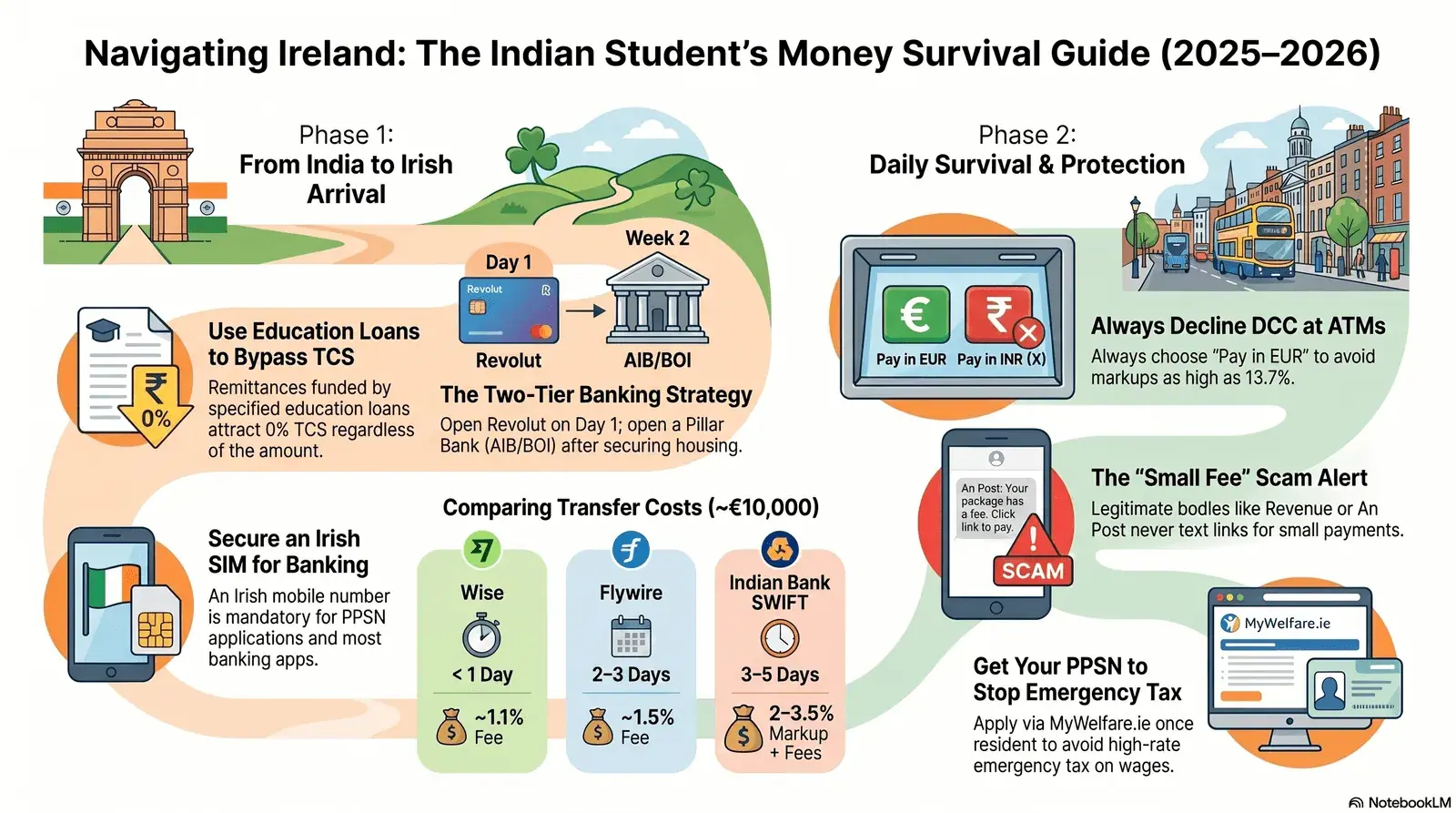

- Open a free student account at AIB, Bank of Ireland, or PTSB (all €0 maintenance) plus Revolut for instant day-one banking — but you'll need a PPSN and proof of an Irish address for the pillar banks. Use an education loan (0% TCS in India) and send money via Wise, not a bank SWIFT wire.

- Always pay in EUR, never your home currency, at every Irish ATM and card terminal — accepting Dynamic Currency Conversion (DCC) adds a markup averaging ~5% and documented as high as 13.7%. It's legal, optional, and entirely avoidable by pressing "pay in euro."

- Treat every "pay a small fee" text as a scam. eFlow toll, An Post parcel, and Revenue tax-refund smishing/phishing are rampant in Ireland. Revenue, An Post, and eFlow never text or email you a payment link. Verify by typing the official .ie address yourself.

🏦 Best day-one account

Revolut (Irish IBAN)

Instant setup · accepts student visa/IRP

🏛️ Best pillar bank

AIB / Bank of Ireland / PTSB

€0 fees · IE IBAN · needed for rent & salary

💸 Cheapest transfer

Wise (INR → EUR)

~1.1% total cost · mid-market rate

⚠️ Biggest daily trap

DCC at ATMs & terminals

~5–13.7% markup · always choose EUR

6 sections covered in this guide

Key Findings

- Student bank accounts are genuinely free, but the address requirement is the real hurdle. AIB, Bank of Ireland, and Permanent TSB all offer third-level student current accounts with €0 quarterly maintenance fee and no charges on everyday euro transactions. The friction for Indian students is proving an Irish address and getting a PPSN — which is why most students open a Revolut account (instant, app-based, accepts non-EEA students with a valid visa/IRP) on arrival and a pillar-bank account once settled.

- Fund tuition through an education loan and Wise, not a bank wire. Under Budget 2025 (effective 1 April 2025) the LRS threshold rose from ₹7 lakh to ₹10 lakh, and remittances funded by a specified education loan now attract 0% TCS regardless of amount. Self-funded education remittances above ₹10 lakh attract TCS (Budget 2026 cut this to 2% from April 2026). Indian bank SWIFT wires cost 2–3.5% in exchange-rate markup plus fixed fees plus $15–$25 correspondent-bank deductions; Wise uses the mid-market rate with a transparent ~1.1% fee on INR→EUR.

- DCC is the single most avoidable cost in daily life. Whether at an ATM or a shop terminal, if the screen offers to charge you in rupees (or shows "pay in INR / pay with conversion"), decline it and choose EUR.

- Smishing is the dominant fraud threat to new arrivals. The same template — "you owe a small fee, click this link" — is cloned across eFlow, An Post, Revenue, and delivery brands.

1 Irish Bank Accounts for Students

All three main Irish pillar banks offer genuinely free student current accounts — but each has different documentation requirements, application channels, and small print worth knowing.

AIB Student Plus Account (third-level) Traditional Free

AIB Student Plus — key facts for Indian students

- Fees: €0 quarterly maintenance and transaction fees, including direct debits, standing orders, and debit-card purchases in euro. AIB also pays the annual Government Stamp Duty on the debit card for student-account holders.

- Eligibility: Any person enrolling in or currently in a full-time third-level course of at least one academic year, including postgraduates.

- Documentation (AML rules): Proof of identity — valid passport, driving licence, or EU national ID card. Proof of current permanent address (dated within 6 months) — utility bill, correspondence from a regulated financial institution, a government department letter, or a Central Applications Office (CAO) letter.

- Perks: Interest-free overdraft up to €1,000 (1st/2nd year) or €1,500 (3rd/4th year); commission-free purchase/sale of foreign currency notes at branch.

- Full AIB Phone & Internet Banking and AIB Mobile Banking app; BIC: AIBKIE2D

Bank of Ireland 3rd Level Current Account Traditional Free

Bank of Ireland — key facts for Indian students

- Fees: No account maintenance fee; no separate fees for direct debits, standing orders, card payments, ATM use, or duplicate statements. Charges can apply for international/foreign-currency card use and Government Stamp Duty.

- Eligibility: Open to undergraduates and postgraduates of any age on any full-time course (since April 2021).

- Documentation: Photo ID — passport, driving-licence card, or EU national ID card. Proof of address — utility bill, financial statement, or letter from Revenue, an approved university, the CAO, the Department of Social Welfare, or the immigration service; documents must be in English. A selfie is required in the application.

- Application channels: Online, in branch, or by phone (+353 1 404 4034). You can apply up to 45 days before you arrive in Ireland.

- Student credit card: Credit limit €600 (1st/2nd year) or up to €1,000 (3rd year+); representative APR 20.2% variable; BIC: BOFIIE2D

Permanent TSB (PTSB) Student Current Account Traditional Free

PTSB Student Account — key facts for Indian students

- Fees: No fees for maintaining the account and no day-to-day transaction charges (direct debits, cash lodgements/withdrawals, euro debit-card purchases).

- Charges still apply for ATM use outside the Eurozone; debit-card purchases in foreign currency; a referral item fee of €5 per item (max €15/day); and an unpaid item fee of €10 for unpaid direct debits/standing orders.

- Eligibility: Students aged 18+ in full-time third-level education (including postgrad of at least one year), for a maximum of 5 years; one account per student.

- Extras: Includes Zippay person-to-person mobile payments (send up to €1,000 instantly using a mobile number). BIC: IPBSIE2D

Digital Neobanks for Non-EEA / Indian-passport Students

Revolut Neobank

- Best day-one option. Open entirely via the app — no branch required. Standard plan: €0/month.

- Irish IBANs since 13 Feb 2023: New Irish Revolut customers receive IE IBANs, resolving the earlier LT IBAN limitation for most use cases. Revolut is a licensed bank (regulated by the Bank of Lithuania/ECB and by the Central Bank of Ireland for conduct of business); deposits up to €100,000 covered by the Lithuanian deposit-guarantee scheme.

- Non-EEA students (e.g. Indian passport holders) must provide proof of residency such as a student visa or IRP — explicitly accepted; the permit must be valid for at least 3 months.

- Revolut is legally required to collect your PPSN (once you have one) to report to Revenue. Setup takes minutes in-app; you must be 18+.

N26 requires EU/EEA residency and a mailing address in a supported country to receive the Mastercard — not realistically openable from India pre-arrival for an Indian-passport holder. Bunq is similarly restricted to EEA residents.

Money Jar (an Irish-IBAN provider some colleges recommend) is available to international students in all countries, can be opened before travelling, gives an Irish IBAN immediately, and does not require proof of address at opening. You must supply your IRP card within 3 months. Useful if you want an Irish IBAN before you land.

The Irish IBAN Structure

An Irish IBAN is exactly 22 characters. Euro transfers within SEPA need only the IBAN — no BIC/SWIFT required.

Country (IE) · Check digits · 4-letter bank code (AIBK/BOFI/IPBS) · 6-digit sort code · 8-digit account number = 22 characters total

2 International Money Transfers from India to Ireland

The EUR/INR rate in June 2026 is around ₹110.4 per euro, meaning €10,000 ≈ ₹11 lakh. A 1% fee on that transfer is ~₹11,000; a 3% bank markup is ~₹33,000. Getting this right matters.

Transfer Options Compared

| Service | Fee structure | Cost on ₹11 lakh (≈€10,000) | Speed |

|---|---|---|---|

| Wise | Mid-market rate + ~1.1% fee (fixed + variable) | ~₹12,000 (~1.1%) | 95% arrive in <1 day |

| Flywire (tuition only) | ~1.5% bundled in exchange rate | ~₹16,500 | 2–3 business days |

| Indian bank SWIFT (SBI/HDFC/ICICI) | 2–3.5% rate markup + ₹500–₹1,000 flat + $15–$25 correspondent fee | ~₹25,000–₹40,000+ | 3–5 business days |

| Western Union | Widest rate margins of all options | High (not recommended for large sums) | Fast for cash |

What are the TCS rules for Indian students remitting money to Ireland in 2026?

India's Liberalised Remittance Scheme (LRS) applies when Indian residents send money abroad. Budget 2025 and Budget 2026 changed the rules materially:

| Remittance amount (per financial year) | Source of funds | TCS rate (from April 2026) |

|---|---|---|

| Up to ₹10 lakh | Any | 0% (no TCS) |

| Above ₹10 lakh | Education loan from a specified financial institution | 0% TCS (regardless of amount) |

| Above ₹10 lakh | Self-funded / personal / family funds | 2% TCS on amount above ₹10 lakh |

| Above ₹10 lakh | Non-education remittances | 20% TCS |

TCS collected by your remitting bank is not a final tax — it is fully creditable against your Indian income tax liability or refundable via your ITR (Income Tax Return) if no tax is due. Without a PAN, TCS rates rise significantly (5% for education loans, 10% for other sources). Always confirm current rates with your bank at the time of transfer — TCS rules are updated regularly.

Wise now supports education-loan verification for Indian transfers, so loan-funded remittances qualify for 0% TCS at the time of transfer. INR transfer limit: up to ₹15 lakh per working day. Exact fees vary — always check Wise's live calculator at wise.com before sending.

3 Dynamic Currency Conversion (DCC) — What It Is and How to Avoid It

Dynamic Currency Conversion (DCC) is one of the most common and avoidable financial traps for Indian students in Ireland. Understanding it takes 2 minutes and can save you hundreds of euros per year.

What DCC Is

When you use your Indian card at an Irish ATM or chip-and-PIN terminal, the machine may offer to charge you in rupees (INR) instead of euros (EUR). Accepting this means the merchant's DCC provider — not your card network (Visa/Mastercard) — sets the exchange rate. That rate is almost always significantly worse than the mid-market rate.

Per Bankrate (citing Kinstellar analysis): the average DCC markup across Europe is around 5%, with an extreme case of 13.7% documented at an ATM. One US traveller reported a 12.95% DCC fee. This markup is on top of any foreign-transaction fee your home bank charges. On €200 of cash withdrawal: 5% DCC = €10 extra per transaction. Multiply that by every ATM visit over a year and it becomes substantial.

How to Decline DCC — Every Time

- At the ATM or terminal prompt, choose "Pay in EUR", "Without conversion", or "Proceed without conversion."

- If the screen asks "Pay in INR?" or "Press YES for INR, NO for euros" — press NO.

- Under EU Regulation 2019/518, providers must show you the conversion markup as a percentage versus the ECB reference rate and must allow you to decline — they cannot choose for you. If a terminal won't let you pay in euro, decline and report it to your card issuer.

- Prefer bank-branded ATMs (AIB, BOI, PTSB) — Irish-bank ATMs generally don't charge a withdrawal fee for euro cash. Privately operated ATMs (in shops, pubs, kiosks — especially Euronet machines) are the most likely to push DCC and add operator fees.

🧮 Indian Student Money Survival & DCC Calculator

Calculate the total INR cost and savings of sending tuition/living funds (€10,000) and spending locally in Ireland using optimized transfer and card payment methods.

💵 Total Cost & Net Savings Breakdown (Exchange Rate: €1 = ₹110.4)

4 Daily Banking in Ireland: SEPA, Utilities, SIMs, Rent & Transport

SEPA Direct Debit — The Backbone of Irish Bill Paying

Recurring euro bills — electricity, gas, broadband, gym, some rent — are collected by SEPA Direct Debit. You authorise a mandate with your IBAN, and the money is pulled from your account on the due date.

Utilities

- Electric Ireland (electricireland.ie): Set up/amend direct debit in "Your Account Online" — needs a Republic-of-Ireland bank account allowing direct debit + your IBAN. Non-ROI accounts require a paper mandate.

- Bord Gáis Energy (bordgaisenergy.ie): Set up online; account debited 14 days after the bill issue date. Only ROI-based accounts can be set up online; direct debit/Level Pay can earn a discount.

- Uisce Éireann (Irish Water): Most domestic water is funded through general taxation; standard household water charges generally don't apply. If billed (e.g. for excess use), set up direct debit through your Uisce Éireann account. Verify directly on uisce.ie for the latest setup process.

Mobile SIMs

Bring your passport — SIM registration is mandatory. Plans run €20–€30 for 28-day prepaid bundles with unlimited/10 GB+ 5G data and EU roaming. Three, Vodafone, and Eir are the main operators. Buy at Dublin Airport, operator stores, or convenience stores; eSIMs available. You need an Irish mobile number for banking apps and MyGovID.

| Provider | Plan | Price | Highlights |

|---|---|---|---|

| Three | Super Surfer | €20/28 days | Unlimited 5G data, 200 mins/texts, 26 GB EU roaming |

| Three | Connect Complete | €30/28 days | Unlimited data/calls, 32 GB EU roaming |

| Vodafone | Data Unlimited 5G | €20/28 days | Unlimited 5G data |

| Eir | Prepaid plans | €10–€20 | Entry-level and mid-tier options |

An Post Money Services

Ireland's 900+ post offices offer commission-free foreign-currency cash (GBP, USD, CAD, AUD, PLN; ID required for exchanges over €150; up to €3,000 per transaction), bill payments, and cash lodgements/withdrawals. An Post is also a Western Union agent. The An Post Money Currency Card is a prepaid Mastercard holding up to 15 currencies — but note the 5.75% FX fee if you spend in a currency you don't hold on the card.

Rent Payment Norms

Irish rent is most commonly paid by bank transfer or standing order in euro to the landlord's Irish account. Landlords are generally reluctant to deal with international transfers for monthly rent and expect payment from a local euro account — another reason to open an Irish IBAN. Always get a rent book/receipts (a tenant right under the Residential Tenancies Acts). For current guidance on accepted rent-payment methods, check rtb.ie.

Leap Card (Public Transport)

Top up via the TFI Leap Top-Up app (hold the card to an NFC smartphone to check balance and top up — online top-ups are usually collectable from 8am the next day), at retail outlets/ticket machines, or online. New zonal fares for Dublin and the Commuter Area took effect on 28 April 2025. The app shows daily/weekly fare capping.

5 Security & Scams Targeting New Arrivals

The common thread across all Irish scams targeting students: an urgent "pay a small fee / update your details" message with a link. Legitimate Irish bodies never send payment links by SMS or email.

Fake texts claim an unpaid toll or "radar ticket" and link to cloned sites harvesting card details. Bank of Ireland's Head of Fraud warned (May 2023): "eFlow has advised that they do not send text messages with links to confirm account or payment details." Transport Infrastructure Ireland identified and destroyed over 70 fake eFlow websites in 2023 alone. Report bogus eFlow texts to [email protected], then delete.

Texts tell recipients to pay an outstanding delivery fee — usually €1.90, €1.95, or €1.99 — then link to a fake An Post page to steal card data. An Post's official Security page states: "An Post will never ask you to pay customs charges via a link in an SMS or email… If customs charges are due on your item, you will receive a postcard in the post." Verify the domain carefully: the text immediately before ".com/.ie" must be exactly "anpost.com".

Fake "tax refund," "tax bill," or "you are due an audit" emails/texts. Revenue states it "will never contact you by email, SMS or phone call to inform you of a tax refund or bill" and uses the secure MyEnquiries service instead. Forward suspect messages to [email protected] and delete. Never click; type www.revenue.ie yourself.

Scammers impersonate government services to harvest your PPSN and bank details. Your PPSN is sensitive — share it only with employers, your bank/Revolut (for tax reporting), your college, and official bodies. The government will never send you a payment link to obtain or verify your PPSN.

Type the official .ie address into your browser yourself. Check sender addresses end in @revenue.ie, @anpost.com, etc. Never use phone numbers or links supplied in the message. If a bank text seems real, call the number on the back of your card. Report frauds to your local Garda station; report suspect texts to 7726 (free on all Irish networks).

6 PPSN: What It Is, Who Needs It, and How to Apply

Your PPSN (Personal Public Service Number) is your unique Irish reference number — 7 digits followed by 1–2 letters — used for tax, social services, and banking. It is the rough Irish equivalent of a PAN. You need it to work legally, to fully activate your bank account (Revolut requires it for Revenue reporting), to register with a GP, and for numerous government services.

How to Apply for Your PPSN

- Create a basic MyGovID account at mygovid.ie (you'll need an Irish mobile number, which is why buying a SIM in week 1 is important).

- Apply online at MyWelfare.ie (Department of Social Protection). Official service page: gov.ie/en/service/12e6f-get-a-personal-public-service-pps-number/

-

Upload your documents:

- Photo ID — your passport

- Proof of address — utility bill or official document within the last 3 months, with a valid Eircode (not a hostel or temporary address)

- Evidence of why you need a PPSN — e.g. college enrolment letter or employer letter

- Wait 5–10 working days (some sources say 2–3 weeks during busy academic months). Your PPSN is posted to your address.

- Provide your PPSN to: your employer (before first payslip), your bank/Revolut (for Revenue tax reporting), and your college if required.

10-Step Action Plan

Before You Leave India

- Take an education loan from a specified financial institution if you can — loan-funded remittances are 0% TCS in India, freeing up cash and avoiding refund paperwork. Keep your PAN updated with your bank.

- Open a Wise account for ongoing transfers (mid-market rate, ~1.1% fee), and consider Money Jar if you want an Irish IBAN before landing. Set up Flywire only if your Irish university mandates it — and compare its INR total against Google's rate first.

- Carry proof-of-address documents in English and your admission/offer letter.

Week 1 in Ireland

- Download Revolut, verify with passport + student visa/IRP, and start banking immediately. This covers you before the pillar-bank account opens. Tip: sign up with referral code REVOLUT-ANUBHA68LC at revolut.com/referral to receive a €20 bonus once eligibility conditions are met (conditions apply, valid July 2026).

- Buy a SIM (Three/Vodafone/Eir, ~€20) — you need an Irish mobile number for banking apps and MyGovID.

- Secure long-term accommodation, then get an Eircode and a proof-of-address document.

Weeks 2–4

- Apply for your PPSN via MyGovID → MyWelfare.ie the moment you have an address. Then open an AIB / Bank of Ireland / PTSB student account for a clean Irish IBAN that all utilities and landlords accept.

- Set up SEPA Direct Debits for utilities from your Irish account; pay rent by standing order in euro.

Ongoing Money Hygiene

- Always pay in EUR at every ATM/terminal; prefer bank-branded ATMs; decline DCC every time. This alone saves ~5%+ per foreign-card transaction.

- Never click pay-a-fee links. Verify eFlow/An Post/Revenue by typing the .ie address yourself. Report scams to [email protected] (eFlow), [email protected] (Revenue), and to the Gardaí.

Frequently Asked Questions

Which is the best bank account for Indian students arriving in Ireland?

The recommended strategy is dual-account: download Revolut immediately on arrival for instant banking (it now issues Irish IBANs and accepts student visas), then open an AIB, Bank of Ireland, or Permanent TSB student account within your first 2-3 weeks once you have your PPSN and proof of Irish address. All three pillar-bank student accounts charge €0 maintenance. Revolut alone is insufficient because some landlords and utilities still require a pillar-bank Irish IBAN for direct debits.

What is Dynamic Currency Conversion (DCC) and how do I avoid it in Ireland?

Dynamic Currency Conversion (DCC) is when an ATM or card terminal offers to charge your Indian card in rupees (INR) instead of euros (EUR). The DCC provider sets a worse exchange rate, adding a markup that averages around 5% across Europe and can reach 13.7% in extreme cases. To avoid DCC: always choose 'Pay in EUR' or 'Without conversion' at every ATM and terminal. If the screen asks 'Pay in INR?', press No. Under EU regulations, merchants must show you the markup and allow you to decline. Always decline DCC - every time.

What is the cheapest way to send money from India to Ireland in 2026?

Wise is the cheapest transparent option, using the mid-market exchange rate with a fee of approximately 1.1% on the INR to EUR route (around ₹12,000 on a ₹11 lakh / €10,000 transfer). Traditional Indian bank SWIFT wires cost 2-3.5% in exchange-rate markup plus ₹500-₹1,000 flat fee plus $15-$25 correspondent-bank deduction - often 4-5x more expensive than Wise. For tuition payments specifically, use Flywire only if your university requires it, and always compare its quoted INR total against Google's mid-market rate first.

How do I apply for a PPSN in Ireland as an international student?

You must be physically resident in Ireland to apply for a PPSN. Steps: (1) Create a basic MyGovID account at mygovid.ie. (2) Apply online at MyWelfare.ie (Department of Social Protection). Upload your passport, proof of Irish address (utility bill or official document within 3 months, with a valid Eircode), and evidence of why you need a PPSN such as a college enrolment letter or employer letter. Processing takes 5-10 working days and the PPSN is posted to your address. Apply as soon as you secure long-term accommodation.

Why do Irish utilities and landlords sometimes reject my Revolut IBAN?

Under Irish SEPA scheme rules (BPFI), paperless or electronic direct-debit mandates can only be set up for Irish-domiciled accounts. Although Revolut now issues Irish (IE) IBANs to new Irish customers (since February 2023), some older Revolut accounts still have Lithuanian (LT) IBANs, and certain utilities or landlords may specifically require a pillar-bank IE IBAN. If your direct debit is rejected, open an AIB, Bank of Ireland, or PTSB student account and set up the direct debit from there.

Ready to fly to Ireland? Compare live fares first.

Once your banking strategy is sorted, find the best available fare on your route from India to Dublin.

- Scholarships for Indian Students in Ireland 2026: University Merit Awards Beyond GOI-IES — map every funding route from Trinity and UCD merit awards to Inlaks, JN Tata, and IRC research grants, with a stacking strategy to layer awards

All bank account features, fees, IBAN details, TCS rates, SEPA rules, proof-of-address policies, transfer fees, PPSN processes, and scam descriptions in this article are based on publicly available information from AIB (aib.ie), Bank of Ireland (bankofireland.com), Permanent TSB (ptsb.ie), Revolut (revolut.com), Wise (wise.com), the Irish Revenue Commissioners (revenue.ie), the Central Bank of Ireland (centralbank.ie), An Post (anpost.com), Transport Infrastructure Ireland (eflow.ie), the Department of Social Protection (mywelfare.ie/mygovid.ie), and the Government of India Ministry of Finance, as of June 2026. Banking policies, TCS rates, SEPA rules, and scam tactics change regularly and without advance notice. Always verify current terms directly with the relevant bank, Revenue, and INIS before making financial decisions. MyFlightOffers is not affiliated with any bank, transfer service, or Irish government body mentioned in this article. This article does not constitute financial, tax, or immigration advice.

- New Leap Card & Public Transport Guide for International Students in Ireland (2026) — Student Leap Card application, the €1 90-minute fare, €12 weekly cap, and how to travel Dublin, Cork, Galway and Limerick on a student budget.

- New Ireland to India Semester-Break Flights 2026: Cheapest Booking Strategies for Students — when to book for Christmas, Easter and summer, student fares on Air India and Emirates, open-jaw routing tricks, and baggage vs. courier cost comparison.

- New Best Part-Time Jobs for International Students in Ireland 2026 — Sectors, Pay and How to Get Hired — Stamp 2 work rights, best-paying sectors (tutoring €20–€35/hr, IT support, research assistant), PPS number setup and how to avoid the 40% emergency tax trap.

- New Sending Money Home from Ireland to India: Wise vs Revolut vs XE vs Bank Wire for Students 2026 — side-by-side INR comparison for €500, €1,000 and €2,000 transfers, with TCS rules, step-by-step setup and the XE referral code for a €50 bonus.

- Related Best Savings & Notice Accounts in Ireland for International Students 2026 — compare An Post, Trade Republic, Revolut Savings Vaults and AIB notice accounts to earn more on your idle funds, with DIRT tax and eligibility rules explained.

- Related Ireland Banking Guide for International Students 2026 — deep dive into opening procedures, proof-of-address catch-22, SEPA, and the TCS guide for Indian students.

- Related Revenue.ie Emergency Tax Guide for International Students 2026 — step-by-step: get your PPSN, register on MyAccount, link your employer, and reclaim every euro of overpaid emergency tax.

- Ireland Student Survival Guide 2026: Hidden Subsidies & Savings — student discounts, subsidised schemes, and money-saving hacks most students never find.

- Study in Ireland 2026: Ultimate Visa, Housing & IRP Guide — step-by-step arrival guide covering student visa setup, Burgh Quay IRP appointments, PPS Number registration, housing, and safety.

- Finding Affordable Flights: Dublin to Delhi 2026 — all airlines, fare benchmarks, cheapest booking windows, and Indian credit card offers.

- Best ICICI Bank Credit Cards for Travel 2026 — includes MakeMyTrip ICICI at 0.99% forex markup for international spend.