- Use a dual-account strategy: open an AIB or Bank of Ireland student account (€0 fees, Irish IE IBAN — required for salary and rent) plus a Revolut account (instant setup, great for daily spending) — relying on Revolut alone risks rejection by landlords and utilities.

- The proof-of-address catch-22 is solvable: a letter from your university accommodation office or international student office is accepted by both AIB and Bank of Ireland in place of a utility bill — request it on arrival day.

- Use Wise, not a bank wire, to send money from India: Wise charges ~1% on INR→EUR versus 4–5% total cost via Indian bank SWIFT, saving you €400–€750 per year on a €10,000 annual remittance.

🏦 Best traditional account

AIB or Bank of Ireland Student Account

Free · Irish (IE) IBAN · required for salary &

rent

📱 Best digital account

Revolut Standard

Free · instant setup · note LT IBAN caveat

📄 Critical document

PPS Number

Apply at Intreo Centre · needed for work &

Revenue

💸 Cheapest money transfer

Wise (INR → EUR)

~0.5–1% total cost · beats every Irish bank wire

14 questions answered in this guide

- Why do I need an Irish bank account urgently?

- Traditional banks vs. digital neobanks — the honest comparison

- AIB and Bank of Ireland student accounts

- Digital-first options: Revolut, N26, and Bunq

- Document checklist: what you actually need

- Solving the proof-of-address catch-22

- The €10,000 immigration funds rule explained

- SEPA, Irish IBANs, and BIC codes demystified

- Smart international transfers: Wise vs. traditional wire fees

- Linking your bank to Revenue with your PPS Number

- Irish banking scams to know before you arrive

- The master comparison table

- Indian student guide: TCS, forex markup, and the India–Ireland money bridge

- Frequently asked questions

1 Why Do I Need an Irish Bank Account — and Why Urgently?

Opening an Irish bank account within your first two weeks is not optional — it is structurally required for working, renting, and satisfying immigration rules. Without a local account, four things immediately break down.

- Wages: Irish employers are legally required to pay salaries by electronic funds transfer. Without an Irish IBAN, you cannot receive your part-time income. On Stamp 2 permission, you can legally work 20 hours per week during term — at Ireland's minimum wage of €13.70 per hour, that is up to €1,080 gross per month. You cannot access this income without a local account.

- Rent: Virtually every Irish landlord requires a standing order or direct debit from an Irish account. Sending cash or international transfers for rent immediately signals risk to landlords in a competitive rental market.

- Immigration proof of funds: Irish immigration expects you to demonstrate accessible financial resources during visa or IRP (Irish Residence Permit) renewals. Funds held in a foreign account are harder to verify than a current Irish bank statement.

- Irish daily life: Tap-to-pay culture dominates Ireland. Physical cash is increasingly rare. An Irish debit card linked to a local account is your primary transactional tool for groceries, transport, and services.

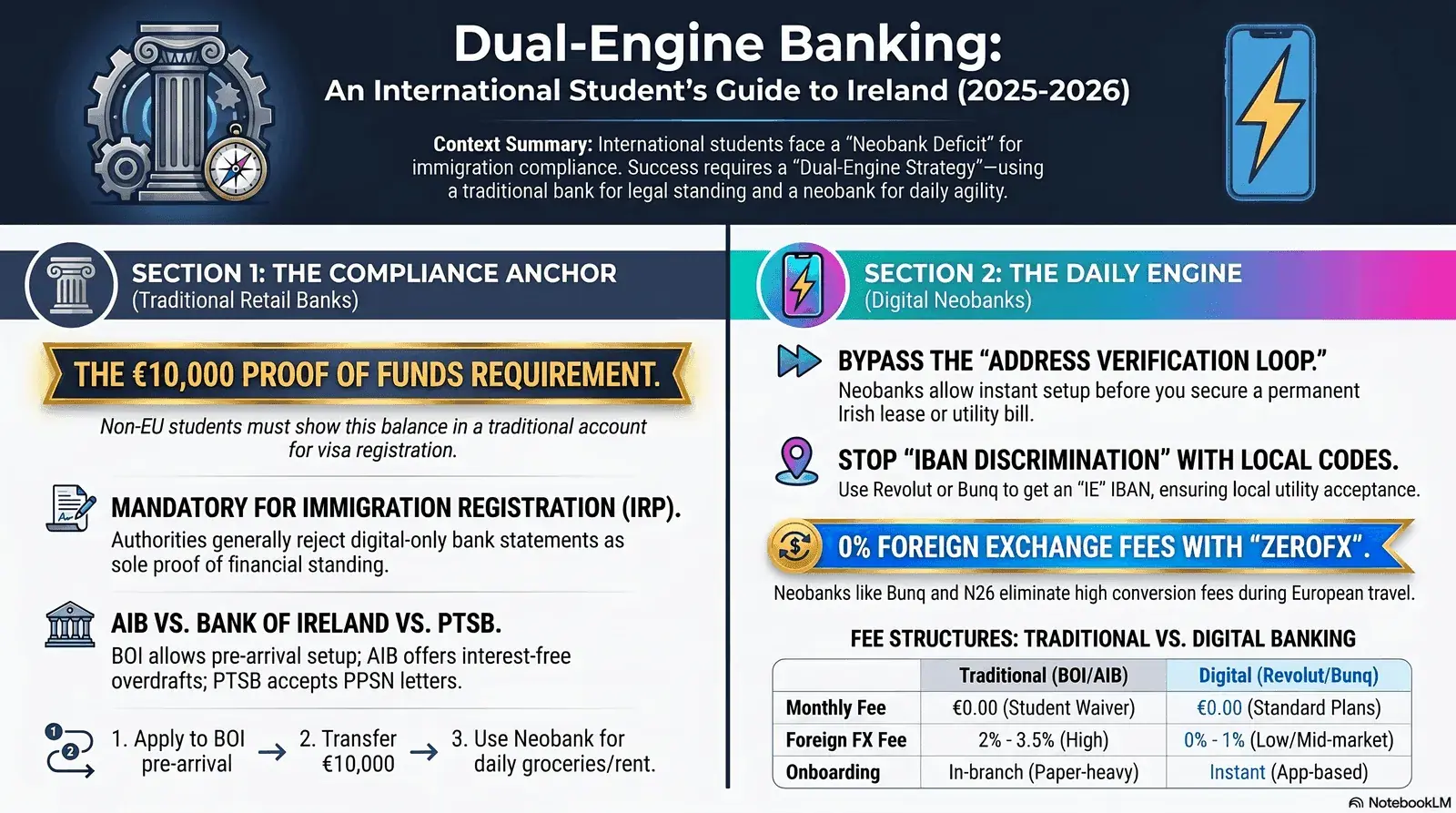

2 Traditional Banks vs. Digital Neobanks — The Honest Comparison

The correct strategy for most international students in Ireland in 2026 is not either/or — it is both. Use a traditional bank (AIB or Bank of Ireland) for your salary, rent direct debit, and any transaction that requires an Irish IBAN starting with IE. Use a neobank like Revolut for daily spending, travel, and international transfers. Here is why each half of that strategy matters.

| Factor | Traditional Banks (AIB / BOI) | Neobanks (Revolut / N26) |

|---|---|---|

| IBAN type | Irish IE IBAN — universally accepted | LT (Revolut) or DE (N26) — rejected by some Irish landlords and utilities |

| Monthly fee (student) | €0 with student status | €0 on standard plan |

| Opening process | In-branch appointment; 3–7 working days | 100% in-app; 10–30 minutes |

| Physical branches | Yes — nationwide network | None (digital support only) |

| International transfer cost | €15–€25 flat + 2–3% rate margin | Free up to limit (Revolut); market rate |

| Forex spending abroad | 1.5–2.5% markup on card spend | Near-zero (Revolut standard, within monthly limit) |

| Deposit protection | €100,000 (EDIS — Central Bank of Ireland) | €100,000 (EDIS via Lithuanian or German licence) |

3 AIB and Bank of Ireland Student Accounts

AIB Student Account (AnyTime) Traditional Free

AIB AnyTime — key facts for international students

- Monthly fee: €0 while in full-time education at an accredited Irish institution (standard AnyTime account charges a €4.50 maintenance fee — waived on student status)

- Contactless Visa Debit card; Apple Pay and Google Pay integration

- AIB Mobile app — rated as one of Ireland's better-reviewed banking apps; includes spend tracking, instant notifications, and SEPA transfer capability

- BIC: AIBKIE2D

- Unlimited transactions and ATM withdrawals (subject to daily limits set on your card)

- Apply in-branch; branch appointments are bookable online at aib.ie

Bank of Ireland 365 Student Account Traditional Free

BOI 365 Student — key facts for international students

- Monthly fee: €0 for students in full-time education; standard 365 account charges €6/month — waived on student proof

- Visa Debit card with contactless; compatible with Apple Pay and Google Pay

- Bank of Ireland app — includes real-time transactions, card controls (freeze/unfreeze), and SEPA transfers

- BIC: BOFIIE2D

- Overdraft facility may be available to eligible students after account maturity — do not rely on this initially

- BOI has the largest ATM network in Ireland; useful in rural university towns

4 Digital-First Options: Revolut, N26, and Bunq

Revolut Standard Neobank

Revolut is the most popular supplementary account among international students in Ireland, primarily because of its instant setup, near-zero spending fees abroad, and strong international transfer rates. Key details for 2026:

- Standard plan: €0/month; Revolut Plus, Premium, and Metal plans add features at a monthly fee

- IBAN type: Lithuanian (LT…) — this is the critical limitation. Since Revolut's EU banking licence is issued through Lithuania, Irish customers receive an LT IBAN, not an IE IBAN. A significant number of Irish landlords, utilities providers, and government-linked services specifically require an Irish (IE) IBAN and will reject a Lithuanian one. Never attempt to pay rent via Revolut without confirming the landlord accepts non-Irish IBANs first.

- International spending: market exchange rate up to a monthly limit (Standard plan); 0.5% fee above the limit on weekdays

- Regulated by the Central Bank of Ireland and the Bank of Lithuania; deposits protected under EU DGS up to €100,000

- Open entirely via the Revolut app — no branch, no proof of address required at initial setup

- Sign-up bonus: if you register using referral code REVOLUT-ANUBHA68LC at revolut.com/referral, you can receive a €20 bonus once eligibility conditions are met (conditions apply, valid July 2026 — confirm the current offer on the Revolut site). See our guide to sending money home from Ireland to India for how Revolut compares with Wise and XE on transfer fees.

N26, the German neobank, operates in Ireland but assigns German (DE…) IBANs. Bunq, the Dutch neobank, similarly issues Dutch (NL…) IBANs. Both face even more frequent rejection by Irish businesses than Revolut's LT IBAN. These accounts are useful as third spending cards for travel or cashback, but should never be your primary account for salary or rent in Ireland.

5 Document Checklist: What You Actually Need to Open an Account

Every traditional Irish bank requires the same core four documents. Arriving at a branch without one means rescheduling — book your appointment and prepare the full set in advance.

- Passport (original): Your primary photo ID. A national ID card from an EU country is also accepted; no other ID is generally sufficient for an initial account opening.

- PPS Number: Ireland's Personal Public Service Number — a 7-digit number followed by 1 or 2 letters (e.g., 1234567A). Required by all Irish banks for account opening. Apply before or immediately after arrival — see Q10 for step-by-step guidance.

- Proof of student enrolment: A letter from your college's international student office or registrar on headed notepaper, confirming your full-time enrolment and programme dates. This simultaneously proves your student status (waiving account fees) and establishes your connection to Ireland.

- Proof of address: This is the hardest document to obtain in your first week. See Q6 for a full breakdown of accepted alternatives.

- Proof of funds (recommended): A 3-month bank statement from your home-country bank, translated into English if applicable. Not always required at opening, but valuable evidence for immigration and sometimes requested during account setup for non-EU nationals.

6 Solving the Proof-of-Address Catch-22

The most common reason international students fail to open an Irish bank account in their first week is the proof-of-address requirement — a genuine catch-22: banks want an address document, but you cannot get one until you have been living somewhere long enough to receive bills.

Irish banks define proof of address as a document not older than 6 months showing your name and Irish address. Utility bills, bank statements, and Revenue letters are the standard examples — none of which a student who just arrived in Ireland will have. Here is what actually works:

- Letter from university accommodation office (most reliable): If you are living in on-campus or university-managed off-campus accommodation, your institution's accommodation office can issue a letter on headed paper confirming your name, Irish address, and residency dates. This is accepted by AIB and BOI without question. Request it from the Accommodation Office as soon as you have a room allocation — many universities issue it automatically with your arrival pack.

- Letter from international student office: The international student office can provide a letter confirming your programme, Irish address, and expected duration of stay. This is widely accepted as a substitute for a utility bill.

- Landlord confirmation letter: If you are renting privately, a letter from your landlord on headed paper (or including their contact details for verification) confirming your tenancy and address is accepted by most bank branches. Ask for this when signing your lease.

- GP registration letter: Once you register with a GP (a process you should complete in your first month), the surgery can issue a letter confirming your address. This is a slower option but useful if other routes fail.

- Use a neobank first: If you need a debit card immediately while your traditional account application is in progress, open Revolut via the app. Revolut does not require proof of address at initial setup. This gives you a functional payment card within 24 hours while your traditional bank application proceeds.

7 The €10,000 Immigration Funds Rule Explained

Irish immigration authorities require international students to demonstrate sufficient funds to cover living expenses, separate from and in addition to prepaid tuition fees. The widely cited guideline is approximately €10,000 per year for living costs, though the Irish Immigration Service (INIS) does not set a fixed statutory minimum — the requirement is that you can demonstrate you will not require public funds during your stay.

In practice, this means:

- Your bank statements (Irish and/or home-country) should show accessible, liquid funds — not investments, property equity, or assets that cannot be readily converted

- Having €10,000+ in your Irish bank account or demonstrable via regular monthly remittances from a family member's account is the cleanest way to satisfy immigration officers at IRP card registration and renewal

- If your funds are held in India or another country, a recent bank statement (translated into English if required) plus a family sponsor declaration letter can serve as supporting evidence

8 SEPA, Irish IBANs, and BIC Codes Demystified

SEPA (Single Euro Payments Area) is a 36-country framework that standardises euro bank transfers across Europe, making cross-border payments within the zone as fast and cheap as domestic ones. Ireland is a full SEPA member. Understanding how the system works saves you significant confusion when sending or receiving money across European borders.

The structure of an Irish IBAN

Country (IE) · Check digits · Bank code (4 letters) · Account number (14 digits) = 22 characters total

- SEPA Credit Transfer (SCT): Same-day or next-day processing for euro transfers between SEPA-member accounts. No surcharge within the SEPA area.

- SEPA Instant Credit Transfer: Now increasingly available — processed in under 10 seconds, 24/7/365. AIB and BOI are progressively rolling out instant SEPA capability.

- BIC codes: AIB's BIC is AIBKIE2D; Bank of Ireland's is BOFIIE2D. Always provide your BIC alongside your IBAN for international transfers even within SEPA — some older systems still request both.

- Non-euro SEPA countries: Norway, Iceland, and Switzerland are in SEPA but do not use the euro — transfers from/to these countries in EUR are covered by SEPA rules but involve a currency conversion at the recipient end.

9 Smart International Transfers: Wise vs. Traditional Bank Wire Fees

Wise (formerly TransferWise) consistently delivers the lowest cost for international money transfers to Ireland, charging approximately 0.4–1% of the total amount plus a small fixed fee, while using the mid-market exchange rate with no hidden markup. Comparing this to a traditional Irish bank wire makes the cost difference stark:

| Transfer method | Fee structure | Cost on a €2,000 transfer | Processing time |

|---|---|---|---|

| Wise | ~0.5–1% + small fixed fee | ~€10–20 | 1–2 business days |

| Revolut (standard plan) | Free up to monthly limit; 0.5% above | ~€0–10 | Minutes to hours |

| Remitly | Varies; often competitive on INR → EUR | ~€12–25 | 1–3 business days |

| Irish bank international wire | €15–€25 flat + 2–3% rate margin | ~€55–€85 | 2–5 business days |

| Indian bank wire (direct) | ₹500–₹1,000 flat + 2–3% rate margin | ~€50–€75 | 3–5 business days |

🧮 Indian Student Forex & TCS Remittance Calculator

Calculate the Tax Collected at Source (TCS) on your education remittance from India and compare the transfer fees of Wise vs. a traditional bank wire.

10 Linking Your Bank Account to Revenue with Your PPS Number

To work legally in Ireland and pay the correct amount of tax, you need a PPS Number and must register with Irish Revenue through the myAccount portal at revenue.ie. Here is the step-by-step process:

- Apply for your PPS Number at your nearest Intreo Centre (find yours at gov.ie/intreo) or Citizens Information Centre. Bring your passport and proof of your Irish address. If you are in student accommodation, bring the accommodation office letter. PPS Numbers are also now available via the MyWelfare.ie portal if you have a verified MyGovID account.

- Register on Revenue myAccount at myaccount.revenue.ie using your PPS Number and personal details. This creates your tax record in Ireland.

- Receive your Tax Credit Certificate (TCC) which your employer uses to calculate the correct tax deductions from your salary. Without this, employers must apply emergency tax (a significantly higher rate) until the certificate is in place.

- Claim unused tax credits at year end via myAccount if you were on emergency tax for any portion of the year — Revenue will issue a refund. Always check your myAccount balance in December of each tax year.

A PPS Number consists of 7 digits followed by 1 or 2 letters (e.g., 1234567AB). Processing typically takes 5–10 working days after your in-person appointment. Some Intreo Centres issue the number on the same day — call your local office ahead to check. Your employer will need your PPS Number before your first payslip is processed.

11 Irish Banking Scams to Know Before You Arrive

Ireland has a well-documented problem with SMS phishing ("smishing") scams that specifically target people who are new to the country and unfamiliar with how legitimate Irish institutions communicate. The following are the most common scams targeting international students in 2026:

- An Post parcel scams: Fake texts claiming a parcel is being held and requiring a €2–€3 customs fee to release it. An Post will never request payment via a link in an SMS. Go directly to anpost.com to track parcels.

- Bank phishing texts: Messages mimicking AIB or Bank of Ireland claiming unusual activity on your account and asking you to click a link to verify your details. Neither bank will ever request your full card number, PIN, or password via text or email.

- Fake landlord rental scams: Listings on Facebook Marketplace or Daft.ie for properties significantly below market rent — often for properties the advertiser does not own. Never wire a deposit without viewing the property in person and verifying the landlord's identity via the RTB (Residential Tenancies Board) at rtb.ie.

- Revenue tax refund scams: Emails or texts claiming you are owed a tax refund and must click a link to claim it. Revenue will post you a cheque or credit your bank account directly — they will never request bank details via an unsolicited message. Always check via myaccount.revenue.ie directly.

- GNIB/IRP registration scams: Third-party websites that offer to book your immigration appointment for a fee. Irish immigration appointments are booked free of charge at inis.gov.ie — you should never pay an intermediary to secure one.

Report banking scams to the Garda National Cyber Crime Bureau (GNCCB) via garda.ie, and report fraudulent texts to your mobile carrier by forwarding the message to 7726 (free on all Irish networks).

12 The Master Comparison Table

Choose your accounts based on their specific strengths — no single account does everything optimally for an international student in Ireland.

| Account | Monthly fee | IBAN type | Salary/rent direct debit | Intl. transfers | Opens in-app? | Best for |

|---|---|---|---|---|---|---|

| AIB AnyTime (student) | €0 | IE ✓ | Yes | Expensive | No (branch) | Salary, rent, primary account |

| BOI 365 Student | €0 | IE ✓ | Yes | Expensive | Partial (branch to complete) | Salary, rent, primary account |

| Revolut Standard | €0 | LT ⚠️ | Risky — check first | Excellent (within limit) | Yes — 100% | Daily spending, travel, transfers |

| N26 Standard | €0 | DE ⚠️ | Often rejected | Good | Yes — 100% | European travel spending |

| Wise (transfer service) | €0 account; fee per transfer | Multi-currency | Not a current account | Best in class | Yes — 100% | Receiving/sending international money |

13 Indian Student Guide: TCS, Forex Markup, and the India–Ireland Money Bridge

Indian students remitting funds from India to Ireland under the Liberalised Remittance Scheme (LRS) should plan carefully around Tax Collected at Source (TCS) thresholds, which affect the real cost of funding your Irish education from Indian bank accounts.

TCS on LRS remittances for education

| Remittance amount per financial year | Source of funds | TCS rate |

|---|---|---|

| Up to ₹10 lakh | Any | 0% (no TCS) |

| Any amount | Education loan from a specified financial institution | Nil (0% TCS) |

| Above ₹10 lakh | Personal/family funds (not a loan) | 2% on amount above ₹10 lakh (from 1 April 2026) |

TCS collected by your remitting bank is not a final tax — it is fully creditable against your total Indian income tax liability for the financial year, or refundable if you have no Indian tax due. File your ITR (Income Tax Return) in India to claim the credit. Always confirm the current rates with your Indian bank at the time of transfer, as the government periodically revises TCS rules.

Using your Indian credit card in Ireland

Most standard Indian credit cards carry a 3.5% forex markup on international transactions. On €10,000 of annual spending in Ireland, that is approximately ₹29,000 in markup fees alone. Consider upgrading to a low-forex card before departure:

- ICICI MakeMyTrip card: 0.99% forex markup — the lowest widely available from any major Indian bank

- HDFC Infinia / Bank of India (Kotak Miles Elite): 2% forex markup

- SBI ELITE / SBI Miles Elite: 1.99% forex markup

- Wise Debit Card (recommended): Near-zero conversion fees for EUR spending using your Wise account balance; no forex markup in the traditional sense

- Best ICICI Bank Credit Cards for Travel 2026 — includes MakeMyTrip ICICI at 0.99% forex

- Best SBI Credit Cards for Flights & Travel 2026 — SBI ELITE and Miles Elite at 1.99% forex

- Axis Bank Credit Cards for Flights 2026 — Magnus at 2% forex with unlimited international lounge access

Frequently Asked Questions

Can I open an Irish bank account before arriving in Ireland?

You can pre-register with neobanks like Revolut entirely online before arriving — no physical presence is required. Traditional Irish banks (AIB, Bank of Ireland) require an in-branch appointment, so your account opening must take place after you arrive in Ireland.

Do I need a PPS Number to open a bank account in Ireland?

Yes — Irish banks require a PPS Number for account opening. Apply at your nearest Intreo Centre or Citizens Information Centre, or online at MyWelfare.ie. Neobanks like Revolut can be opened without a PPS Number initially, but you still need one to work legally in Ireland.

Will Revolut work for paying rent in Ireland?

It depends entirely on your landlord. Because Revolut assigns Lithuanian (LT) IBANs to Irish customers rather than Irish (IE) IBANs, many Irish landlords, letting agents, and utilities companies will reject Revolut standing orders and direct debits. Always confirm whether your specific landlord accepts non-Irish IBANs before attempting to use Revolut for rent — and have an AIB or BOI account ready as the primary option.

Is my money safe in a Revolut account in Ireland?

Revolut holds an EU banking licence issued through Lithuania (granted by the European Central Bank in 2024). Deposits are protected under the European Deposit Guarantee Scheme up to €100,000 per depositor. Revolut is also subject to supervisory oversight by the Central Bank of Ireland for its Irish operations.

How do I get a refund if I overpaid tax as a student?

Log into myAccount at myaccount.revenue.ie at the end of the tax year (December or January). Under "Income Tax Return," file a simple end-of-year return for the relevant year. Revenue will process any refund owed and credit it to your Irish bank account. Students on emergency tax for part of the year frequently receive refunds of €200–€600.

What is the Central Bank of Ireland's role in student banking?

The Central Bank of Ireland is the financial regulator for all banks and payment institutions operating in Ireland. It enforces consumer protection rules including the Consumer Protection Code, which gives you the right to clear, fair information about fees and account terms. If you have a complaint about an Irish bank that the bank has not resolved, escalate to the Financial Services and Pensions Ombudsman (FSPO) at fspo.ie — free of charge.

Which is the best bank for international students in Ireland in 2026?

For most international students, the recommended approach is a dual-account strategy: open an AIB or Bank of Ireland student account (free, Irish IBAN, required for salary and rent direct debits) plus a Revolut Standard account (free, instant, excellent for daily spending and low-fee international transfers). Relying on Revolut alone risks IBAN rejection from landlords and Irish utilities who require an Irish IBAN.

What can I use instead of a utility bill as proof of address when opening an Irish bank account?

The most widely accepted alternatives for international students without utility bills are: a letter from your university accommodation or international student office on headed notepaper confirming your address; a letter from a registered GP; or in some cases, a letter from the accommodation provider confirming your tenancy. Neobanks (Revolut, N26) typically do not require proof of address for initial account setup.

How do I send money cheaply from India to Ireland?

Wise consistently offers the lowest cost for INR to EUR transfers, typically charging around 0.5 to 1 percent of the total amount plus a small fixed fee, while using the mid-market exchange rate. This substantially undercuts traditional bank international wire transfers which charge €15-€25 flat fee plus a 2 to 3 percent exchange rate margin. Indian students should also factor in TCS (Tax Collected at Source) on LRS remittances above ₹10 lakh.

What is the €10,000 funds rule for Irish student immigration?

Irish immigration authorities expect international students to demonstrate they have sufficient funds to cover their living expenses for the duration of study, in addition to prepaid tuition fees. The widely referenced guideline is approximately €10,000 per year for living costs, though the exact threshold can vary. This should be evidenced by bank statements showing accessible funds, not invested or illiquid assets.

What TCS applies when Indian students remit money to Ireland for education?

Under India's Liberalised Remittance Scheme (LRS), TCS (Tax Collected at Source) applies on remittances above ₹10 lakh per financial year (threshold raised from ₹7 lakh by the Finance Act 2025). Education funded by a loan from a specified financial institution attracts nil TCS. For education funded from personal funds (not a loan), the TCS rate is 2% on the amount above ₹10 lakh from 1 April 2026 (down from 5%). TCS is fully creditable against your Indian income tax liability or refundable if no tax is due. Always confirm the current rates with your remitting bank, as TCS rules are subject to change by the government of India.

Ready to fly to Ireland? Compare live fares first.

Once your banking strategy is sorted, find the best available fare on your route from India, China, or anywhere else to Dublin.

All bank account features, fees, IBAN details, BIC codes, TCS rates, SEPA rules, proof-of-address policies, transfer fees, PPS Number processes, and immigration guidance described in this article are based on publicly available information from AIB (aib.ie), Bank of Ireland (bankofireland.com), Revolut (revolut.com), Wise (wise.com), the Irish Revenue Commissioners (revenue.ie), the Irish Immigration Service (irishimmigration.ie), the Central Bank of Ireland (centralbank.ie), and the Government of India Ministry of Finance as of June 2026. Banking policies, TCS rates, IBAN types, and immigration requirements change regularly and without advance notice. Always verify current terms directly with the relevant bank, Revenue, and INIS before making financial decisions. MyFlightOffers is not affiliated with any bank, transfer service, or Irish government body mentioned in this article. This article does not constitute financial, tax, or immigration advice.

- NEW How to Apply for a PPS Number in Ireland as an International Student (2026 Guide) — step-by-step MyWelfare.ie application, required documents, appointment booking, and how to avoid the 40% emergency tax rate from your first payslip.

- NEW IRP Card Registration: A Step-by-Step Guide for International Students in Ireland (2026) — the step before you can open a bank account: Burgh Quay appointment, €300 fee, required documents, and how your Stamp 2 IRP card enables your AIB/BOI account application.

- NEW Sending Money Home from Ireland to India: Wise vs Revolut vs XE vs Bank Wire for Students 2026 — exact fee comparison for all four providers with side-by-side INR amounts received, plus TCS rules and step-by-step setup guides.

- NEW Pre-Departure Checklist for Indian Students Flying to Ireland 2026 — 30-Day Countdown — when to set up your NRE/NRO account, how to activate Wise before you leave India, what cash and forex card to carry, and the full document checklist for Dublin Airport immigration.

- NEW Ireland Student Visa 2026 Financial Proof Update — €10,000 Rule, Source Checks & Tuition Deposit — the updated ISD bank statement and source-of-funds requirements you need before applying for your D Study Visa, including the €6,000 tuition deposit rule and the Education Bond alternative.

- NEW Best Savings & Notice Accounts in Ireland for International Students 2026 — once your current account is open, compare An Post, Trade Republic, Revolut Savings Vaults and AIB notice accounts to make your savings work harder (with DIRT tax explained).

- NEW The Indian Student's Money Survival Guide to Ireland (2025–2026) — DCC avoidance, Wise vs SWIFT transfers, TCS rules, SEPA direct debits, PPSN application, and Irish scam protection in one guide.

- NEW Revenue.ie Emergency Tax Guide for International Students 2026 — step-by-step: get your PPSN, register on MyAccount, link your employer, and reclaim every euro of overpaid emergency tax.

- NEW Aviation Tech Careers in Ireland 2026: GDS & Airline Operations — break into GDS analyst and aircraft leasing roles at AerCap, Aer Lingus, and Ryanair Labs using your Stamp 1G.

- Part 1 — Universities, Costs, Scholarships & Flights — top 10 universities, GOI-IES scholarship, IELTS requirements, and how to book your flight to Dublin.

- Study in Ireland 2026: Ultimate Visa, Housing & IRP Guide — step-by-step arrival guide covering student visa setup, Burgh Quay IRP appointments, PPS Number registration, housing checks, and safety.

- Finding Affordable Flights: Dublin to Delhi 2026 — all airlines, fare benchmarks, cheapest booking windows, and Indian credit card offers.