paper statements from your bank; if online-only, ask for notarised copies and an authenticity letter

- ☐ If using a fixed deposit, obtain a bank letter confirming you can break it or access it on demand during your studies

- ☐ If using a sponsor, brief them on the full documentation package (6-month statement, employer letter, payslips, relationship evidence) and gather it in advance

- ☐ Consider the Education Bond if you are a degree student and your personal bank history is thin — the €10,000 moves from your account to TransferMate but it eliminates source-of-funds risk

- ☐ Do not transfer a large sum into your account in the 4–8 weeks before application. If you must receive money from family, document it as a sponsor arrangement rather than a transfer

- ☐ Ensure your statement date is within 30–45 days of the date ISD receives your application (not the date you submit online)

What if your visa is still refused on financial grounds?

You have the right to appeal an Irish student visa refusal within two months of the decision date. The appeal must be sent in writing to the Visa Appeals Officer at ISD and should include any additional financial documentation that was not in your original application. Ireland's refusal rate for student visas remains low — typically 1–4% — so a well-prepared application with clean financial documentation has a very high probability of success.

If your refusal letter specifically cites source-of-funds issues, your reapplication or appeal should include a detailed cover letter narrating the full history of the funds, cross-referenced to each document in your pack. Simply resubmitting the same bank statement without context will result in a second refusal.

Frequently Asked Questions

How much money do I need to show for an Ireland student visa in 2026?

For courses lasting more than 8 months, you must show immediate access to at least €10,000 for the first year of study, plus the same amount for each subsequent year. For courses of 8 months or less, the requirement is €833 per month (maximum €6,665). This is the official ISD requirement updated on 30 June 2025.

Do I need to pay tuition fees before applying for an Ireland student visa?

Yes. You must pay at least €6,000 toward your tuition (or the full course fee if it is less than €6,000) before submitting your student visa application. Evidence of this payment - such as an official receipt or bank transfer confirmation - must be included with your application.

Why are large deposits flagged on Ireland student visa bank statements?

ISD officers are trained to identify 'funds parking' - a large, unexplained lump sum deposited shortly before the application. Such deposits raise concerns about borrowed or temporarily transferred money. All large or irregular lodgements must be fully explained with supporting documentation such as a loan letter, gift letter, or sale receipt.

Are fixed-term deposit accounts accepted as proof of funds for an Ireland student visa?

Fixed-term or locked savings accounts are generally not accepted unless you provide a letter from your bank confirming you can withdraw the funds during your studies. ISD requires that funds be readily accessible, not locked in an account you cannot access until maturity.

Can a parent or relative sponsor my Ireland student visa finances?

Yes. A sponsor (parent, relative, or other third party) can cover all or part of your costs. You must provide the sponsor's 6-month bank statements on headed paper, evidence of their relationship to you (birth/marriage certificate), a letter from their employer confirming employment and 3 recent payslips, and a clear statement of how much they intend to give you.

What is the Education Bond Ireland alternative to bank statements?

Degree programme students (NFQ Level 7-10) can use the Education Bond Ireland service operated by TransferMate as an alternative to bank statements. You deposit €10,000 with TransferMate, which holds it in trust until you arrive in Ireland, at which point the funds are released to you. The bond receipt is accepted by ISD as proof of finances.

Flying to Ireland for your studies?

Once your visa is approved, compare live fares from your home city to Dublin on MyFlightOffers — including student-friendly one-way fares and baggage allowance guides.

All information in this article is based on publicly available official sources including ISD (irishimmigration.ie) and Citizens Information Ireland as of June 2026. Immigration rules change — always verify the current financial requirement directly with ISD before submitting your application. MyFlightOffers is not affiliated with ISD, any college, or any visa agent. This article does not constitute immigration or legal advice.

- NEW Study in Ireland 2026: Visa, Housing & IRP Guide — the full picture from application to arrival

- Ireland Banking Guide for International Students 2026 — opening an Irish bank account before and after arrival

- The Indian Student's Money Survival Guide in Ireland — managing rupees to euros on a student budget

- Ireland Student Survival Guide: Hidden Subsidies 2026 — grants, discounts, and free services you may not know about

- Types of One-Way Student Flight Tickets — which fare type to book when you need a one-way to Dublin